When Do You Start Paying 40 Tax Uk

Ah, the magic number 40. For some, it's the age when you finally feel like you've got it all figured out (or at least pretend to). For others, it's the year you might start eyeing up those comfy slippers with a little more enthusiasm. But in the land of HMRC, 40 isn't just a milestone; it's a tax bracket. And for many of us, the question pops up like a surprise pop quiz: When do I actually start paying 40% tax in the UK? Let's break it down, shall we? No need to break out the calculator just yet – we're going for a chill vibe here.

Think of your income like a delicious multi-layered cake. The first layer is usually tax-free, thanks to your Personal Allowance. This is the foundational sweetness, the bit everyone gets to enjoy without the taxman taking a slice. Then comes the next layer, taxed at a more manageable rate (hello, basic rate taxpayers!). But eventually, you reach the premium layer, the one with the extra cherries and gold leaf – the 40% tax bracket.

Decoding the Tax Brackets: A Gentle Unpacking

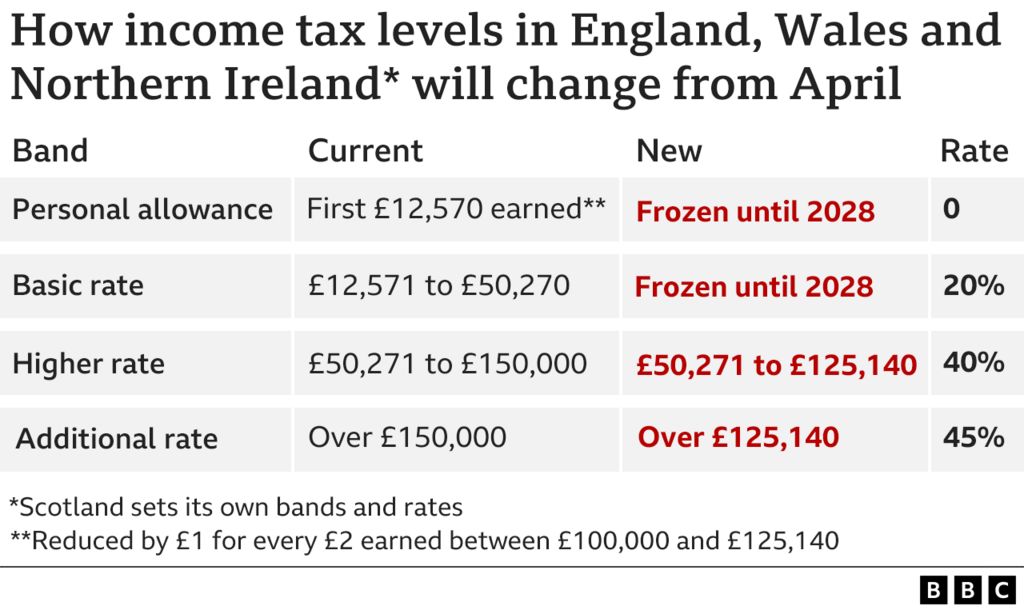

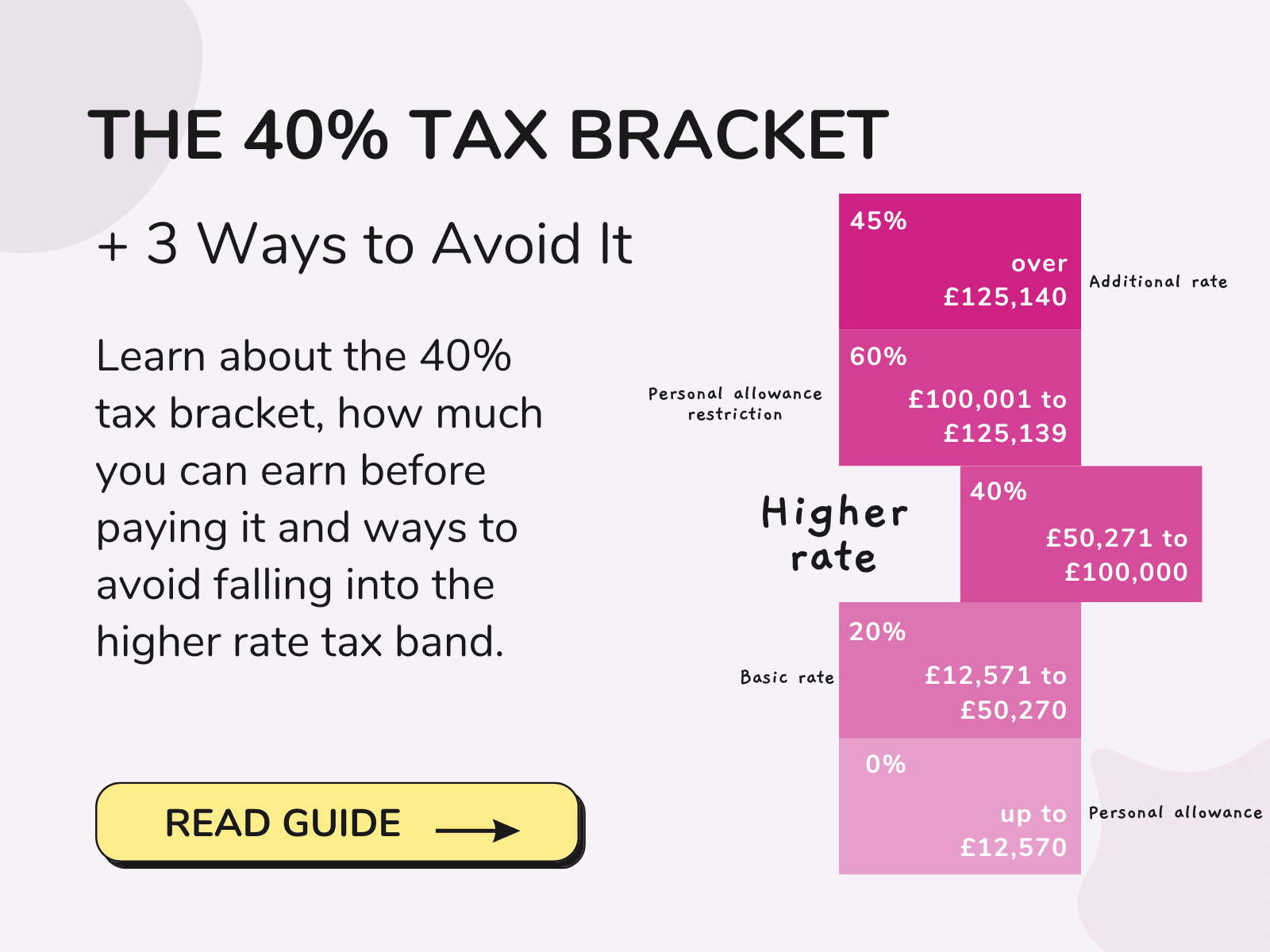

So, what's the golden ticket, or rather, the threshold that ushers you into this higher tax tier? For the 2023/2024 tax year in England, Wales, and Northern Ireland, the magic number is an income of £50,270. Once your taxable income – that’s your income after your Personal Allowance and any other tax-deductible expenses – creeps above this figure, you start paying 40% on the additional income.

Must Read

It's crucial to remember it's not your entire income that gets slapped with the 40% rate. It’s only the portion that falls within that higher bracket. So, if you earn £55,000, you're not suddenly paying 40% on all of it. You're still paying the lower rates on the first chunk, and then 40% on the £4,730 that’s over the £50,270 threshold. Think of it like a special occasion discount – you only pay the premium price for the extra indulgence.

Scotland: A Slightly Different Flavour

Now, if you're living north of the border, things get a tiny bit more interesting. Scotland has its own devolved income tax system, which means the thresholds and rates can differ. For the 2023/2024 tax year, the Scottish starter rate kicks in, followed by intermediate and then the higher rate. The point at which Scottish taxpayers hit the 40% bracket is slightly lower, around £25,688. So, if you're a Scot reading this, pay attention to your specific tax bands!

It's a bit like comparing your favourite local bakery to one in another city. Both sell delicious bread, but the ingredients or recipes might have subtle, yet important, differences. Always good to know which bakery you're shopping at, tax-wise!

What Exactly is "Taxable Income"?

This is where things get a little more hands-on. Your "taxable income" isn't just your gross salary from your main job. It’s your total income from all sources, minus certain allowances and deductions. This can include things like:

- Your main salary or wages

- Income from a second job or freelance work

- Rental income from a property

- Pension income

- Interest from savings (above your ISA allowance, of course!)

- Dividends from shares

And then come the deductions! These are the things that help reduce your taxable income, bringing that cake layer down a bit. Think of them as edible decorations you can strategically place to make the cake look (and feel) smaller.

- Your Personal Allowance: For most people under 65, this is currently £12,570. For every pound you earn over £100,000, your Personal Allowance gets reduced by 50p.

- Pension Contributions: Money you put into a workplace pension or a private pension is often tax-relief eligible. This is a big one for reducing your taxable income!

- Charitable Donations: Giving to a registered charity can also reduce your taxable income. It’s good for the soul and your tax bill.

- Certain Business Expenses: If you're self-employed or have a limited company, allowable business expenses will reduce your profits and therefore your taxable income.

So, if your gross income is £55,000, but you have £3,000 in pension contributions and your Personal Allowance is £12,570, your taxable income is £55,000 - £3,000 - £12,570 = £39,430. In this scenario, you wouldn't even be close to the 40% tax bracket! See? It’s all about what’s left after the good stuff is taken off.

A Fun Little Fact: The Personal Allowance Paradox

Did you know that the Personal Allowance itself is tapered for those earning over £100,000? It's like a subtle nod from the taxman that while you're doing exceptionally well, they're also keeping a closer eye. For every £2 you earn above £100,000, you lose £1 of your Personal Allowance. So, by the time you hit £125,140, your Personal Allowance is completely gone!

When Does the 40% Really Bite?

Generally, the 40% tax rate, often referred to as the "higher rate," kicks in when your taxable income exceeds the threshold. For England, Wales, and Northern Ireland in 2023/2024, this is £50,270.

So, let's say you're a savvy freelancer or you've had a fantastic year with your investments, and your taxable income is £52,000. Here's the breakdown:

- You'll pay the basic rate (20%) on your income up to the higher rate threshold.

- You'll pay the higher rate (40%) on the income between the basic rate threshold and your total taxable income.

- You'll pay the additional rate (45% in England, Wales, and Northern Ireland) on any income above £150,000.

It's always worth double-checking the specific tax year you're looking at, as these thresholds can, and do, change annually. Think of them as the ever-evolving set list for your favourite band – you need to catch the latest tour to get the most up-to-date experience.

The Devil is in the (Tax) Details

It’s important to distinguish between your gross income and your taxable income. Many people assume that if their salary hits £50,270, they’ll immediately be in the 40% bracket. But as we’ve seen, with allowances and potential deductions like pension contributions, your taxable income could be significantly lower. This is why understanding your personal tax situation is key.

Imagine you’re planning a picnic. You’ve got your basket, your blanket, and your delicious sandwiches. Your gross income is the whole picnic spread. Your Personal Allowance is the space for your main sandwiches. Pension contributions and other deductions are like the tasty side salads and drinks that take up space but make the overall picnic (your taxable income) more manageable and enjoyable. If you only have a small space for sandwiches, you might not need a massive picnic basket.

Practical Tips for Navigating the 40% Zone (or Avoiding It!)

If you find yourself approaching or entering the 40% tax bracket, don't panic! It's often a sign of a successful and well-earning year, which is something to celebrate. However, there are smart ways to manage your tax affairs:

1. Embrace Your Pension Contributions

This is probably the most effective way to reduce your taxable income. Workplace pensions offer tax relief at your highest rate. If you're a higher-rate taxpayer, your contribution is boosted, and your taxable income is reduced by the gross contribution. This means you get the benefit of tax relief at 40%!

If you're self-employed, consider setting up a personal pension. It's a fantastic way to save for your future while also potentially lowering your current tax bill.

2. Explore Other Tax-Efficient Investments

ISAs (Individual Savings Accounts) are your best friend here. Any interest, dividends, or capital gains you make within an ISA are tax-free. Maximising your ISA allowance is a no-brainer.

For higher net worth individuals, other investment vehicles might offer tax advantages, but these can be more complex and often require professional advice.

3. Understand Allowable Business Expenses

If you're self-employed or run a limited company, meticulously tracking and claiming all your allowable business expenses is crucial. This directly reduces your taxable profit. Think of every legitimate expense as a tiny tax rebate!

4. Consider the Timing of Your Income

This is more advanced and often applies to those who have control over when they receive certain income, like bonuses or payments for freelance work. Sometimes, deferring income into the next tax year can help you stay below the higher rate threshold.

5. Seek Professional Advice

This is the golden rule. Tax laws can be complex and change regularly. A qualified accountant or tax advisor can provide tailored advice based on your specific circumstances. They can help you maximise your allowances, identify potential deductions, and ensure you're not paying a penny more tax than you need to. Think of them as your personal tax sherpas, guiding you through the mountain of tax legislation.

A Cultural Nod: The "Aspiration Zone"

Interestingly, the 40% tax bracket is often dubbed the "aspiration zone." It signifies a level of income that many people strive for, a marker of professional success. While it comes with a higher tax bill, it also implies that you've achieved a certain level of financial comfort. It’s the financial equivalent of reaching the viewing platform on a skyscraper – you get a fantastic view, even if the air is a little thinner.

![When Do I Start Paying Tax UK? [2024/25] Complete Guide](https://legendfinancial.co.uk/wp-content/uploads/2024/11/When-Do-I-Start-Paying-Tax-1024x576.webp)

Think of historical figures who achieved great things. They often navigated financial complexities, and understanding tax was part of that journey. From the merchants of the Silk Road to the innovators of the industrial revolution, managing finances, including taxes, was always a crucial skill.

The Psychological Impact

Reaching the 40% bracket can sometimes feel a bit jarring. The jump from 20% to 40% on that additional income can seem steep. It’s a psychological hurdle for some, but it's also a testament to your earning potential. It’s like upgrading from a standard hotel room to a suite – it costs more, but the amenities and the view are often worth it.

The Bottom Line: It’s All About Your Taxable Income

So, to recap, the 40% tax rate in the UK generally kicks in when your taxable income exceeds the higher rate threshold. For most of us in England, Wales, and Northern Ireland, this is £50,270 for the 2023/2024 tax year. For Scottish taxpayers, the figure is different.

It's not about your gross salary alone, but what's left after your Personal Allowance and any other allowable deductions. Embrace the power of pension contributions, ISAs, and professional advice to navigate your tax situation smoothly.

A Gentle Reflection

Life’s a bit like a well-baked loaf of bread. You have your basic ingredients – your effort, your skills, your time. Then come the leavening agents and the flavours – your opportunities, your investments, your smart financial choices. Your income is the finished loaf, and taxes are, well, the crust. Sometimes it’s a generous, satisfying crust, and sometimes, it’s a slightly thinner one. What matters is that the loaf itself is nourishing and sustaining.

Whether you're comfortably in the basic rate or starting to explore the higher rate, the key is to approach your finances with curiosity and a plan. It’s not about dwelling on the percentages, but about making informed decisions that support your lifestyle and your future. After all, a little understanding of tax can go a long way in ensuring you have more of that delicious loaf to enjoy for yourself.