What Is Average Uk Pension Pot

So, there I was, wrestling with my laptop, trying to figure out this whole pension thing. You know, the little email that pops up from your provider, usually around tax return time, with a cheerful, "Here's how your nest egg is doing!" My neighbour, Brenda, a woman who could charm a badger out of its sett, popped her head over the fence. "Still wrestling with that pension, dear?" she asked, a twinkle in her eye. "Honestly, I just sort of hope it's enough." Hope. That was her strategy. And bless her, Brenda seemed perfectly content living on hope and a healthy dose of her state pension. But for most of us, especially those of us who didn't inherit a small fortune or win the lottery, hope alone doesn't quite cut it, does it? It got me thinking, what is an average UK pension pot, anyway? Is Brenda's 'hope' a realistic national average, or are we all a bit clueless? Let's dive in, shall we? Because frankly, this is something we all need to get our heads around, whether we're Brenda or someone frantically trying to understand the jargon.

The truth is, figuring out the "average UK pension pot" is about as easy as herding cats. There are so many different types of pensions out there – defined contribution, defined benefit, auto-enrolment, private pensions, you name it. Each one tells a slightly different story. Plus, the pot sizes vary wildly depending on age, salary, how long you've been saving, and, let's be honest, a sprinkle of luck (or lack thereof).

But even with all those caveats, people do try to put a number on it. And it's a number that often leaves us scratching our heads. So, what are we actually talking about when we say "average"?

Must Read

The Elusive Average: Numbers That Make You Squint

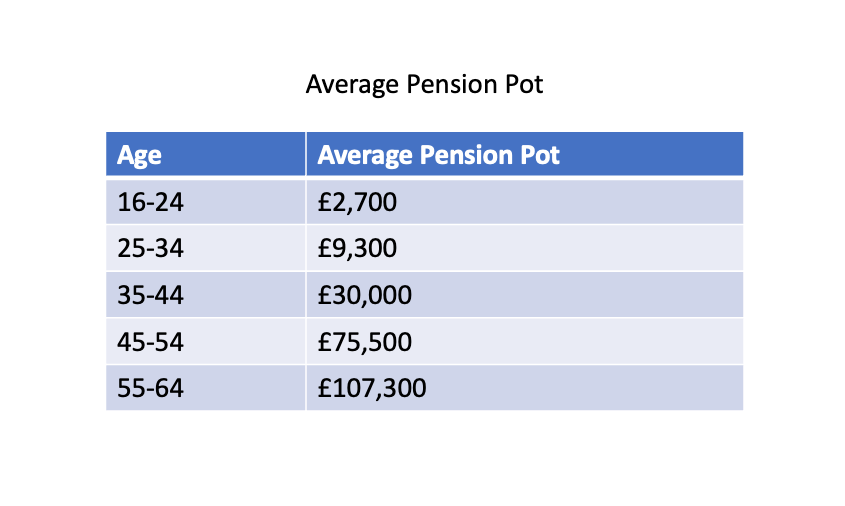

Alright, brace yourselves. The figures you'll see bandied about can be a bit of a rollercoaster. Some reports suggest the average pension pot for someone nearing retirement is around £60,000 to £100,000. Others, looking at a broader age range, might put it lower, perhaps in the £20,000 to £40,000 mark. Confused yet? Yeah, me too. It's like trying to guess the average height of a human when you're only measuring babies and basketball players.

The difficulty lies in what "average" actually means here. Are we talking about the mean average (where you add up all the pots and divide by the number of people)? Or the median average (where half the pots are bigger and half are smaller)? The mean can be skewed by a few super-rich individuals with massive pots, making the average look deceptively high. The median, on the other hand, might be a more realistic reflection for the majority of people.

And then there's the age factor. A 25-year-old with a decent salary and a few years of auto-enrolment will have a vastly different pot to a 65-year-old who's just about to draw their pension. So, when you hear an "average," it's crucial to consider the context. Is it an average for all working adults? Or for those close to retirement? This distinction is HUGE.

It's also worth noting that these figures are often based on surveys and data from pension providers. Not everyone has a private pension, and many rely solely on the state pension. So, while these numbers give us a benchmark, they don't tell the whole story for everyone.

Why the Numbers Might Feel a Little... Underwhelming

Let's be blunt. For many people, these average figures can feel a bit deflating. If you're imagining a comfortable retirement, the thought of having just £60,000 or £100,000 might send a shiver down your spine. Why is that? Well, it's simple maths, really.

If you have, say, £100,000 in your pension pot, and you want that to last you for 20-25 years in retirement (which is a reasonable assumption these days), you're looking at drawing out around £4,000 to £5,000 per year. That's £333 to £416 per month. Now, is that enough to live on, especially after covering essentials like housing, utilities, and food? For many, the answer is a resounding no.

And that's assuming you don't face any unexpected expenses, or that inflation doesn't eat away at your savings faster than you anticipate. It's a sobering thought, isn't it? This is why Brenda's 'hope' strategy, while charming, is probably not the most robust financial plan for the majority of us.

The Auto-Enrolment Effect: A Ray of Hope, But Not a Miracle Cure

Now, before we all descend into a pit of despair, let's talk about auto-enrolment. This has been a game-changer for pension saving in the UK. It automatically enrols eligible employees into a workplace pension scheme, with contributions from both the employee and the employer, plus tax relief from the government.

Since its introduction, millions more people have started saving for retirement. This is fantastic! It means that a whole generation is now building up pension pots who might not have done so otherwise. The idea is sound: get more people saving, and over time, those pots will grow.

However, auto-enrolment has only been around for a decade or so. That means the pots built up by people who were auto-enrolled are still relatively young. The contributions are often set at a basic level to start with (though they are increasing), so while it's a brilliant start, it might not be enough to build a truly substantial pot for everyone, especially those who started saving later in life or have lower earnings.

Think of it like planting a sapling. It's a good start, and with care and time, it will grow into a sturdy tree. But you can't expect it to provide shade and fruit overnight. The same goes for auto-enrolment. It's a vital step, but we might need to see higher contribution rates and more time for these pots to mature into significant retirement funds.

What About Defined Benefit Pensions?

It's worth a quick mention of defined benefit (DB) pensions, often called "final salary" pensions. These are less common now, largely found in the public sector or older, larger private companies. With a DB scheme, your pension is based on your salary and how long you worked there, promising a specific income in retirement, rather than a pot of money.

These are generally considered more secure and predictable. The "average pot" figures we've been discussing mostly refer to defined contribution (DC) schemes, where the retirement income depends entirely on how much you've saved and how well your investments have performed. So, if you have a DB pension, the "average pot" conversation is a bit of a different ballgame for you – you're likely in a more secure position.

Factors That Make Your Pot Bigger (or Smaller!)

So, if the average is what it is, what makes some people’s pots significantly bigger than others? A few key things come to mind:

- Salary: This is a biggie. The more you earn, the more you (and your employer) can contribute, and the more the government's tax relief will be worth. Simple, really.

- Age at Start: Starting early is like giving your money superpowers. Compound interest is your best friend. Even small amounts saved over decades can grow into something impressive. The earlier you start, the less you have to contribute later to reach a decent sum.

- Contribution Rate: How much are you and your employer actually putting in? The minimum auto-enrolment contributions are a starting point, but many people choose to contribute more, and some employers offer better schemes.

- Investment Performance: This is the wildcard. How well have your pension fund's investments performed over the years? Market ups and downs will affect your pot. A well-chosen, diversified investment strategy can make a significant difference. Conversely, poor performance or a too-cautious approach can hold it back.

- Fees: Pension providers charge fees, and these can eat into your returns over time. High fees, even if they seem small percentage-wise, can really chip away at your pot.

- Breaks in Employment/Lower Earnings: If you've had periods of unemployment, taken career breaks (perhaps for childcare), or worked in jobs with lower pay, your pension contributions will have been lower or non-existent during those times. This can have a significant impact on your final pot.

It’s a bit like baking a cake. Your salary is the main ingredients, starting early is letting the dough prove, contributions are the extra chocolate chips, investment performance is how well the oven bakes it, and fees are like accidentally burning the edges.

The "Not Enough" Reality Check

Let's circle back to that "not enough" feeling. Many financial experts suggest you'll need around 70-80% of your pre-retirement income to maintain your lifestyle in retirement. For someone earning £30,000 a year, that's £21,000 to £24,000 annually. If your state pension provides £9,000-£10,000 (which is roughly what the full flat-rate state pension offers), you still need another £12,000-£14,000 from your private pension.

For that, you'd need a pot of roughly £240,000 to £280,000, assuming a 4% withdrawal rate to make your money last. Suddenly, those average figures of £60,000 or £100,000 seem a very long way off for a substantial retirement. This is the harsh reality for many. It's not about living a life of luxury; it's about being able to meet basic needs and enjoy your later years without constant financial worry.

So, What Can You Do?

Right, enough with the doom and gloom. The point of looking at these averages isn't to depress you, but to arm you with information. If the average isn't enough, what can you do about it? Brenda might be happy with hope, but we can be a bit more proactive, can't we?

1. Understand Your Current Situation

First things first, know what you've got. Dig out those pension statements. Look at your online accounts. Figure out how many pension pots you have, what type they are, and what their current value is. Don't shy away from it – facing the music is the first step.

2. Review Your Contributions

If you're auto-enrolled, check your contribution rate. Can you afford to increase it, even by 1%? That little bit extra can make a surprising difference over time. Talk to your employer about options for increasing contributions. Also, consider if you have any old, forgotten pension pots lying around. Consolidating them into one place can make them easier to manage and potentially reduce fees.

3. Project Your Retirement Income

Use online pension calculators (most pension providers have them, or MoneyHelper is a good resource). Plug in your current savings, your age, and your expected retirement age. See what kind of income you're projected to get. This will give you a realistic target to aim for.

4. Consider Later Life Contributions

If you're further along in your career and feeling that the pot isn't big enough, don't despair. Every extra contribution counts. If you can afford to, making a lump sum contribution or increasing your regular payments can boost your pot significantly, even in the later years of saving.

5. Think About Your Investment Strategy

If you have control over your pension investments (which you usually do with DC schemes), take a look at your fund choices. Are they performing well? Are the fees reasonable? Don't be afraid to seek independent financial advice if you're unsure. A qualified advisor can help you choose investments that align with your risk tolerance and retirement goals.

6. Don't Forget the State Pension

While we're talking about private pots, remember the state pension. Make sure you're on track to receive your full entitlement by checking your National Insurance record. It's a vital foundation for your retirement income.

It's easy to get bogged down in the jargon and the seemingly low average figures. But the most important thing is to take action. Whether you're 22 or 52, starting, continuing, or increasing your pension contributions is one of the most powerful things you can do for your future financial security.

So, while Brenda's hope might sustain her, for the rest of us, it's about informed action, consistent saving, and a good dose of proactive planning. The average UK pension pot might be a number that makes you squint, but your own pension pot is entirely within your power to influence. Let's make it a good one, shall we?