What Is A Good Credit Score With Clear Score

So, picture this: my friend Sarah, bless her cotton socks, was absolutely buzzing. She'd just booked her dream holiday to Bali. Flights? Booked. Hotel? Picture-perfect villa with an infinity pool? Done. But then came the bombshell. She wanted to rent a car for exploring the island, and the rental company hit her with a "credit check." Sarah, who frankly considers a Starbucks loyalty card her most significant financial commitment, nearly fainted.

She came to me, wide-eyed, asking, "What is a credit score? And why does this random company care if I can pay for a scooter in paradise?" It got me thinking. We hear about credit scores all the time, especially when something like getting a loan or a new phone contract pops up. But what does it actually mean? And more importantly, what’s considered good, especially when you’re looking at something like Clear Score?

It’s funny, isn’t it? We live in this digital age where everything is tracked and measured, from our steps on a smartwatch to our scrolling habits on social media. Yet, this whole credit score thing can feel like this mysterious black box. You know it’s important, but the finer details? They can be a bit… fuzzy.

Must Read

Let’s dive into this. What exactly is a credit score? Think of it as your financial report card. It's a number that lenders (banks, credit card companies, even your landlord sometimes!) use to assess how risky it might be to lend you money. A higher score suggests you're a responsible borrower who pays bills on time, while a lower score might raise a few red flags.

And this is where Clear Score, and similar services, come in. They're like your personal credit score cheerleader. They give you access to your credit information, often for free, so you can actually see what’s going on. No more guessing games, no more feeling like you’re flying blind. You can see the report, understand the factors influencing your score, and get tips on how to improve it.

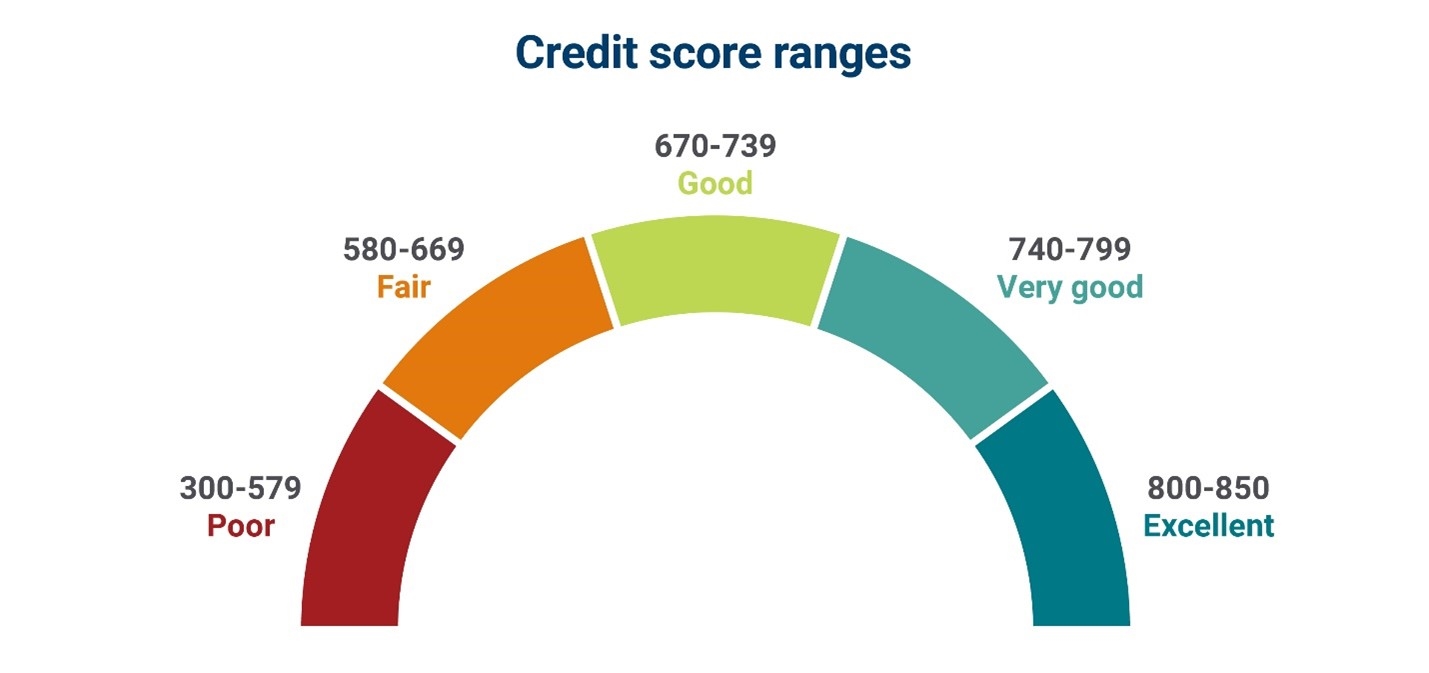

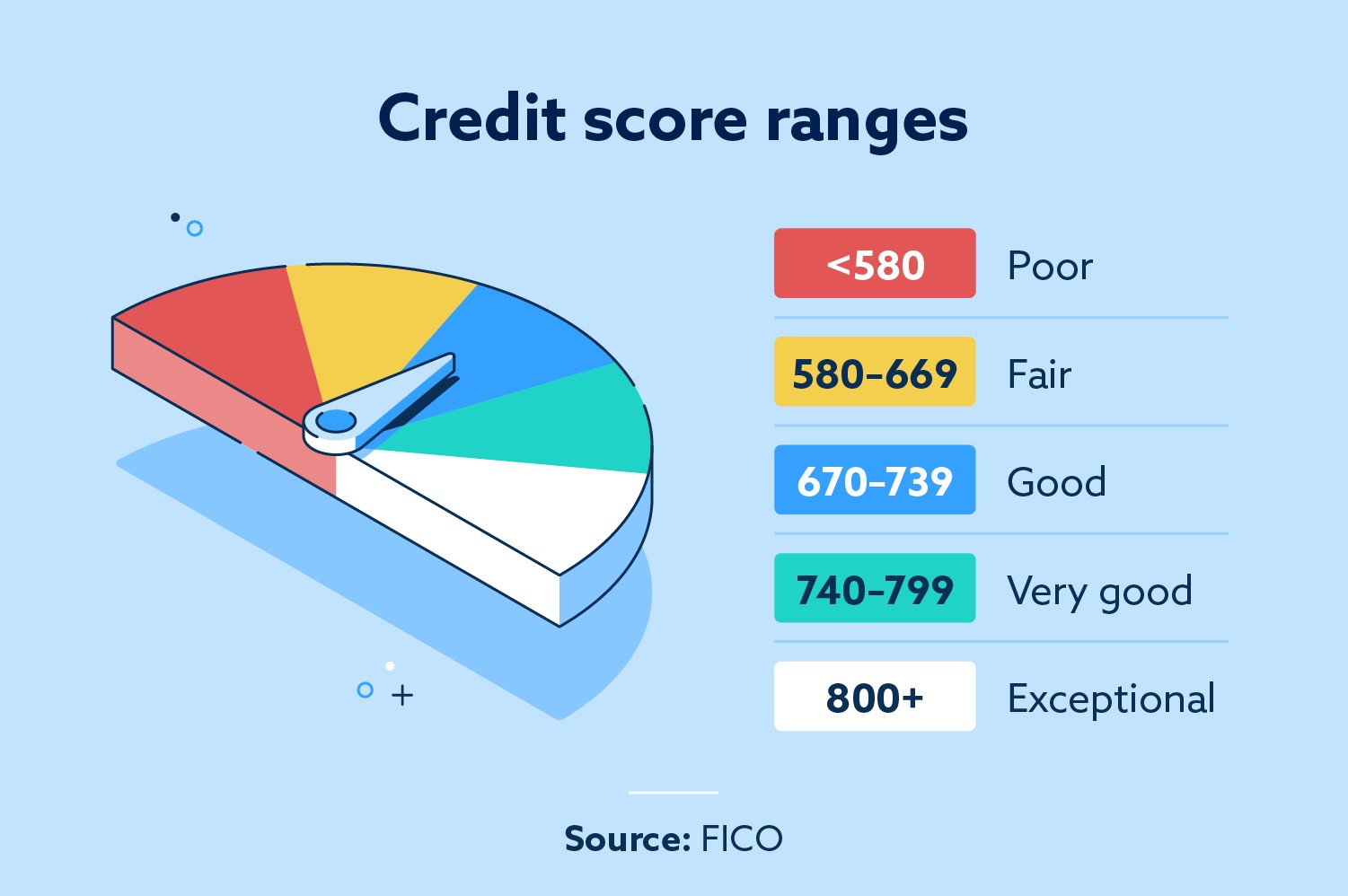

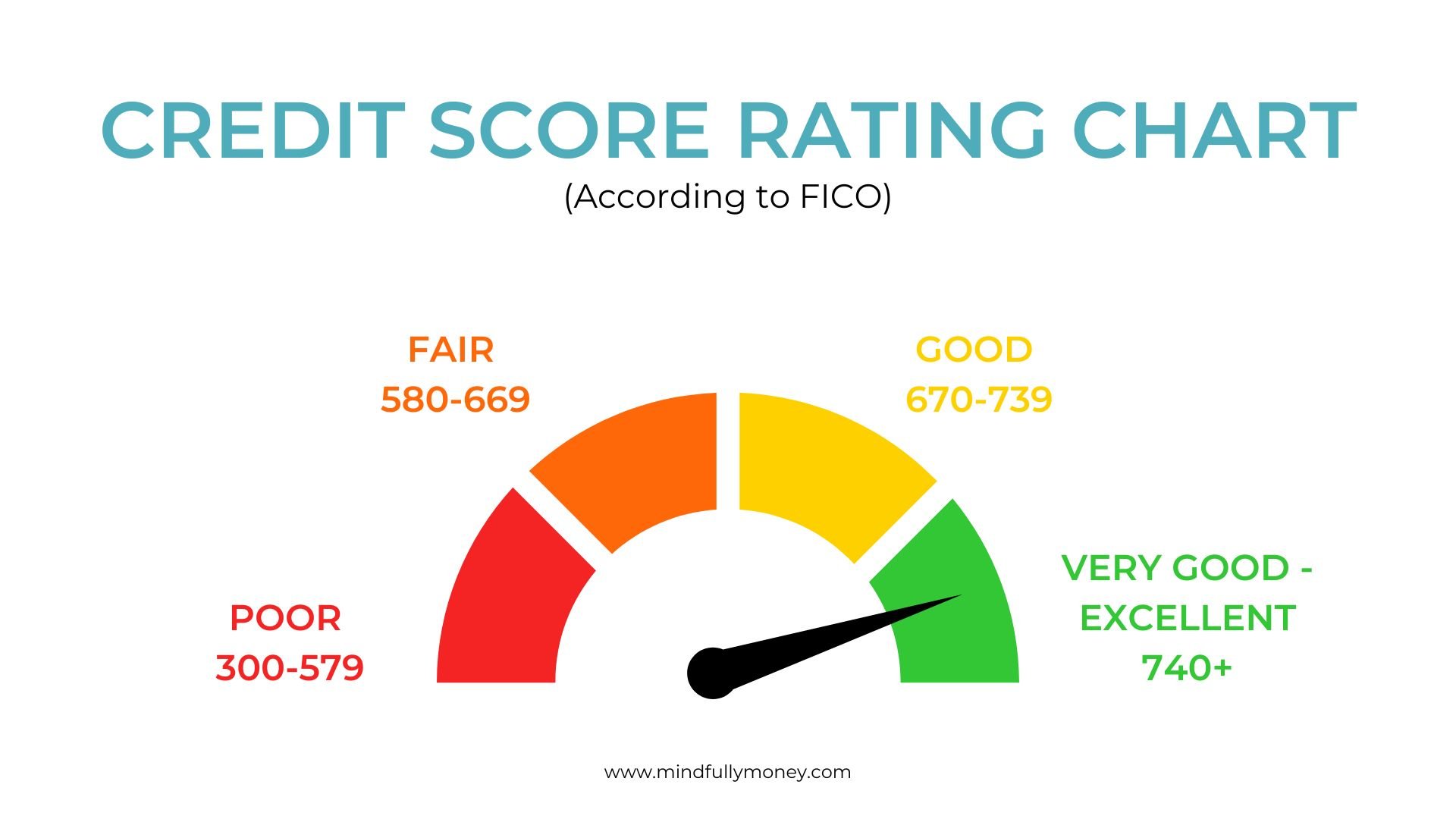

So, what’s a “good” credit score? This is the million-dollar question, right? The answer, frustratingly, isn’t a simple number that applies everywhere. Different credit reference agencies in different countries (and even different lenders within the same country) might use slightly different scoring models. But generally speaking, we can break it down into some broad categories.

The Spectrum of Scores: Where Do You Stand?

Imagine a scale. On one end, you’ve got scores that might be considered “poor” or “fair.” These can make it difficult to get approved for credit, or you might end up with higher interest rates if you are approved. On the other end, you’ve got scores that are “excellent.” These open doors, get you the best deals, and make lenders feel all warm and fuzzy about you.

With Clear Score, you’ll typically see a range. For example, in the UK, a score between 0-700 might be considered developing, 701-850 is good, and 851-950 is excellent. These are just general guidelines, mind you. Your mileage may vary!

So, what’s the magic number? Generally, a score of 650 and above is often considered a decent starting point. It shows you’re not a major risk. But if you’re aiming for the really good stuff, think 700 and upwards. That’s when you start unlocking better interest rates on mortgages, car loans, and more favorable terms on credit cards.

And then there’s the holy grail: an “excellent” credit score. This is typically in the high 800s or even 900s. With a score like this, you’re practically a financial superhero. Lenders will be falling over themselves to offer you their best products. You’ll get approved for the fanciest loans, the lowest interest rates, and maybe even a free unicorn.

It's important to remember that Clear Score (and other similar services) often uses a slightly simplified scoring system, which is great for understanding! They aim to make it accessible. The actual scores used by lenders might be a touch more complex, but Clear Score gives you a really solid foundation.

Why Does Your Score Even Matter? (Besides Bali Car Rentals)

Okay, so Sarah’s car rental is just one anecdote. But the impact of your credit score stretches way beyond holiday wheels. Think about it:

- Loans: Whether it’s a mortgage to buy your dream home, a loan for a new car, or even a personal loan to consolidate debt, your credit score is a major factor in getting approved and the interest rate you’ll pay. A good score can save you thousands over the life of a loan. Seriously.

- Credit Cards: Want a rewards credit card with amazing perks? Or perhaps a balance transfer card to save on interest? A good credit score is usually a prerequisite.

- Renting Property: Landlords often run credit checks to see if you’re likely to pay your rent on time. A solid score can make you a more attractive tenant.

- Mobile Phone Contracts: That shiny new smartphone you’ve been eyeing? Getting it on a monthly contract often involves a credit check.

- Utilities and Services: In some cases, providers of utilities (like electricity or gas) or even some insurance companies might look at your credit history.

So, it’s not just about getting approved; it’s about getting the best terms. A slightly lower score might mean you get approved, but with a sky-high interest rate that makes the debt balloon faster than you can say “oops.”

This is where Clear Score’s “fairness” comes into play. They’re democratizing access to this information. Before services like Clear Score, you might have had to pay for your credit report or navigate complex websites. Now, you can get a pretty good idea of where you stand, often with actionable advice, for free. How’s that for progress?

What Makes a Good Score? The Nitty-Gritty

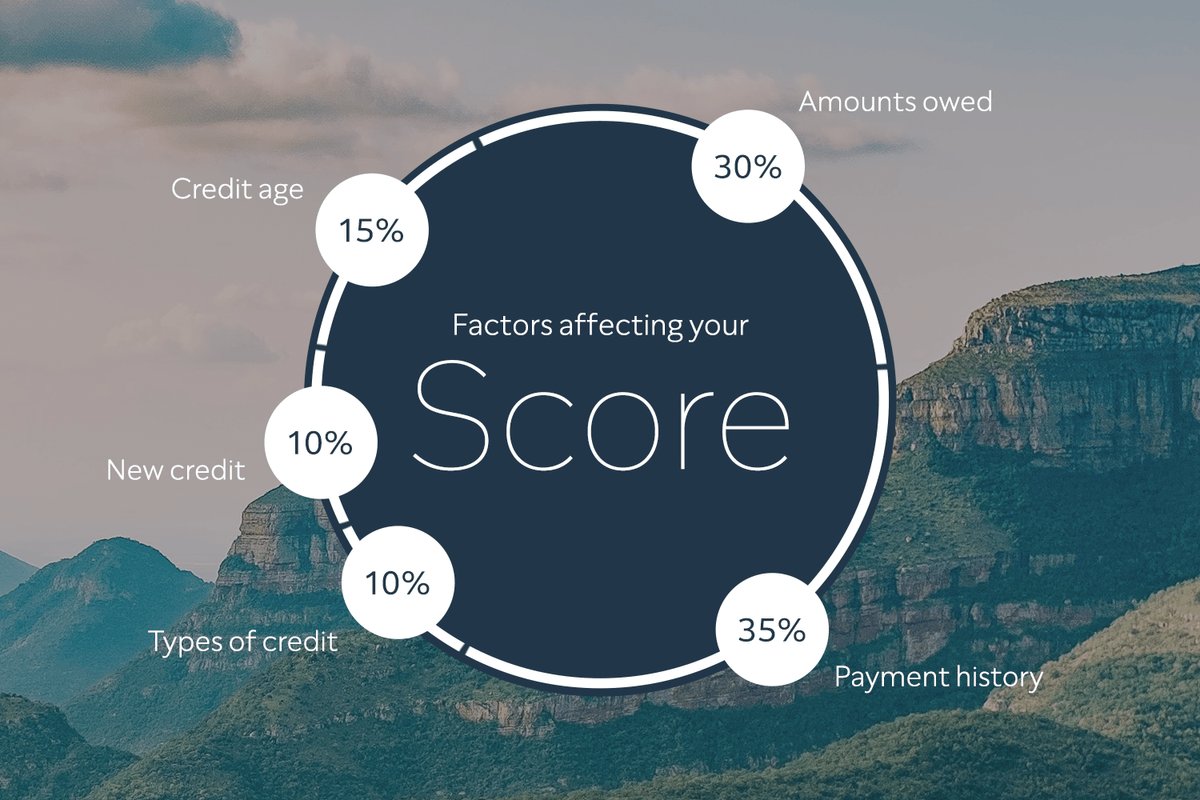

So, you know what a good score is, and you know why it matters. But what actually builds that good score? It’s not some secret formula whispered by financial gurus.

Clear Score and other services will usually break down the key factors. These are generally the same across most credit scoring models:

- Payment History: This is, hands down, the most important factor. Are you paying your bills on time, every time? This includes credit cards, loans, utility bills, etc. Late payments, defaults, and missed payments are like a big, flashing “caution” sign to lenders. Consistency is key.

- Credit Utilization: This refers to how much of your available credit you’re using. For example, if you have a credit card with a £1,000 limit and you’re consistently using £900 of it, your utilization is 90%. This is generally seen as high risk. Lenders prefer to see you using a small portion of your available credit, ideally below 30%. So, if you have a £1,000 limit, try to keep your balance below £300.

- Length of Credit History: The longer you’ve been managing credit responsibly, the better. A longer history demonstrates a track record of financial behavior. This doesn’t mean you need to go out and open a dozen accounts you don’t need, but it’s a reason to keep older, well-managed accounts open.

- Credit Mix: Having a mix of different types of credit (e.g., a credit card, a mortgage, a personal loan) can be beneficial, as it shows you can manage various financial products responsibly. However, don’t take out loans you don’t need just to improve your mix!

- New Credit: While opening a new account can be good for your credit mix, opening too many new accounts in a short period can signal desperation or increased risk. Lenders see this as you trying to borrow a lot of money quickly.

Clear Score often presents this information in a visual way, which is super helpful. You can see which areas are strong and which might need a little TLC. It’s like getting a personalized action plan for your finances.

What If My Score Isn't Great? (Don't Panic!)

So, let’s say you check your Clear Score and it’s not quite where you want it to be. Maybe Sarah’s Bali dreams feel a million miles away. Here’s the good news: your credit score is not set in stone. It’s dynamic, and you have the power to improve it.

Here are some practical tips that Clear Score often reiterates:

- Pay Your Bills on Time: This is the absolute non-negotiable. Set up direct debits, reminders, whatever you need to do. Make sure every payment is made by the due date.

- Reduce Your Credit Utilization: If you have credit card balances, focus on paying them down. Aim to keep your balances low relative to your credit limits.

- Check Your Credit Report for Errors: This is crucial! Sometimes, mistakes happen. Incorrect information on your credit report can drag your score down. Clear Score allows you to see your report, so you can spot any inaccuracies and dispute them. It’s worth doing this regularly.

- Avoid Opening Too Many New Accounts: Be strategic about applying for new credit. Only apply when you genuinely need it.

- Stay on the Electoral Roll: This is a simple one, but it helps lenders verify your identity and address.

- Be Patient: Improving your credit score takes time. There’s no magic wand. Consistent responsible behavior over months and years is what truly builds a strong score.

Think of it like building muscle. You don’t get ripped overnight. It requires consistent effort, the right exercises (financial habits), and a good diet (managing your money wisely). Clear Score is like your personal trainer, giving you the insights and the motivation.

It's also worth noting that the type of credit that Clear Score focuses on can vary slightly. In the UK, for example, Clear Score primarily looks at your credit file with Experian. Other services might use different credit reference agencies like Equifax or TransUnion. So, while the general principles are the same, the exact numbers and reports might differ slightly.

Clear Score: Your Ally in Financial Literacy

What I really appreciate about services like Clear Score is their commitment to financial education. They don't just show you a number; they try to explain what it means and how you can influence it. This is so important because, for many people, financial literacy isn't something that's taught in schools. We’re often left to figure it out as we go along.

When Sarah asked me about her credit score, I realized how many people are in the same boat. They understand the concept vaguely but lack the practical knowledge. Clear Score bridges that gap. It’s like having a friendly guide who’s holding a flashlight in the sometimes-dark world of credit.

And the fact that it’s free? That’s a game-changer. It removes a significant barrier to entry. You can monitor your progress, understand your financial health, and make informed decisions without having to open your wallet. It’s empowering.

So, to circle back to Sarah’s Bali predicament: a good credit score, as shown by Clear Score, would have meant she could have booked that rental car with confidence, and probably at a better rate too. Instead of a last-minute panic, it would have been a seamless part of her holiday planning.

What’s considered a “good” credit score with Clear Score is generally anything that puts you in the “good” or “excellent” categories. Aiming for that 700+ mark is a solid goal. But remember, it’s a journey. Start by understanding your current score, identifying areas for improvement, and then consistently taking those steps. You’ll be surprised at how much your financial well-being can improve, opening up more opportunities – for Bali adventures and beyond!

Don’t let the mystery of credit scores hold you back. Take a look at Clear Score, get informed, and start building that financial future you deserve. You’ve got this!