What Is A Balloon Payment On A Car

Hey there! So, you're thinking about a new set of wheels, huh? Awesome! Buying a car is super exciting, right? But then you hear all these fancy finance terms thrown around, and your brain does a little flip. One of those terms you might stumble across is a "balloon payment." Sounds kinda… dramatic? Like something that’s going to pop and ruin your day? Haha, not quite! But it’s definitely something to get your head around before you sign on the dotted line.

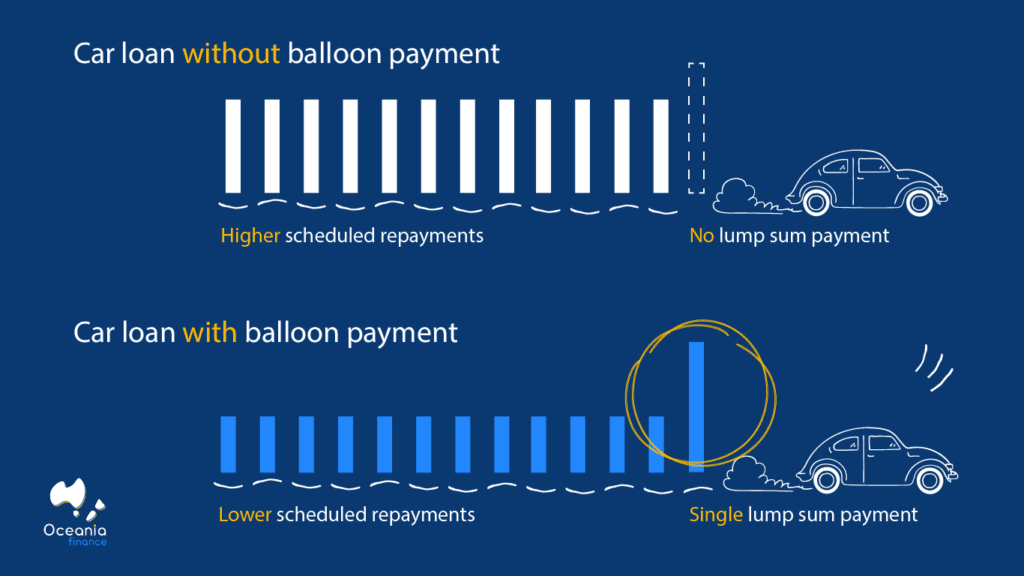

Think of it like this: you know how when you’re planning a big party, you might have some smaller costs leading up to it, and then the big catering bill lands right at the end? A balloon payment on a car loan is a bit like that, but for your car. It’s a way of structuring your loan where you have smaller, regular payments for most of the loan term, but then a large, lump sum payment is due at the very end. Pretty neat, huh?

So, What's the Big Idea Behind It?

Why would anyone want a giant payment hanging over their head at the end? Good question! The main reason is to lower your monthly payments. If you’re someone who likes to have a bit more breathing room in your budget each month, this could be your jam. By pushing a significant chunk of the total loan amount to the end, your regular installments become way more manageable. It’s like tricking your wallet into thinking you’re paying less! Sneaky, I know.

Must Read

Imagine you’re buying a car that costs, say, $30,000. If you took out a regular loan, your monthly payments might feel a bit… oof. But with a balloon payment plan, your monthly payments could be significantly lower, maybe closer to what you’d pay for a much cheaper car. You’re essentially borrowing less initially against the car’s value, with the understanding that you’ll sort out the rest later. It’s like a financial magic trick, but you gotta be ready for the grand finale!

Who Is This For, Anyway?

This kind of loan isn't for everyone, obviously. It's best suited for people who have a pretty solid plan for that big payment down the road. For example, maybe you know you’ll be getting a nice bonus in a couple of years, or you’re planning to sell the car before the balloon payment is due. Or perhaps you're a business owner who expects a big influx of cash at a certain time.

It’s also popular with people who tend to upgrade their cars frequently. Let’s say you love having the latest model every three years. A balloon payment can make the monthly costs of driving a new car now much more affordable. You might be planning to trade it in for a new one before that big payment ever hits. It’s like a really fancy, four-wheeled rental with an option to buy… kinda. You get the gist!

How Does It Actually Work, Step-by-Step?

Okay, let’s break it down a bit more. So, you’ve got your car, let’s stick with that $30,000 example. You agree on a loan term, maybe four years. But instead of dividing the whole $30,000 (plus interest) into 48 equal payments, you and the lender agree that a portion of it, let’s say $10,000, will be the balloon payment due at the end of those four years. This means you're only financing $20,000 for your monthly payments.

So, your monthly payments will be calculated based on that $20,000. That’s going to be a lot less than if you were paying off the full $30,000, right? You’ll be making these smaller, sweet-sounding payments for the entire loan term. And then, BAM! At the end of those four years, you’ve got that $10,000 balloon payment staring you down. You'll need to have that cash ready, or arrange to refinance the remaining balance.

The Payment Breakdown: Smaller Bills, Bigger Finish

So, in a nutshell, you're paying off the depreciation of the car (how much value it loses over time) plus interest, rather than the entire purchase price. The balloon payment represents the estimated residual value of the car at the end of your loan term. It's like saying, "I'm borrowing this car, I'll make regular payments while I use it, and at the end, I'll either pay you its estimated value, or you can take it back." Well, not exactly take it back in most cases, but you get the idea. You’re responsible for that estimated future value.

It's a bit like a lease, but you technically own the car throughout the loan. You're just structuring the payments differently. And that’s the key difference! With a lease, you never own it. With a balloon payment, you do own it, but you're deferring a big chunk of the cost. It’s a subtle but important distinction!

The Good Stuff: Why It Might Be Awesome

Let’s talk about the perks, because there are definitely some! The most obvious one, as we’ve chatted about, is those lower monthly payments. Who doesn’t love saving a bit of cash every month? It frees up your budget for, you know, actual fun stuff. Like avocado toast. Or emergency pizza funds. Or, you know, other bills.

It can also help you afford a nicer car than you might otherwise be able to. That dream car that seemed completely out of reach? A balloon payment might just bring it down to earth. You can drive a car that feels a bit more luxurious or has more features, all while keeping your monthly outgoings manageable. It’s like getting a little upgrade in your daily life without breaking the bank… for now.

And for those of you who are serial car upgraders, it’s a dream come true. You get to enjoy a new car every few years, and because you’re trading it in before the balloon payment is due, you never actually have to pay it. You just roll that into your next car purchase, or use the trade-in value to offset the new loan. It’s a cycle of automotive happiness! Or, you know, just a cycle.

The Not-So-Good Stuff: The Elephant in the Room (or Garage)

Okay, time for the reality check. That big balloon payment? It’s real. And it can be a bit of a shock if you haven’t planned for it. It’s like the final boss battle of your car loan. You gotta be prepared. If you haven’t saved enough or can’t refinance, you could be in a pickle. A really expensive pickle.

The total interest paid over the life of the loan can also be higher. Since you're paying off less principal each month, more of your payment goes towards interest. Over time, this can add up. So while your monthly payments are smaller, you might end up paying more overall for the car compared to a traditional loan. It’s a bit of a trade-off, isn’t it?

Also, what if the car’s value at the end of the loan term is less than the balloon payment amount? This can happen if the car depreciates faster than expected, or if you've put a lot of miles on it, or, you know, if you’ve accidentally driven it into a ditch. (Please don’t do that!) In that situation, if you sell the car, you might not get enough to cover the balloon payment. Then you're still on the hook for the difference. Ouch. Nobody wants that!

So, When Should You Consider It?

If you’re the type who loves to have a new car every few years and always trades in before the loan is up, a balloon payment could be a smart move. You can enjoy lower monthly costs and always drive something fresh. It’s like a continuous car refresh cycle.

Or, if you’re self-employed or a business owner and you know you’ll have a significant cash injection coming in at a specific time in the future, this could be perfect. You can manage your cash flow now and then make that big payment when you have the funds readily available. It’s all about timing!

Also, if you're looking to reduce your monthly outgoings significantly for a period, and you have a solid plan for that final payment. Maybe you're saving up for a house deposit and need to free up cash for a few years. This could be a temporary solution. Just make sure that "solid plan" is really solid. No winging it allowed here!

When to Steer Clear (Unless You Like Risks!)

If you're the kind of person who likes to pay off their debts completely and have that feeling of financial freedom, a balloon payment might just give you anxiety. That final payment can feel like a looming storm cloud.

If you're not sure about your future financial situation, it’s probably best to avoid it. Life happens, and unexpected expenses can pop up. If your income is a bit unpredictable, that big final payment could be a real problem.

And if you're planning to keep the car for a long time, this is probably not the loan for you. You’ll end up paying a lot more interest, and you’ll still have that big lump sum to deal with eventually. It just doesn't make as much sense in the long run if you’re planning on being a long-term car owner.

The Alternatives: Other Ways to Finance Your Ride

Don’t worry, if a balloon payment sounds a bit too much like a financial tightrope walk, there are other options! The most common is a traditional car loan. This is where you borrow the full amount and pay it off in equal installments over the loan term. Simple, straightforward, and you know exactly what you’re paying each month.

Then there’s leasing. As we touched on, with a lease, you’re essentially renting the car for a set period and mileage allowance. You make monthly payments, and at the end, you just hand the car back. No balloon payment, no ownership worries. But, you don’t own it either, and you can’t customize it like you own it. It's like a really fancy, long-term car rental.

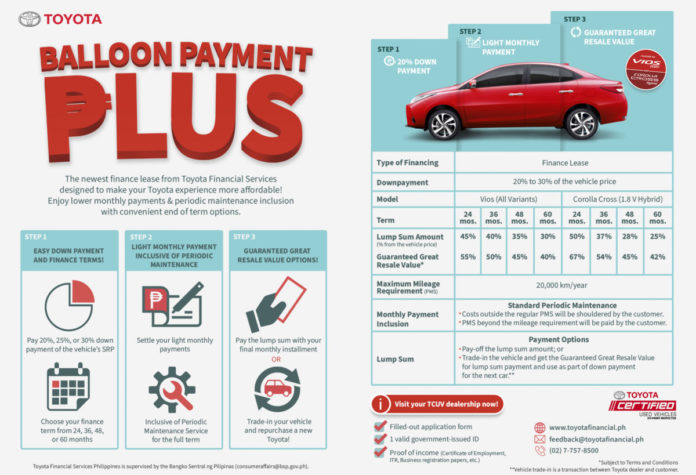

Some dealerships might also offer personal contract purchase (PCP) deals, which can sometimes include a balloon payment structure similar to what we've discussed, but are often presented with a slightly different marketing spin. They might be geared towards making monthly payments low and offering a guaranteed future value (GFV) of the car, which acts much like a balloon payment.

Making the Smart Choice for You

Ultimately, the best way to finance your car depends on your individual circumstances and your financial goals. There's no one-size-fits-all answer! Do your homework, crunch the numbers, and talk to a financial advisor if you’re unsure. It’s always better to be overprepared than to be surprised by a massive payment you weren’t ready for.

A balloon payment can be a great tool for managing your budget and driving a car you love, but only if you have a clear plan for that final, big payment. Think of it as a carefully orchestrated financial symphony – the crescendo at the end needs to be planned for, or it can sound a bit… off-key. So, weigh up the pros and cons, and drive off into the sunset with confidence, knowing you’ve made the right choice for your wallet!