What Does An Underwriter Do For A Home Loan

So, you’re thinking about buying a house? Awesome! It’s a huge step. And chances are, you'll need a home loan. That's where these mysterious folks called underwriters come in. What do they even do? Let's dive in, shall we?

Think of an underwriter as the detective of the mortgage world. Not the trench-coat-and-magnifying-glass kind, though. More like a super-organized, numbers-crunching superhero.

Their main gig? To decide if you’re a good bet for a loan. They’re basically saying, "Can this person handle paying back all this money over, like, 30 years? And will they actually pay it back?"

Must Read

It’s kind of like when you lend your best friend your favorite hoodie. You trust them, right? But maybe you still give them a little mental checklist: "Okay, so they've always returned my stuff before. They have a steady job. They don't have a history of, you know, setting hoodies on fire."

The Underwriting Deep Dive

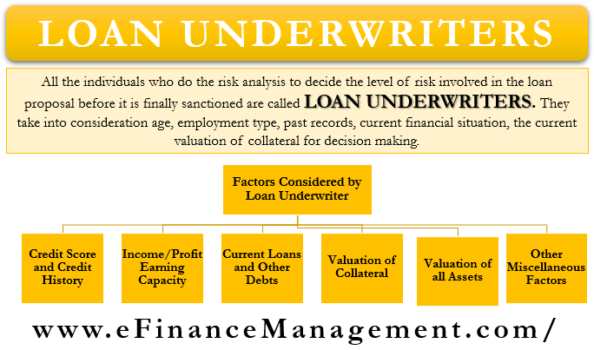

An underwriter looks at a ton of stuff. It's not just a quick peek. They’re going deep. Like, really deep.

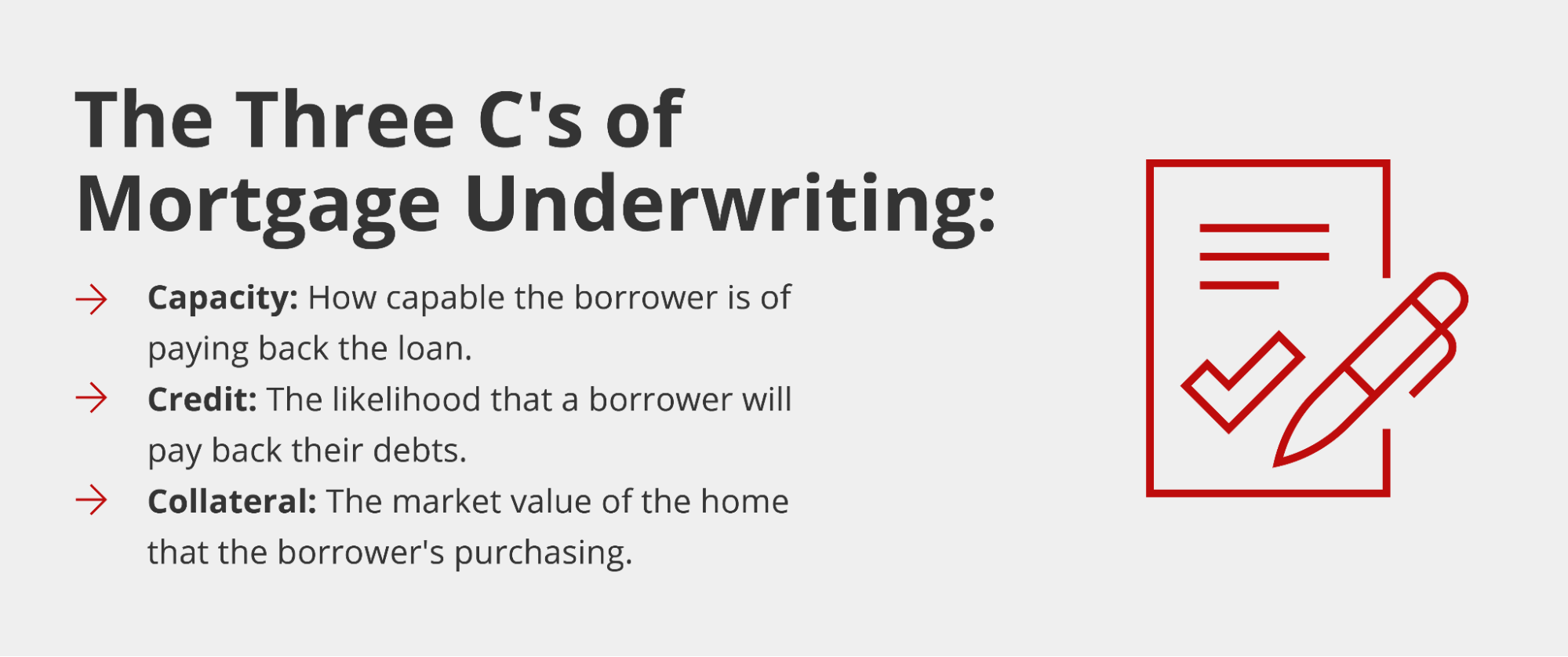

First up: Your credit score. This is your financial report card. A good score says, "Hey, I'm responsible with money!" A not-so-good score might raise a tiny eyebrow. It's like the underwriter seeing a history of on-time payments and thinking, "Ooh, a responsible spender!"

Then there’s your income and employment history. Are you working? For how long? Is your job stable? They want to see that you’re not going to suddenly decide to become a professional llama groomer in a remote mountain village next week. Unless, of course, llamas are suddenly worth a fortune. You never know!

They’ll also scrutinize your debt-to-income ratio. This is a fancy way of saying how much of your money is already spoken for by other bills. If you’re drowning in credit card debt and car payments, it’s harder to take on a big mortgage payment. It’s like trying to balance a giant pizza on your head while juggling water balloons. Ambitious, but maybe not the wisest.

And don't forget your assets! This includes your savings, investments, and any other cash you have lying around. This is your cushion. It shows you’ve got some backup if things get a little bumpy. Think of it as your financial emergency parachute.

The Quirky Side of Underwriting

Here's where it gets fun. Underwriters aren't just looking at spreadsheets. They're often looking for little red flags, or sometimes, just funny quirks.

Ever had a job where you were paid in… well, let’s just say unconventional ways? An underwriter might scratch their head a bit. If your income is mostly tips from a juggling act at a circus, they might need some extra proof. They're not judging, just trying to understand.

What about that side hustle? Selling artisanal pickles on Etsy? They’ll want to see that it’s generating real income, not just costing you money in fancy jars. Unless those jars are really fancy.

And sometimes, there are just weird… things. Like a sudden, unexplained deposit of a large sum of cash. Did you win the lottery? Find a buried treasure chest? The underwriter needs to know. They’re basically asking, "Where did this money come from, and can we trust it?" They’ve seen it all, from inheritance windfalls to suspiciously large birthday gifts.

One thing they really hate? Big, unexplained cash deposits right before you apply for a loan. It looks like you’re trying to hide something. So, if you suddenly inherit a briefcase full of money, maybe have a good explanation ready! Or at least a very believable story about a wealthy, eccentric aunt.

The Underwriter's Toolkit

These folks have a whole arsenal of tools at their disposal. They don't just take your word for it. They verify, verify, verify!

Verification of Employment (VOE): They'll call your employer to confirm you actually work there and are still employed. So, make sure your boss is expecting that call and doesn't think it's a prank!

Bank Statement Analysis: They'll pore over your bank statements. Are your deposits consistent? Are there any weird bounced checks? They’re looking for stability, not a financial roller coaster.

Appraisal Report: This is about the house itself. Is it worth what you're paying for it? An appraiser will check out the property to make sure the bank isn't lending you too much money for a house that’s secretly a haunted gingerbread cottage.

Title Report: This checks for any liens or claims on the property. Basically, they're making sure the seller actually owns the house fair and square and isn't going to show up later with a claim of ownership based on a childhood promise.

Why Do We Even Need Underwriters?

It might seem like a lot of fuss. But think about it. A mortgage is a huge loan. Like, really huge. Banks and lenders are lending out millions, even billions. They need to be sure they're going to get their money back.

Underwriters are the gatekeepers. They protect the lender from taking on too much risk. And in turn, they protect you from taking on a loan you can’t realistically afford. It's a balance. A delicate, financial tightrope walk.

Imagine if there were no underwriters. Everyone could get a loan for anything! We’d all be buying mansions with salaries from our pet rock collection. The economy would probably look… different. And not in a good way. Probably a lot of sad bankers and very confused homeowners.

The "Yes" or "No" Decision

After all that digging, the underwriter makes a decision. It's usually one of three things:

Approved! Woohoo! You did it! The house is yours (well, you’re on the path to owning it).

Approved with Conditions. This means you're almost there. But you need to do a few more things. Maybe provide an extra document, or explain a specific transaction. It’s like getting a "yes" on a date, but they say, "Sure, but maybe wear a different shirt."

Declined. Bummer. It’s not the end of the world, though. Sometimes it means you need to work on your credit, save more, or tackle some debt first. It's a "not yet," not a "never." Think of it as a temporary detour.

So, there you have it! The wonderful, the weird, and the undeniably important world of mortgage underwriting. They’re the unsung heroes (or villains, depending on your perspective) making sure the dream of homeownership is built on a solid financial foundation. Pretty fascinating, right?