What Credit Rating Do I Need For A Mortgage

Buying a home is a dream for many, and figuring out what credit score you need for a mortgage can feel like unlocking a secret level in a video game. It's not as scary as it sounds, and understanding your credit rating is actually a super useful skill that can save you a lot of money and hassle down the line. Think of it as your financial report card, and a good one opens doors to better homeownership opportunities!

So, who’s this all for? If you're a beginner stepping into the world of home buying for the first time, this is your essential guide. Knowing your credit score upfront means you can start setting realistic goals and understand what you need to aim for. For families thinking about upgrading to a bigger place or finding a home with a yard for the kids, a good credit score can mean a lower monthly payment, freeing up more cash for family adventures. And even if you're not actively buying right now, understanding credit scores is a great hobby to pick up – it’s empowering to be in control of your financial future!

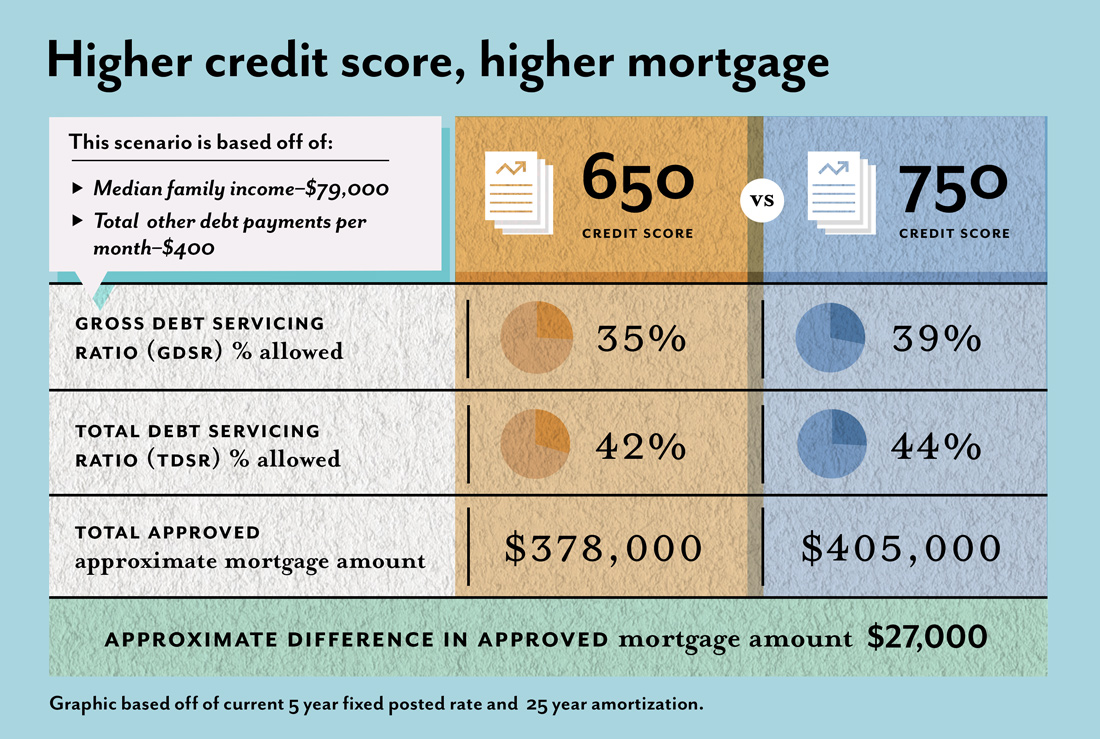

Let’s dive into the numbers. Generally, lenders look for a credit score of around 620 or higher to qualify for most conventional mortgages. However, this is just a starting point. A score between 670 and 739 is considered good and will likely get you better interest rates. If you're aiming for the stars with a score of 740 and above, you’re in the excellent category, which often unlocks the best loan terms and lowest interest rates. Don't despair if your score is a bit lower! There are options like FHA loans, which can be more forgiving and might allow scores as low as 500 with a larger down payment. So, it's not just one magic number; there are variations and pathways for different situations.

Must Read

Ready to get started? It's easier than you think! First, check your credit report. You're entitled to a free report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once a year at AnnualCreditReport.com. Take a peek at it to make sure everything is accurate. Then, calculate your credit score. Many credit card companies offer free access to your score, or you can use various online tools. Once you know where you stand, identify any areas where you can improve. Are there late payments? High credit card balances? Focus on paying bills on time and reducing your debt. Even small improvements can make a big difference.

Ultimately, understanding your credit score is a rewarding journey. It empowers you to make informed decisions about your finances and brings you one step closer to your dream home. It’s a fantastic feeling to know you’re on the right track, and that knowledge is truly valuable!