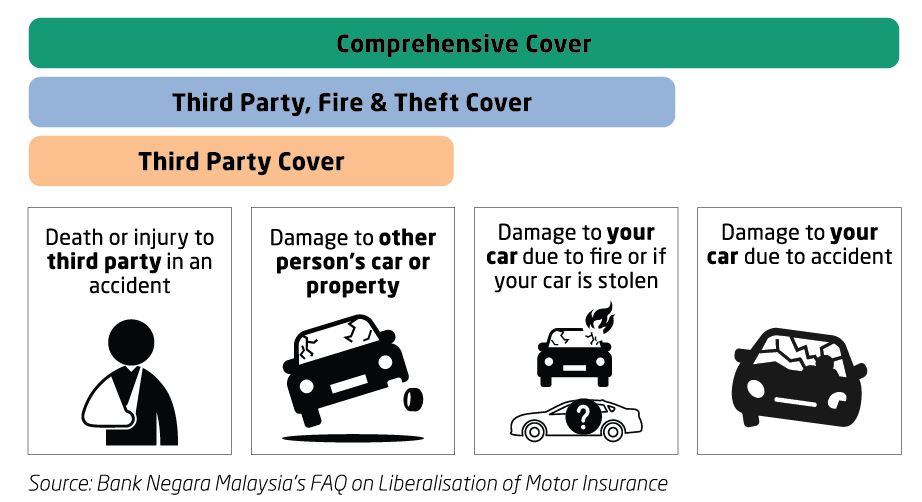

Third Party Fire And Theft Vs Comprehensive

Alright, let's talk about car insurance. Sounds about as exciting as watching paint dry, right? But stick with me, because this is one of those grown-up things that, when you actually get it, makes your life a whole lot smoother. Think of it like choosing your socks for the day. You can go with the plain old black ones that just… exist, or you can opt for something with a bit more personality and, dare I say, protection. That's kind of how Third Party Fire and Theft and Comprehensive insurance roll.

We've all been there. You're cruising down the road, maybe jamming to your favorite 80s power ballad, and suddenly you see it. That one pothole that looks like it could swallow a small car. Or maybe it's that rogue shopping cart that somehow rolls its way onto the highway. Life happens, people! And sometimes, life's little curveballs can leave your trusty steed looking a bit worse for wear.

So, what's the big deal between these two insurance buddies? Let's break it down without making your brain feel like it's doing advanced calculus on a Monday morning.

Must Read

Third Party Fire and Theft: The "Just the Basics, Ma'am" Option

Imagine you're at a potluck. You bring a decent, reliable potato salad. It's good, it does the job, and people appreciate it. That's your Third Party Fire and Theft insurance. It's the bare minimum, the essential. It covers you if your car, through no fault of your own (well, not directly your fault, anyway), decides to spontaneously combust like a bad movie stunt gone wrong, or if it decides to take an impromptu trip to the land of stolen goods. Think of it as your car's bodyguard, but only for specific, dramatic events. And importantly, it also covers you if you, by some unfortunate circumstance, manage to bash into someone else's car or their prize-winning garden gnome. Your policy is there to sort out their mess, not yours.

So, if you accidentally back into Mrs. Higgins' perfectly manicured rose bushes (she'll never forgive you, but your insurance will help pay for the therapy for her roses), or if your car decides to become a temporary home for a bunch of joyriders who then decide to… redecorate it with their questionable artistic choices (i.e., steal it), Third Party Fire and Theft has your back. It's like saying, "Okay, I'll take responsibility for any chaos I cause to others, and if my car gets torched or nicked, that's covered too."

It's a popular choice, especially for older cars that aren't worth a king's ransom. You wouldn't insure a flip phone for a million dollars, right? Similarly, if your car has seen better days and its market value is less than the cost of a fancy avocado toast, this option makes a lot of sense. It’s the sensible grown-up choice when you don't want to break the bank but still want a little bit of peace of mind.

Think of it like this: you're buying a lottery ticket. Third Party Fire and Theft is like buying a ticket that says, "If I win, I'll give you a cut, and if my ticket spontaneously catches fire or gets stolen, I'm covered." It’s not the full jackpot of protection, but it’s a decent scratch-off.

Comprehensive: The "Everything But the Kitchen Sink" Deal

Now, Comprehensive insurance. This is where things get fancy. This is the premium package. This is like bringing a gourmet, five-course meal to that potluck. It covers everything that Third Party Fire and Theft does, plus a whole lot more. It’s your car's all-inclusive resort package. If your car gets damaged, stolen, or catches fire – yep, still covered. But it also steps in when you, for example, misjudge that turn into your driveway and scrape your entire side mirror off on the garage door. Ouch. Or when a rogue hailstorm decides to turn your car’s hood into a miniature golf course. Or when a deer, with eyes bigger than its stomach, decides your car looks like a tasty snack and leaps onto your hood like it's auditioning for a nature documentary.

This is the insurance that says, "Whatever life throws at my car, be it from another driver, the elements, or just sheer bad luck, I want it fixed." It's the insurance for when you want to sleep soundly at night, knowing that if your car gets vandalized by disgruntled squirrels with a penchant for spray paint, or if it gets submerged in a sudden flash flood (because, let's face it, that happens!), you’re not left holding the metaphorical, soggy car keys.

Picture this: You’re at the supermarket, and as you’re wrestling with a particularly stubborn lid on a jar of pickles, you accidentally fling it. It flies through the open window of your car, lands on your dashboard, and somehow shorts out your entire infotainment system. Next thing you know, your car is making bleeping noises that sound like a dying robot. With Comprehensive, that pickle-induced electronic apocalypse is covered. With Third Party Fire and Theft? Well, you might be learning how to navigate with a paper map again.

It's like having a superhero for your car. If it gets hit by a meteor (highly unlikely, but you never know with Mother Nature!), or if it gets kidnapped by aliens and returned with a strange, glowing antenna, Comprehensive has your back. It’s the ultimate peace of mind, especially if you have a newer or more expensive car that you’d hate to see fall into disrepair due to something completely out of your control. It’s the "what if" insurance, covering those "what ifs" that you haven't even thought of yet, like your car getting pecked by a flock of angry geese.

Here's the Scoop: When to Choose Which

So, how do you decide? It really boils down to your car and your comfort level with risk. Let’s play a little game of "Would You Rather."

Would you rather:

a) Have a car that’s older than your favorite pair of jeans, has a few dings and dents that give it character (like battle scars from surviving the morning commute), and you’re not too fussed if it’s stolen or goes up in smoke (because let’s be honest, it’s probably seen enough drama already)? Then Third Party Fire and Theft might be your jam. It's like a good, sturdy umbrella – it’ll keep the main downpours off, but it might not stop you from getting a little splash if a truck drives by.

b) Have a shiny, relatively new car that you’ve basically bonded with, a car that makes you feel a little pang of sadness if it even gets a minor scratch? Or perhaps you live in an area where your car is more likely to be a target for petty thieves than a prize-winning pumpkin at a local fair? In that case, Comprehensive is probably your best bet. It’s like wrapping your car in bubble wrap, but in an insurance policy form. It’s the "I want to sleep through the night without worrying about my car" option.

Think about your car's personality. Is it a reliable old workhorse that's seen it all and is happy to keep chugging along, even with a few more battle scars? Or is it more of a pampered pet that deserves the absolute best protection? Your car's age, its value, and your personal risk tolerance are the key ingredients here.

Also, consider your budget. Comprehensive insurance is generally more expensive because, well, it covers more. It’s like buying the full buffet versus just the salad bar. So, you'll want to weigh the cost against the potential payout and your peace of mind. Some people are happy to take on a bit more risk for a lower premium, while others prefer to pay a little more for the ultimate security blanket.

And let's not forget the little things. Sometimes, your Third Party Fire and Theft policy might have a deductible (the amount you pay out of pocket before the insurance kicks in) for fire and theft claims. Comprehensive policies will almost certainly have deductibles for all sorts of claims. So, if you're looking at the numbers, it's worth checking out what those deductibles are. You don't want to be surprised by a bill that makes your eyes water more than a strong onion.

Ultimately, the goal is to find the insurance that makes you feel secure, knowing that if something unfortunate happens to your car, you're not going to be facing a financial disaster. It's about protecting your investment, whether that investment is a vintage beetle or a brand-new SUV.

So, next time you're thinking about car insurance, don't just pick the cheapest option because it's the easiest. Take a moment, have a cuppa, and think about what you truly need. Is it the reliable potato salad, or the gourmet five-course meal? Your car, and your wallet, will thank you for it. And who knows, you might even manage a smile while you're doing it.