Proof Of Funds To Buy A House

Ever dreamt of snagging that perfect fixer-upper or a charming bungalow with a white picket fence? Well, before you start mentally decorating the living room, there's a little secret weapon you'll need: Proof of Funds. And guess what? It’s not as scary or complicated as it sounds. In fact, understanding it can be a major confidence booster on your home-buying adventure!

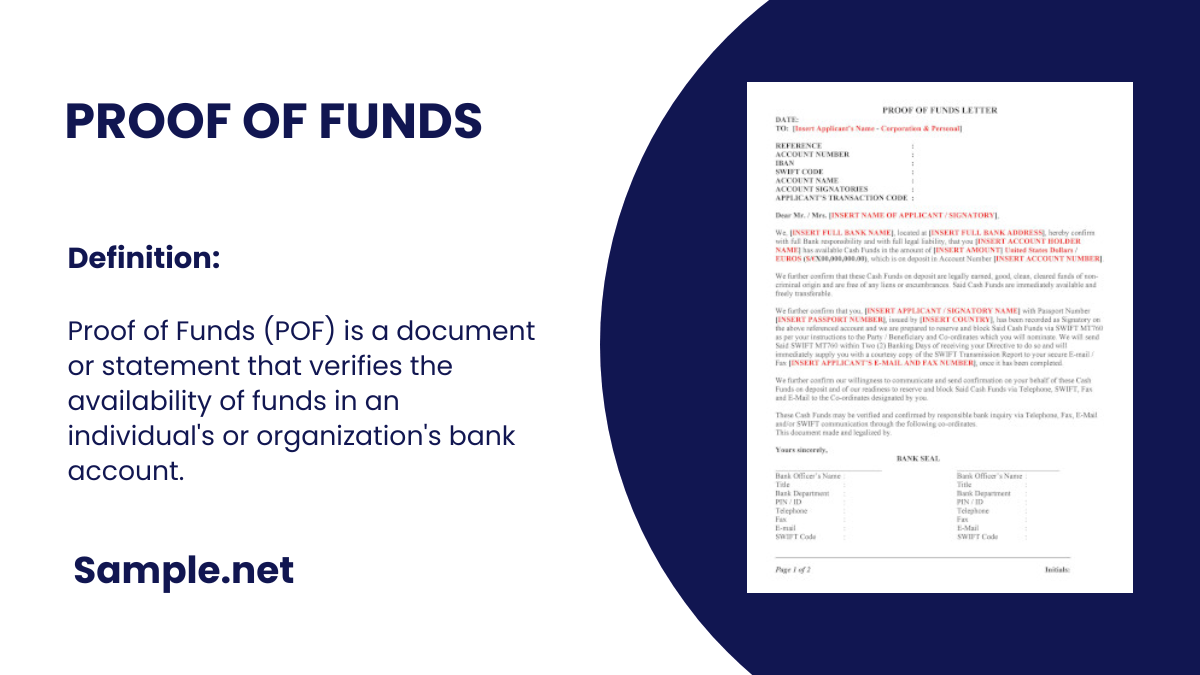

Think of Proof of Funds as your golden ticket. It’s the lender's way of saying, "Okay, this person is serious and has the actual moolah to back up their offer." It’s a document, or a collection of documents, that shows you have enough money readily available to cover the down payment and closing costs for the house you want to buy. Lenders want to see that you're not just hoping to win the lottery or relying on a surprise inheritance. They need tangible evidence that you have the financial wherewithal to make this significant purchase. It’s a crucial step in the mortgage process, and getting it sorted early can smooth out a lot of potential bumps.

Why is Proof of Funds So Important? The Lender's Perspective (and Yours!)

From a lender's point of view, Proof of Funds is all about risk management. When they lend you a large sum of money for a mortgage, they want to be as sure as possible that you can repay it. Seeing that you have a substantial portion of the purchase price (the down payment) and associated expenses (closing costs) already in the bank reassures them that you’re a reliable borrower. It significantly reduces the chance that you’ll default on your loan. They’re essentially looking for a healthy deposit, a sign of your commitment and financial stability.

Must Read

But it's not just about the lender! For you, understanding and preparing your Proof of Funds is equally beneficial.

- It Shows You're Serious: Having your finances in order demonstrates to sellers that your offer is legitimate and not just a hopeful gesture. This can give you a competitive edge, especially in a busy market where sellers receive multiple offers. A seller is much more likely to accept an offer from a buyer who has their ducks in a row.

- It Speeds Up the Process: When you're pre-approved for a mortgage, your lender will often require Proof of Funds as part of that process. Having these documents ready means you can move faster when you find "the one." No more scrambling to find bank statements when you're eager to put in an offer!

- It Prevents Surprises: Knowing exactly how much you have available helps you set realistic expectations about what kind of homes you can afford. You won't waste time looking at properties that are out of your price range. This foresight can save you a lot of emotional energy and frustration.

- It Builds Trust: Transparency with your lender and the seller builds trust. It creates a smoother, more confident transaction for everyone involved.

What Kind of "Funds" Are We Talking About?

So, what counts as valid Proof of Funds? Generally, lenders are looking for liquid assets, meaning money that's easily accessible. Here are the common players:

- Checking and Savings Accounts: These are the most straightforward. Simply provide recent bank statements.

- Money Market Accounts: Similar to savings accounts, these offer easy access to your cash.

- Certificates of Deposit (CDs): While CDs might have a slight withdrawal penalty, they are usually acceptable as proof of funds.

- Stocks and Bonds: If you have investments, you can often use them, but they might be valued at a slightly lower rate due to market fluctuations. You'll likely need to provide brokerage statements.

- Retirement Accounts (like 401(k)s or IRAs): In some cases, a portion of these might be considered, but there are often strict rules and potential penalties for early withdrawal, so this is usually a last resort or requires careful consultation with your lender.

The key here is that the funds need to be seasoned. This means they've been in your account for a reasonable period, typically a few months. Lenders want to see that the money wasn't just deposited there last week from an unknown source. If you receive a large gift from a relative to help with your down payment, for example, you'll likely need a gift letter from them, and potentially proof of where they got the money. This is to ensure it's not a loan that you'll have to repay, which could affect your debt-to-income ratio.

Think of your Proof of Funds as your financial resume for homeownership. The stronger and clearer it is, the better your chances of landing your dream home!

Navigating the world of mortgages and finances might seem daunting, but understanding concepts like Proof of Funds is a powerful step towards making your homeownership dreams a reality. So, gather those statements, chat with your lender, and get ready to make that offer!