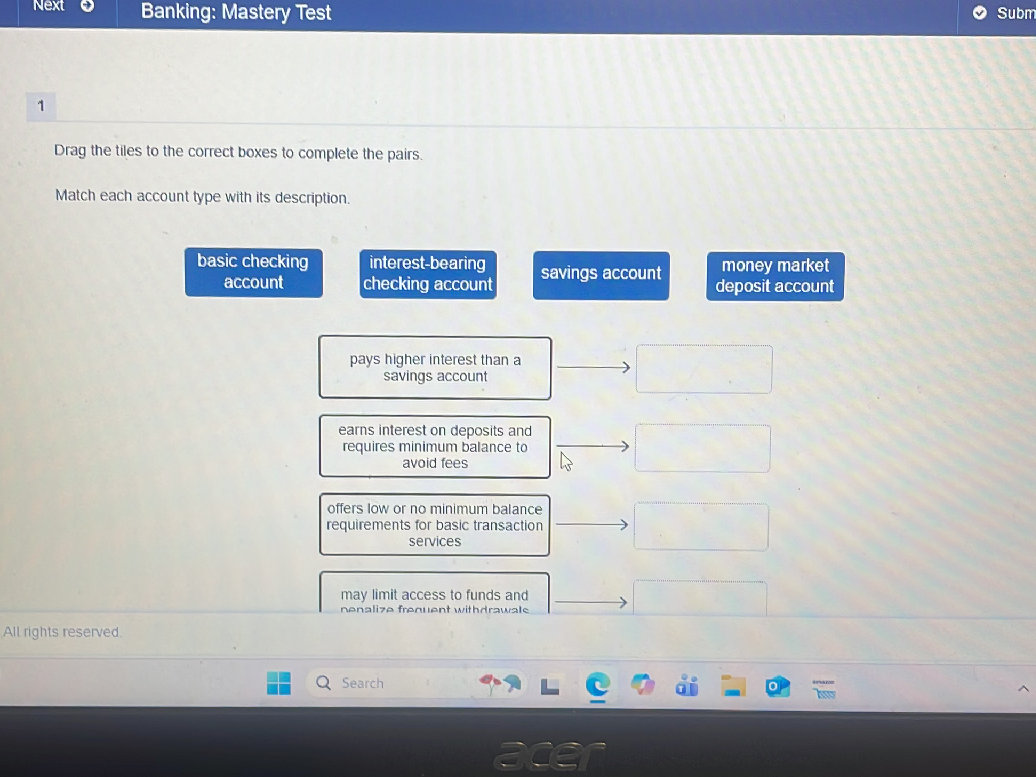

Match Each Account Type With Its Description

Hey there, fabulous humans! Let’s chat about something that might sound a little… grown-up at first glance, but stick with me, because it’s actually super handy for making our everyday lives a whole lot smoother. We’re talking about account types. Now, before you picture dusty ledgers and complicated jargon, think of it like this: your money is like a bunch of different tools in your toolbox. Some tools are for quick fixes, others are for long-term projects, and some are just for keeping things organized. Matching the right tool (or account, in this case!) to the job makes everything easier, right?

So, let’s break down these common money-friends and see where they fit best. It’s all about making your money work for you, not the other way around. Think of it like picking the perfect outfit for the occasion – you wouldn’t wear a tuxedo to the beach, and you wouldn’t wear swim trunks to a fancy wedding. Same goes for your cash!

The Speedy Saver: The Checking Account

First up, the superstar of your daily routine: the checking account. This is your go-to for, well, checking things off your to-do list! Need to grab a coffee? Pay your rent? Splurge on that amazing book you’ve been eyeing? Your checking account is there, ready and willing. It’s like your trusty sidekick, always accessible, always on the move.

Must Read

Imagine your checking account as your everyday wallet. It's where you keep the cash you need for immediate expenses. You probably have a debit card linked to it, making it super easy to tap and pay your way through life. It’s the engine that keeps your daily financial life humming along. Without it, things would get… well, complicated, like trying to buy groceries with a piggy bank full of coins!

Key takeaway: This is for your day-to-day spending. Easy access is the name of the game here. You want to be able to grab your money without a second thought.

The Little Seed That Grows: The Savings Account

Now, let’s talk about dreams. That vacation you’re planning? That down payment on a car? Or maybe just a rainy-day fund for when your washing machine decides to stage a protest? For these bigger, brighter goals, you need a savings account. This is where your money can chill out, get comfortable, and, importantly, grow a little.

Think of your savings account like a piggy bank, but with a friendly fairy godmother sprinkling a little extra magic (interest!) on it. You deposit money, and it sits there, safely earning a small return. It’s not for your daily lattes, but for the bigger splashes you want to make down the line. It encourages you to be a bit more patient, to let your money build up over time.

Picture this: you’re saving up for a new bike. Every week, you put a little bit aside into your savings account. It might not seem like much at first, but as the weeks turn into months, you’ll see that balance creep up, inching you closer to that shiny new wheels! It’s the magic of delayed gratification, powered by a sensible savings account.

Key takeaway: This is for your future goals and emergencies. It’s about building up wealth, slowly but surely. Think of it as planting a little money tree.

The Smart Investor: The Money Market Account

Okay, things are getting a little more sophisticated now, but don’t worry, we’re still keeping it breezy! The money market account is like a hybrid between your checking and savings accounts. It offers a little more flexibility than a traditional savings account while still aiming to earn a bit more interest than a standard checking account.

Imagine you have a chunk of money you want to keep relatively accessible but also want it to earn a bit more than just sitting in your checking. A money market account is like giving your money a comfortable armchair where it can relax and earn a bit of extra. You might get a debit card or check-writing privileges, but there are often limits on how often you can access the funds. It’s a good middle ground for funds you might need in the near future but don’t need instant access to every single day.

Think of it like this: you’ve just sold a bunch of old stuff online, and you have a nice sum of money. You don’t need it right now, but you might need it in a few months for a new piece of furniture. A money market account lets that money earn a little more interest while still being available when you’re ready to shop. It’s for those bigger, but not immediate, financial needs.

Key takeaway: This is for larger sums of money you want to keep accessible while earning a bit more interest. It’s a smart place for your “medium-term” savings.

The Long-Term Dream Weaver: Certificates of Deposit (CDs)

Alright, let’s talk about serious, long-term commitment. When you have money you know you won’t need for a set period – maybe a few months, a year, or even longer – and you want to get the best possible interest rate, a Certificate of Deposit (CD) is your best friend. This is where you tell your money, “Okay, buddy, you’re on a mission. Stay put for X amount of time, and I’ll reward you handsomely!”

Think of a CD like putting your money in a locked box with a timer. You agree to leave it there undisturbed until the timer goes off. In return for this commitment, the bank offers you a fixed, often higher, interest rate. The longer you commit, generally, the higher the rate you can expect. It’s perfect for money you’re absolutely sure you won’t need to touch.

Imagine you’re saving for a big purchase in five years, like a down payment on a house. You can put that money into a 5-year CD. That money is now locked away, but it’s working hard for you at a good interest rate, building up that nest egg without you being tempted to dip into it for impulse buys. It’s the ultimate in hands-off wealth building for a defined period.

Key takeaway: This is for money you won’t need for a fixed period, offering higher interest rates in exchange for locking it away. It’s the commitment-minded saver’s choice.

Why Should You Care?

So, why all this fuss about matching accounts? Because it’s all about financial peace of mind and making your money work smarter! When you use the right account for the right purpose, you:

- Earn more interest: Your savings and longer-term funds can grow faster.

- Stay organized: It’s easier to track your money when it’s separated for different goals.

- Avoid fees: Overdraft fees on checking accounts can be a real bummer! Using savings for unexpected expenses can prevent this.

- Reach your goals faster: Whether it's a vacation or a new car, having the right savings strategies helps you get there.

It’s like having a well-organized closet. When everything has its place, finding what you need is a breeze, and you feel a whole lot less stressed. Your finances should be the same! Taking a few minutes to understand these account types can literally save you money and stress in the long run. So go forth, match your money to its perfect home, and watch your financial life become a little bit more wonderful!

![[ANSWERED] Match the type of checking account with the correct - Kunduz](https://media.kunduz.com/media/sug-question-candidate/20220519221754514905-4444842.jpg?h=512)