Is It Better To Pay Off Mortgage Or Save Money

Hey there, homeowners and dreamers! Let's chat about something that pops up in so many conversations, especially around the dinner table or during those late-night "what ifs": the age-old question – should you throw every spare penny at your mortgage or stash it away in savings? It sounds like a grown-up problem, right? But honestly, it’s more like deciding whether to buy that extra slice of pizza now or save it for a really special occasion later. Both have their perks!

Think of your mortgage like a long-term commitment, a very big, very important relationship. It’s a big chunk of money you owe, and paying it off early feels like giving that relationship a big, warm hug. You get that sweet relief of being debt-free, and let’s be honest, saying "I own my home outright!" is a pretty amazing feeling. Imagine this: no more monthly mortgage payments. That money, suddenly freed up, could be your ticket to a spontaneous getaway, finally getting that vintage record player you've been eyeing, or maybe just a sigh of relief when you look at your bank account.

On the flip side, let’s talk about savings. Think of savings as your financial superhero cape. It’s there to swoop in and save the day when unexpected things happen. Your washing machine decides to stage a protest and flood the laundry room? Zap! Your car needs a surprise surgery? Pow! A fantastic investment opportunity whispers in your ear? Ka-ching! Having a healthy savings account is like having a safety net made of marshmallows. It’s soft, comforting, and catches you before you fall too hard.

Must Read

The Mortgage Hug vs. The Savings Shield

So, how do we even begin to untangle this? Let's break it down with some relatable scenarios. Picture your neighbor, Brenda. Brenda is a mortgage-slayer. She lives frugally, packs her lunch every day, and her extra cash? Straight to the mortgage principal. She’s got a countdown clock on her loan, and she’s getting closer to that "paid in full" party every single month. Brenda sleeps like a baby knowing her biggest financial obligation is shrinking faster than a wool sweater in a hot wash.

Then there’s your friend, Mark. Mark is a savings guru. He’s got an emergency fund that could rival a small nation’s treasury. He’s also got a separate pot of money for "fun stuff" and another for "future adventures." Mark’s mortgage is chugging along at its usual pace, but if a tree falls on his roof, he’s not calling the bank for a loan – he’s calling the repair crew with cash in hand. Mark feels secure, knowing he’s got options and isn't at the mercy of unexpected life events.

Who’s right? Well, both Brenda and Mark are doing something smart, just with different priorities. It’s not a one-size-fits-all situation, folks. It’s more like choosing your favorite ice cream flavor – it depends on your mood, your circumstances, and what makes you feel the most satisfied.

:max_bytes(150000):strip_icc()/sick-of-mortgage-payments-pay-off-your-home-early-453826_Final-201fc508b83c4f839d73a7a8bb4d1098.png)

When Does the Mortgage Hug Feel Sweeter?

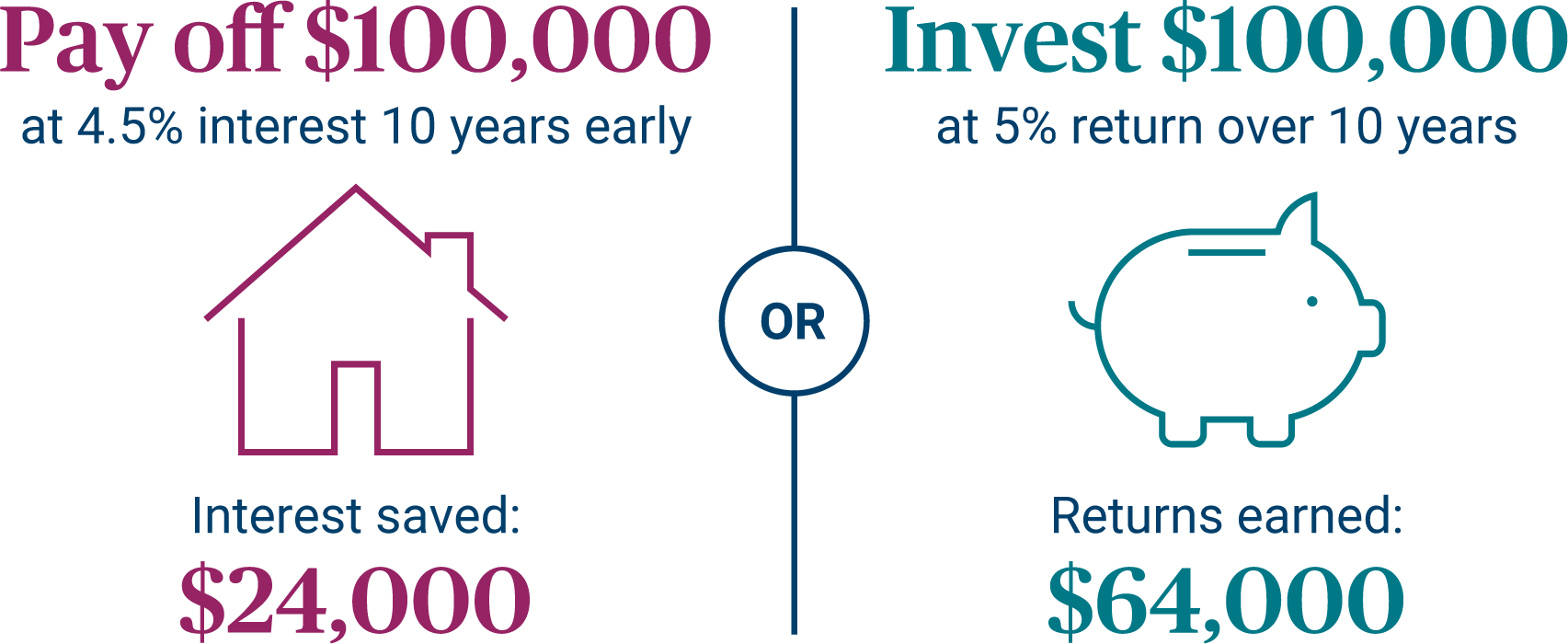

There are definitely times when aggressively paying down your mortgage makes a lot of sense. Let's say your mortgage interest rate is relatively high. Imagine paying 5% or more on a large sum of money for years. Every extra dollar you put towards the principal is like getting a guaranteed return of that interest rate, tax-free! That’s pretty hard to beat with most savings accounts, especially in today's economic climate.

Think about it this way: if you have $100,000 left on your mortgage at 5% interest, and you make an extra $500 payment one month, that $500 isn't just a payment. It's like investing that $500 at a guaranteed 5% return, because that's the interest you won't have to pay over the life of the loan. Over time, that adds up to a significant amount of saved interest. It’s like finding money you didn't even know you were losing!

Also, consider your personality. Are you the type of person who gets stressed out by debt? Does the thought of that monthly payment hang over your head like a rain cloud? If so, paying down your mortgage can bring immense psychological relief. It’s like shedding a heavy backpack you’ve been carrying around for years. That peace of mind is invaluable, and sometimes, it’s worth more than a few extra dollars in a savings account.

And let’s not forget the "finish line" feeling. There's a powerful motivation in seeing your mortgage balance dwindle. It's a tangible goal, and achieving it feels incredibly empowering. It’s like crossing the finish line of a marathon – exhausting, but oh-so-rewarding!

When Does the Savings Shield Shine Brighter?

Now, what about the savings shield? When is having a robust savings account the smarter move? First and foremost, if your mortgage interest rate is super low – like, 2% or 3% – the guaranteed return from paying extra on your mortgage might not be as compelling. You could potentially earn more by investing that money, even in relatively safe options.

But the biggest reason to prioritize savings is for those inevitable life curveballs. Remember Brenda, the mortgage-slayer? What if Brenda’s job is suddenly cut, or she faces a major medical emergency and her insurance doesn’t cover everything? Without a substantial emergency fund, she might have to tap into her retirement savings or even take out a high-interest loan, negating the benefits of her aggressive mortgage payments.

Think of it like this: you're hiking up a mountain. Paying off your mortgage is like reaching a beautiful scenic overlook. But having savings is like packing extra water and a first-aid kit. You might not need them, but if you do, they can be absolute lifesavers. It ensures you can keep going, even if the trail gets a bit rocky.

Furthermore, if you have other, higher-interest debts – like credit card balances or personal loans – it almost always makes sense to tackle those before aggressively paying down your mortgage. Those debts are like leaky faucets in your financial house, dripping away your money with high interest. Plugging those leaks should be your top priority!

Finding Your Sweet Spot

So, where does that leave us? The truth is, for most people, the answer isn't an "either/or." It’s often a "both/and." It’s about finding your personal sweet spot.

Here's a simple approach:

- Build a Basic Emergency Fund: Before you even think about extra mortgage payments, make sure you have a cushion for at least 3-6 months of essential living expenses. This is your non-negotiable safety net.

- Tackle High-Interest Debt: If you have credit card debt or other loans with high interest rates, make paying those off your absolute priority. The interest you save here is usually much higher than your mortgage interest.

- Consider Your Mortgage Rate: If your mortgage rate is low, you have more flexibility to balance saving and paying extra. If it's high, extra mortgage payments become more attractive.

- Factor in Your Personality: How much do you value peace of mind versus potential financial gains? Your comfort level with debt is a huge factor.

- Don't Forget Future Goals: Are you saving for retirement? For your kids' education? Make sure you’re also contributing to these long-term goals.

Maybe you decide to put an extra $200 towards your mortgage each month and also beef up your savings account with $150. Or perhaps you focus heavily on savings for a year until you reach a specific goal, then shift your focus to the mortgage. It's about being intentional and creating a plan that works for you.

At the end of the day, whether you’re a mortgage-slayer like Brenda or a savings guru like Mark, you’re making a choice that aligns with your financial well-being. The most important thing is to be informed, be deliberate, and to make a decision that brings you a sense of security and happiness. So, take a deep breath, consider your own situation, and choose the path that makes your financial heart sing!