Is Income Statement The Same As Profit And Loss

Hey there, fellow humans! Ever find yourself staring at a pile of bills, a receipt from that amazing coffee shop, or maybe even just counting the coins in your pocket after a big grocery run? If so, you've already dipped your toes into the world of income and expenses. And that, my friends, is exactly what we're going to chat about today – a little something called the Income Statement. Now, before you picture a stuffy accountant with a calculator the size of a brick, let me tell you, it's not as scary as it sounds. In fact, it’s kinda like looking at your own personal budget, but for a business.

So, the big question that might be tickling your brain cells is: Is the Income Statement the same as the Profit and Loss (P&L) statement? Drumroll, please… The answer is a resounding yes! They are basically two peas in a pod, two sides of the same very important coin. Think of it like this: "income statement" is the formal, professional name, while "profit and loss statement" is the more descriptive, down-to-earth way of saying the same thing. They both tell the same story, just perhaps with slightly different emphasis on the title.

Let's break it down with a fun analogy. Imagine you have a lemonade stand. On a hot summer day, you're super excited to sell your refreshing concoctions. Your income, in this case, is all the money you make from selling that delicious lemonade. Every cup sold is a little victory! Now, think about what it takes to make that lemonade. You need lemons, sugar, water, cups, and maybe even a cute little sign. The money you spend on these things? That's your expenses, or as businesses call them, your costs. You've got the cost of the lemons, the sugar, the cups – all those little bits that add up.

Must Read

The Income Statement, or P&L, is simply a report that shows how much money you've brought in (your income) and how much money you've spent (your expenses) over a certain period of time. It's like a snapshot of your financial health, showing whether your lemonade stand is making you a profit or if you're ending up with less money than you started.

The Magic of "Profit" and "Loss"

This is where the "profit and loss" part really shines. At the end of the day (or the month, or the year), you want to know if your lemonade stand is actually making you any money, right? If you sold $50 worth of lemonade and only spent $20 on ingredients and supplies, congratulations! You’ve made a profit of $30. That's the good stuff! That $30 is what you get to keep, or reinvest in better lemons, maybe a fancier pitcher, or even a fun treat for yourself.

But what if, on a slow Tuesday, you only sold $10 worth of lemonade, but you still had to buy $15 worth of supplies? Ouch. In this scenario, you've made a loss of $5. This means you spent more than you earned, and you're down $5. It’s not the end of the world, but it’s definitely something you’d want to pay attention to. Maybe you need a better spot for your stand, or perhaps a special "buy one, get one free" deal.

Why Should You Even Care?

Okay, so you might be thinking, "This is all well and good for lemonade stands, but I'm not running a business." Ah, but you are, in a way! Think about your own finances. When you get your paycheck, that's your income. The rent, the groceries, that fun movie ticket, the gym membership – those are your expenses. You are essentially doing your own personal profit and loss calculation every time you manage your money!

Understanding your Income Statement (or P&L) is super important for businesses because it tells them a few key things:

1. Are We Making Money? This is the most obvious one. If a business isn’t making a profit, it can’t survive. It’s like trying to keep your car running without gas – it just won’t go anywhere for long.

2. Where Is Our Money Going? The P&L statement breaks down all the expenses. So, a business owner can see if they're spending too much on, say, fancy office supplies or if their marketing budget is really paying off. It’s like looking at your bank statement and saying, "Wow, I spend a lot on takeout coffee!"

3. How Are We Performing Over Time? By looking at the P&L for different periods (like this month versus last month, or this year versus last year), businesses can see if they are growing, shrinking, or staying the same. It’s like tracking your weight – you can see if you’re getting healthier or if you need to make some changes.

4. Can We Afford to Do New Things? If a business is consistently making a good profit, it has more freedom to invest in new products, hire more people, or even open up new locations. Imagine your lemonade stand making enough profit to buy a whole truckload of lemons for a massive neighborhood sale!

The "Official" Look

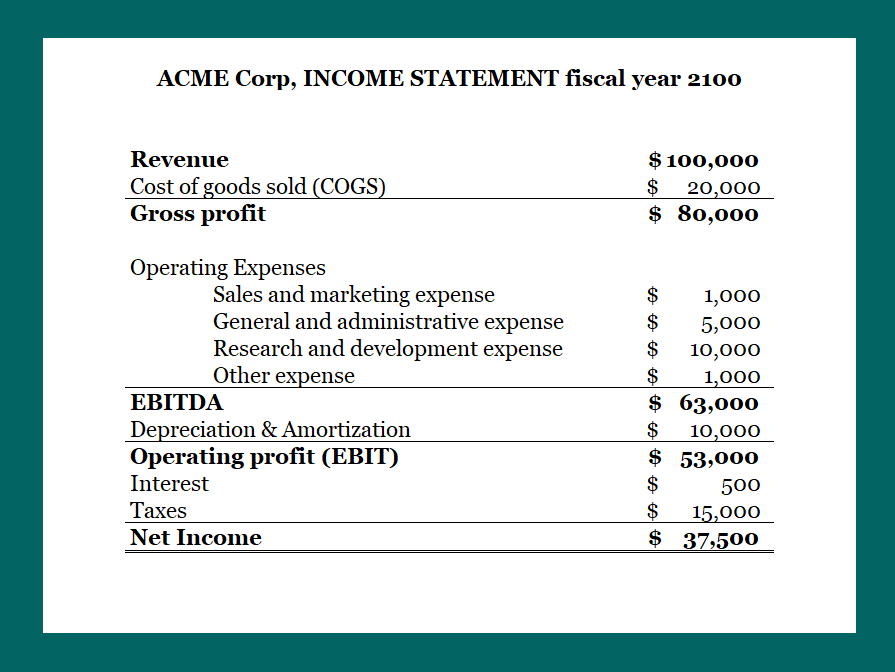

So, what does this magical statement actually look like? Well, it’s usually a pretty straightforward list. It starts with all the revenue (that's just another word for income, the money coming in from sales). Then, it subtracts all the costs of goods sold (the direct costs to create what you sell – like the lemons and sugar for our lemonade). What’s left is your gross profit.

Next, it subtracts all the other operating expenses (things like rent, salaries, marketing, utilities – the everyday running costs of the business). And ta-da! What’s left is your net profit (or net loss). This is the bottom line, the real number that tells you if you’ve had a successful period or not. It’s the grand finale of the financial story.

Think of it like baking a cake. Your revenue is the price you sell the cake for. The cost of flour, eggs, sugar, and butter is your cost of goods sold. The profit you make after selling the cake is your gross profit. Then, if you’re running a bakery, you have to pay for the oven, the electricity, the rent for the shop, and maybe even a baker’s salary. Those are your operating expenses. Subtract those, and what’s left is your net profit – the sweet reward for your hard work!

So, the next time you hear someone talk about the "Income Statement" or the "Profit and Loss statement," you can nod knowingly. They are both simply the financial report card that shows whether a business is earning more than it's spending, helping it to grow and thrive. It's not some secret code for the super-rich or the accounting wizards; it’s a fundamental way to understand the health of any venture, big or small. And that, my friends, is something we can all benefit from understanding, even if it’s just for our own personal lemonade stands!