How To Pay Inheritance Tax Without Selling Property

So, you've inherited a bit of a windfall – maybe a charming cottage by the sea, or a sprawling estate that's been in the family for ages. Fantastic! But then, the dreaded spectre of Inheritance Tax (IHT) looms, and you start to panic about potentially having to wave goodbye to those cherished bricks and mortar. Don't you worry your sweet little head about it! There are actually some rather clever ways to tackle this tax beast without resorting to a frantic "For Sale" sign. We're talking about keeping your beloved property and satisfying the taxman. It’s like having your cake and eating it too, but with less flour and more spreadsheets!

Let's be honest, the thought of selling a place filled with precious memories can feel like a bit of a tragedy. Imagine the tears! The packing boxes! The questionable estate agent advice! But fear not, because the good old UK tax system, believe it or not, offers a few sneaky little loopholes. We're going to explore some of these, and I promise, it's not going to be a dry, dusty lecture. Think of this as your fun, no-sweat guide to keeping your inheritance intact.

The "Pay As You Go" Approach – But Not Literally!

Okay, so you can't exactly pop down to the corner shop with your IHT bill. But there's a concept called paying the tax in instalments. Yes, you read that right! You can actually spread the cost, making it a whole lot less like a financial punch to the gut. This is particularly brilliant if the property itself isn't generating immediate cash, but it's worth a pretty penny.

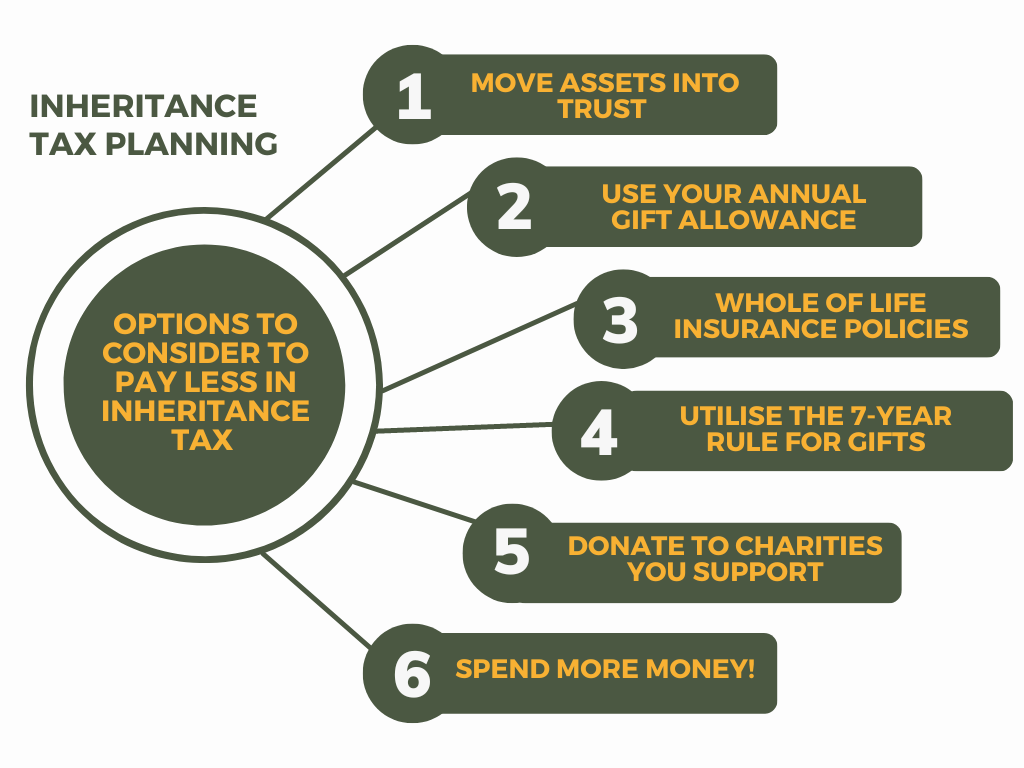

Must Read

The magic ingredient here is often found in the form of a loan. Now, I know what you're thinking: "A loan? To pay tax? Isn't that like borrowing money to buy lottery tickets?" Not quite! Think of it as a strategic financial move. You're borrowing the cash to pay the tax bill, and then you can either repay the loan from other assets you have (perhaps some cash stashed away, or maybe another less sentimental investment) or, and this is where the property comes in, you can eventually sell the property later and use those funds to clear the loan. It's a bit of a long game, but it keeps the family home safe for now.

The key is to get this organised with HMRC, the UK's tax authority. They're not usually the kind of people you want to ignore, but they can be surprisingly understanding if you approach them with a sensible plan. They’d rather have the money eventually than have you forced into a desperate sale. It’s all about communication, darling!

The "Borrow From the Bank of Mum and Dad... or the Bank of the Bank"

This ties in beautifully with the instalment idea. If you’ve got other financial wiggle room, perhaps an existing savings account brimming with a few extra quid, or even a sensible investment portfolio that’s not tied up in, say, a collection of antique porcelain cats (unless they're very valuable), you can tap into that. This is essentially using your own liquid assets to cover the IHT bill.

Imagine you've inherited that delightful cottage, but you also have a nice chunk of cash from your own hard work. You can simply use that cash to pay the tax! No property sales required. It’s like a superhero swooping in with a bag of money just when the tax monster is about to strike. Ta-da! The property remains yours, and your bank account takes a slight, but manageable, hit.

Alternatively, if your own coffers aren't quite so full, you can explore options like a loan secured against other assets. This could be another property you own, or perhaps investments. The bank will look at your overall financial picture, and if it's solid, they might be willing to lend you the money you need to pay the IHT. Again, the goal is to avoid selling the inherited property.

The "Gift-Giving" Game – With a Twist

Now, this one requires a bit of forward planning, and it's more about how future inheritances might be handled, but it’s a clever strategy nonetheless. If you're looking to pass on assets to your own children or loved ones in the future, and you're concerned about them facing IHT, you can start making gifts during your lifetime. Now, there are rules around this, so you can't just hand over everything willy-nilly and expect it all to be tax-free immediately. That would be a bit too easy, wouldn't it?

However, there's a concept called the "seven-year rule". If you survive for seven years after making a gift, it generally falls outside of your estate for IHT purposes. This is like a magic shield that gets stronger with time! So, if you have assets that you know will eventually be subject to IHT, and you can afford to part with some of them, giving them away to your beneficiaries years in advance can significantly reduce the IHT burden for them down the line. It's like playing a long game of financial chess.

This is particularly useful if you have assets that are likely to appreciate in value. By gifting them early, you're not only reducing the IHT on the current value, but you're also gifting away any future growth. It’s a win-win, provided you're not planning on needing those assets yourself in the next seven years. So, no gifting your emergency fund for that sudden urge to buy a private jet!

The "Trusty Trustee" Technique

For the more organised among us, or for those with particularly valuable estates, setting up a trust can be an absolute game-changer. Trusts are like little financial boxes where you can place your assets. You, or someone you appoint, can be the trustee, managing the assets for the benefit of your chosen beneficiaries.

The beauty of a trust is that it can be structured in such a way that the assets within it are not considered part of your estate for IHT purposes. This can significantly reduce the tax bill when the assets are eventually passed on. It’s like having a secret vault that the taxman can’t peek into!

There are various types of trusts, each with its own rules and benefits, so it's definitely worth getting some professional advice on this one. But the general idea is that by transferring ownership of assets to the trust, you're effectively moving them out of your personal estate, thereby reducing the IHT liability for your heirs. Imagine your beautiful inherited property being held securely within a trust, protected from hefty tax bills.

The "Let the Property Pay for Itself" Ploy

This is a more direct approach that can work if the inherited property can generate income. Think of a rental property. If you inherit a house that’s already tenanted, or one you can easily rent out, the rental income can be used to pay down the IHT bill. It’s like the house is working for its keep!

You can, of course, continue to pay the tax in instalments using loans as we discussed. But if the rental income is substantial enough, you might be able to use it to pay off those loan repayments. Over time, the property is essentially funding its own tax clearance. It's a beautiful synergy of real estate and fiscal responsibility.

This strategy requires careful management of the property and its finances, of course. But the concept of having the asset itself contribute to its tax burden is undeniably appealing. No need to sell the farm when the farm can help you pay the bills!

So, there you have it! A few delightful ways to navigate the tricky world of Inheritance Tax without having to sell off your precious inherited treasures. Remember, a little bit of planning and a touch of financial savvy can go a long way. You can keep your memories, your property, and your peace of mind. Now, go forth and be merry (and financially responsible)!