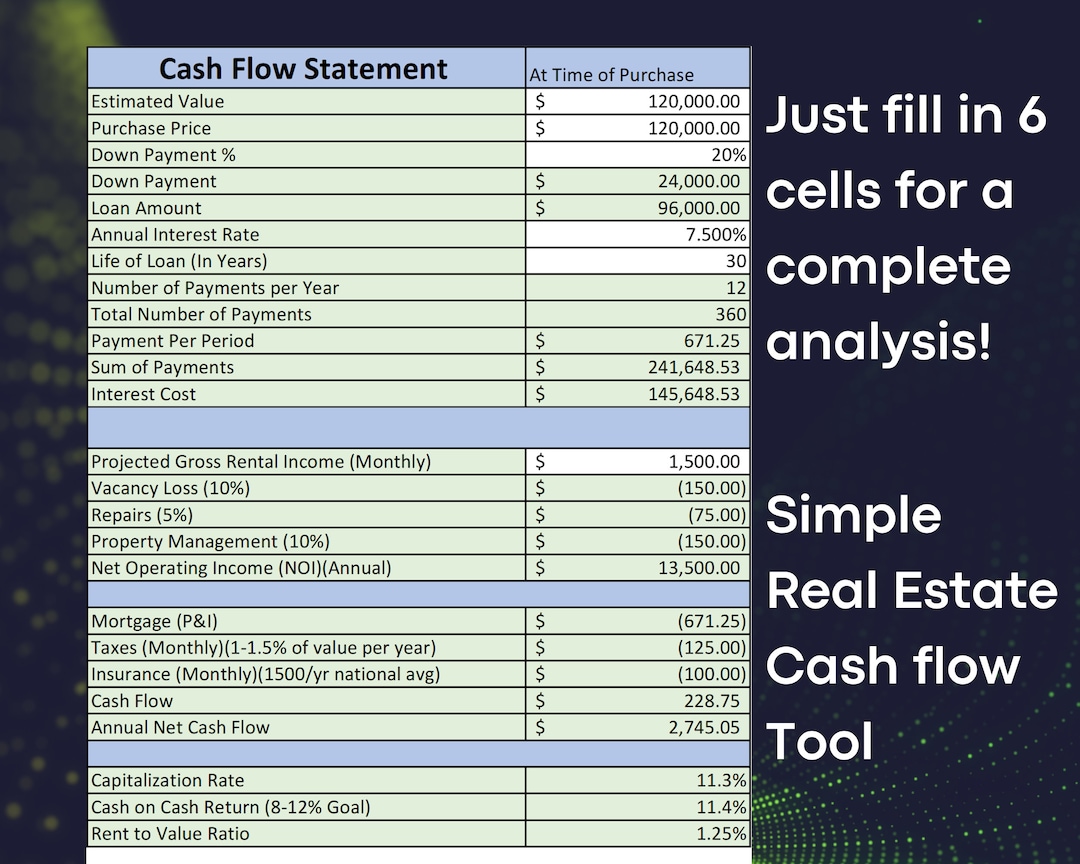

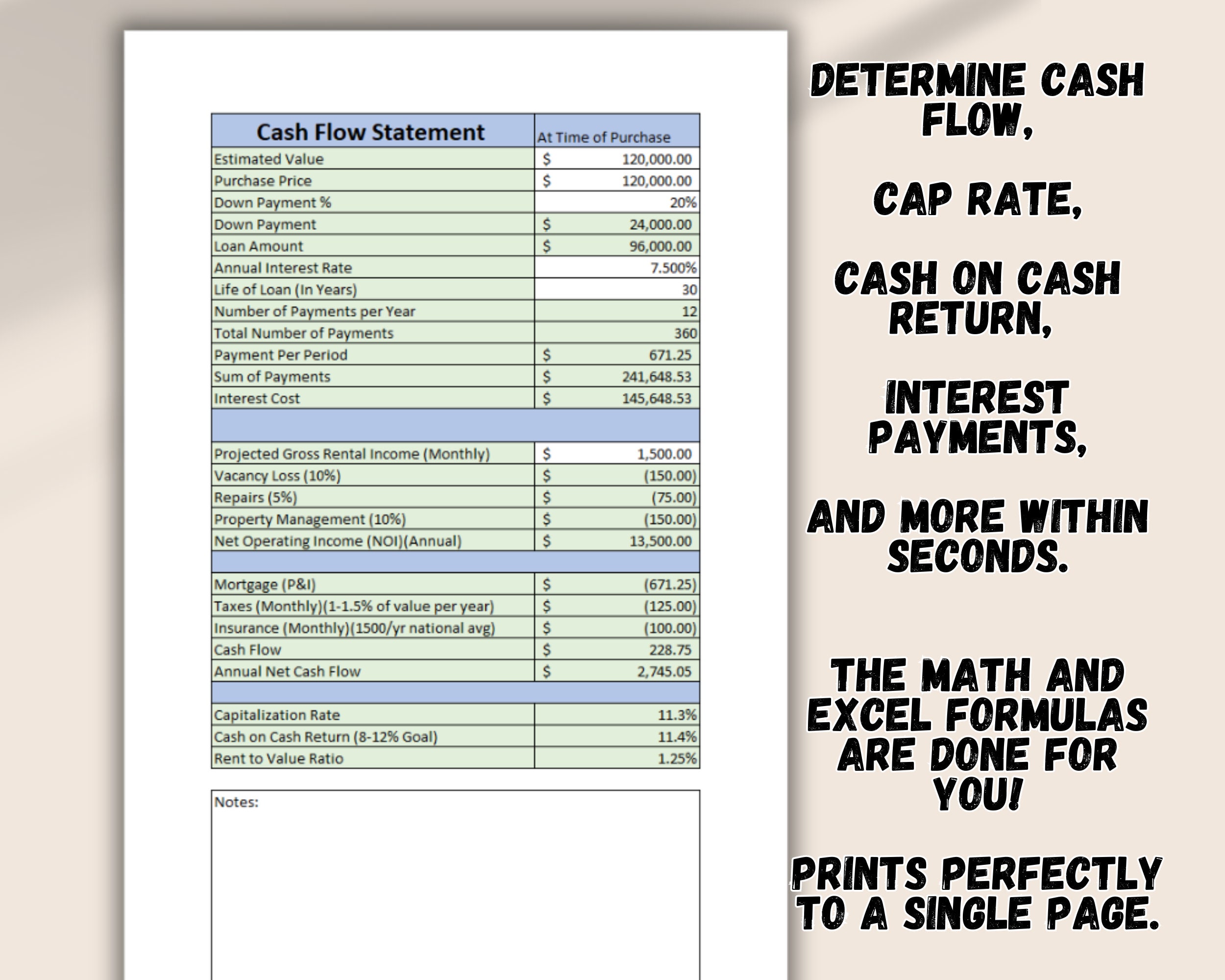

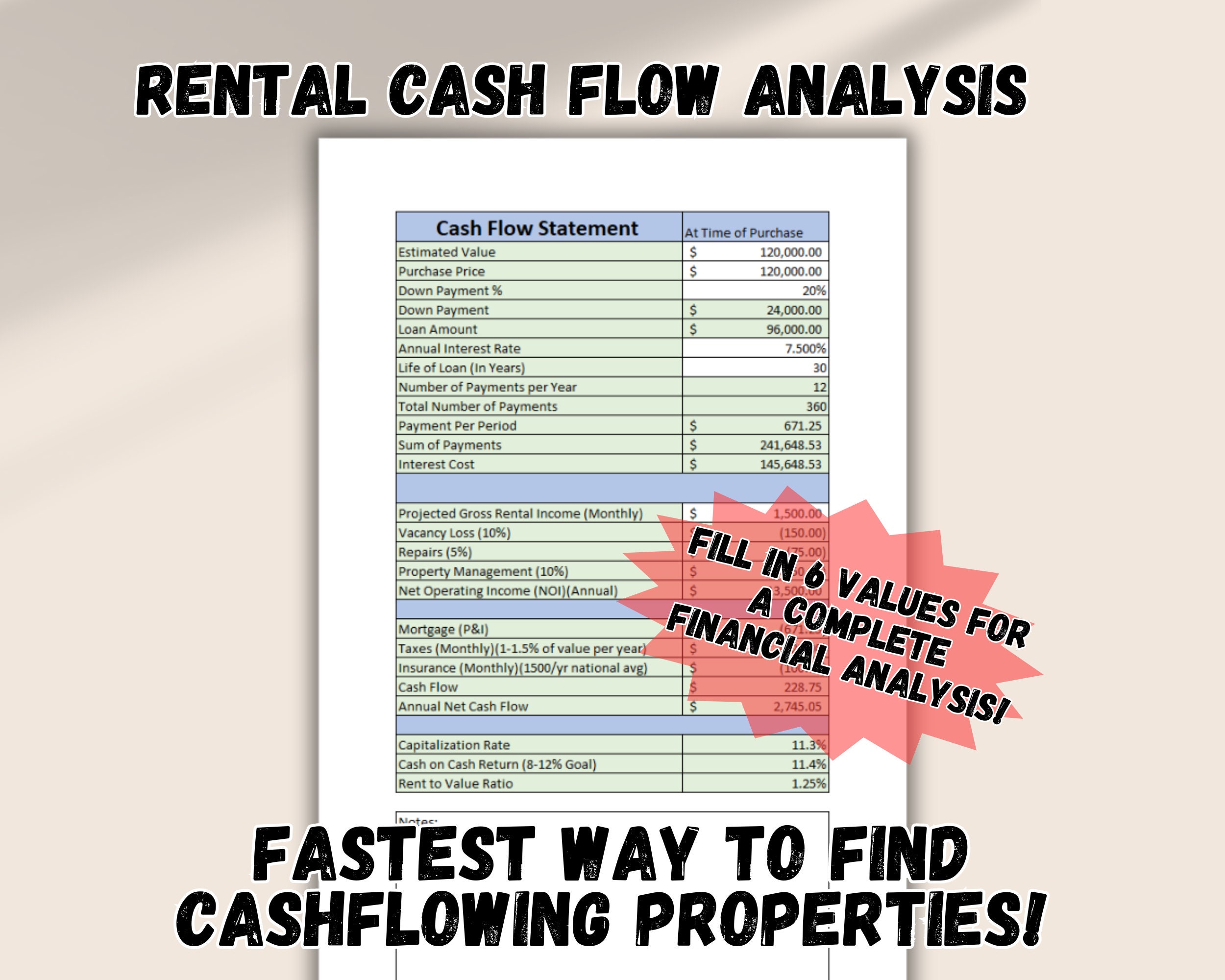

How To Estimate Rental Property Cash Flow

Ever dreamt of a little pile of cash just magically appearing in your bank account every month, thanks to a property you own? Well, it's not exactly a unicorn, but it's definitely a thing called rental property cash flow! And guessing how much that magical money will be isn't as scary as wrestling a greased-up pig at a county fair. Let's break it down, shall we?

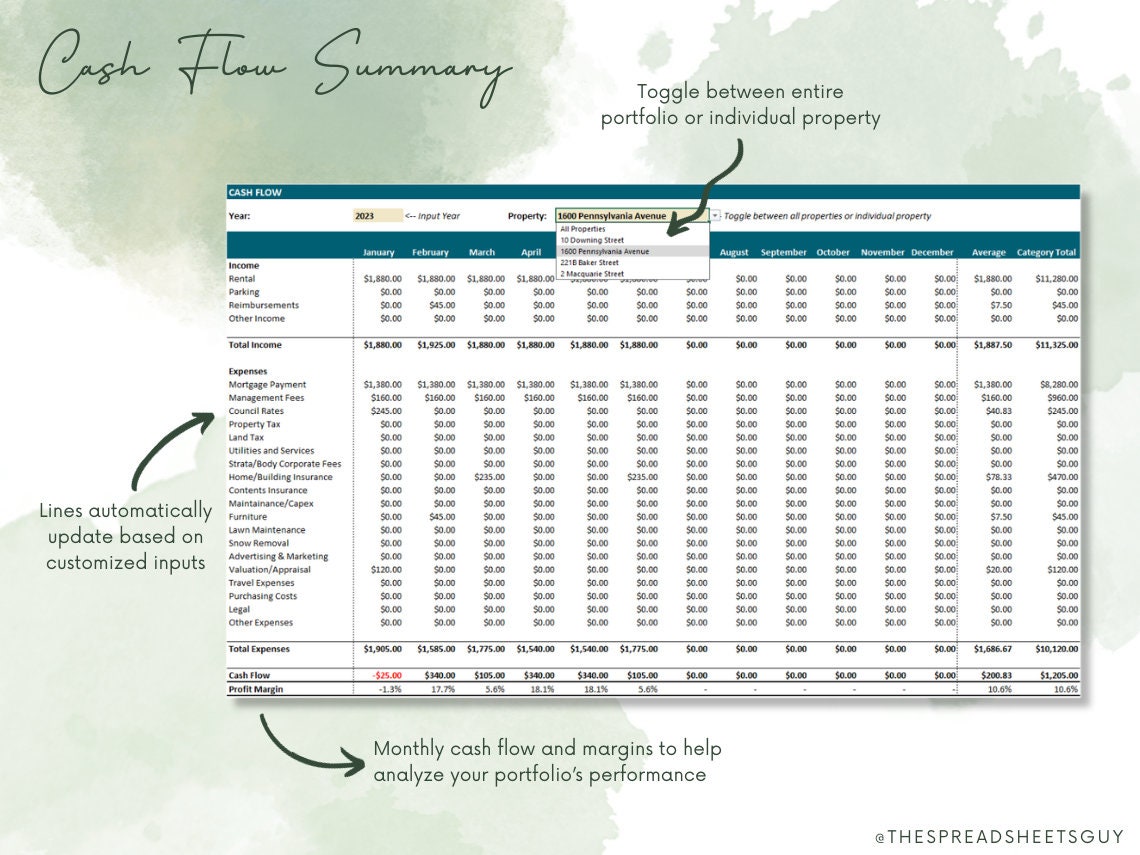

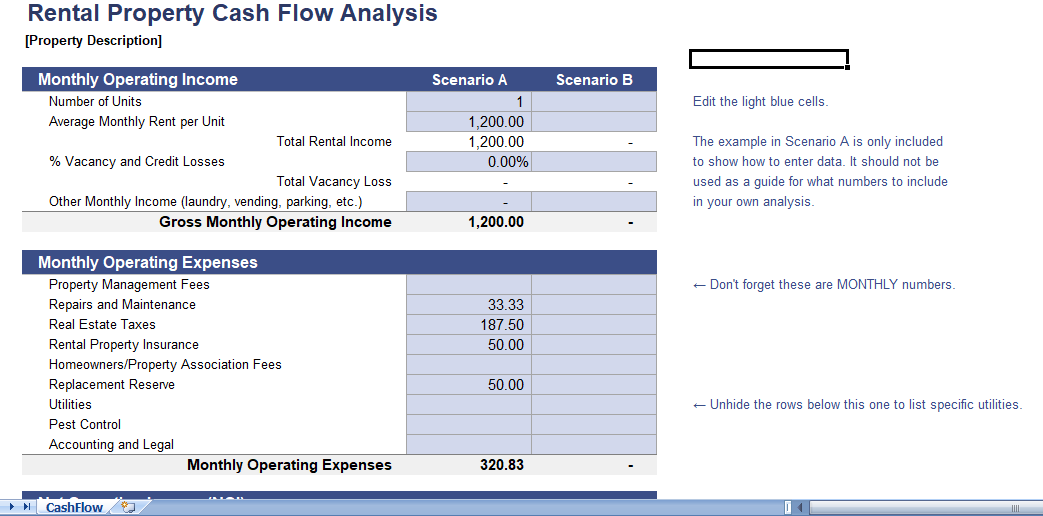

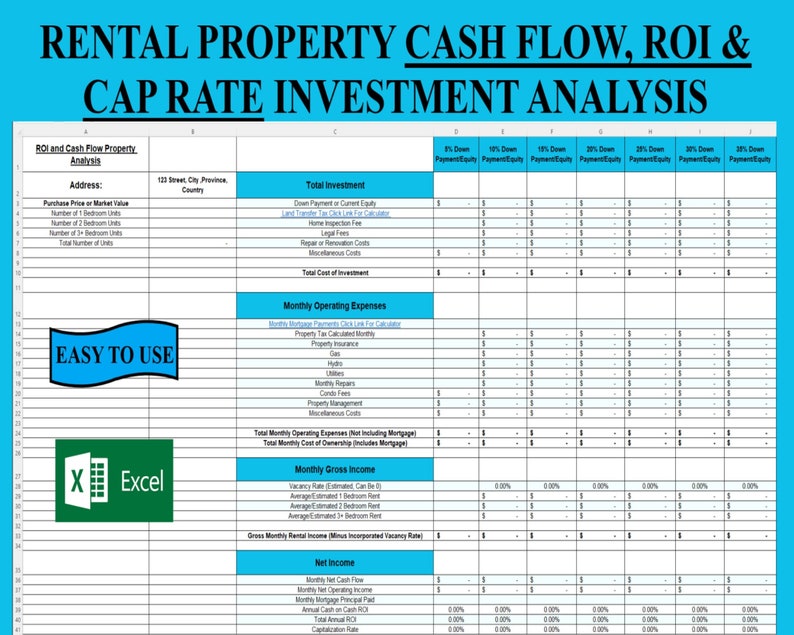

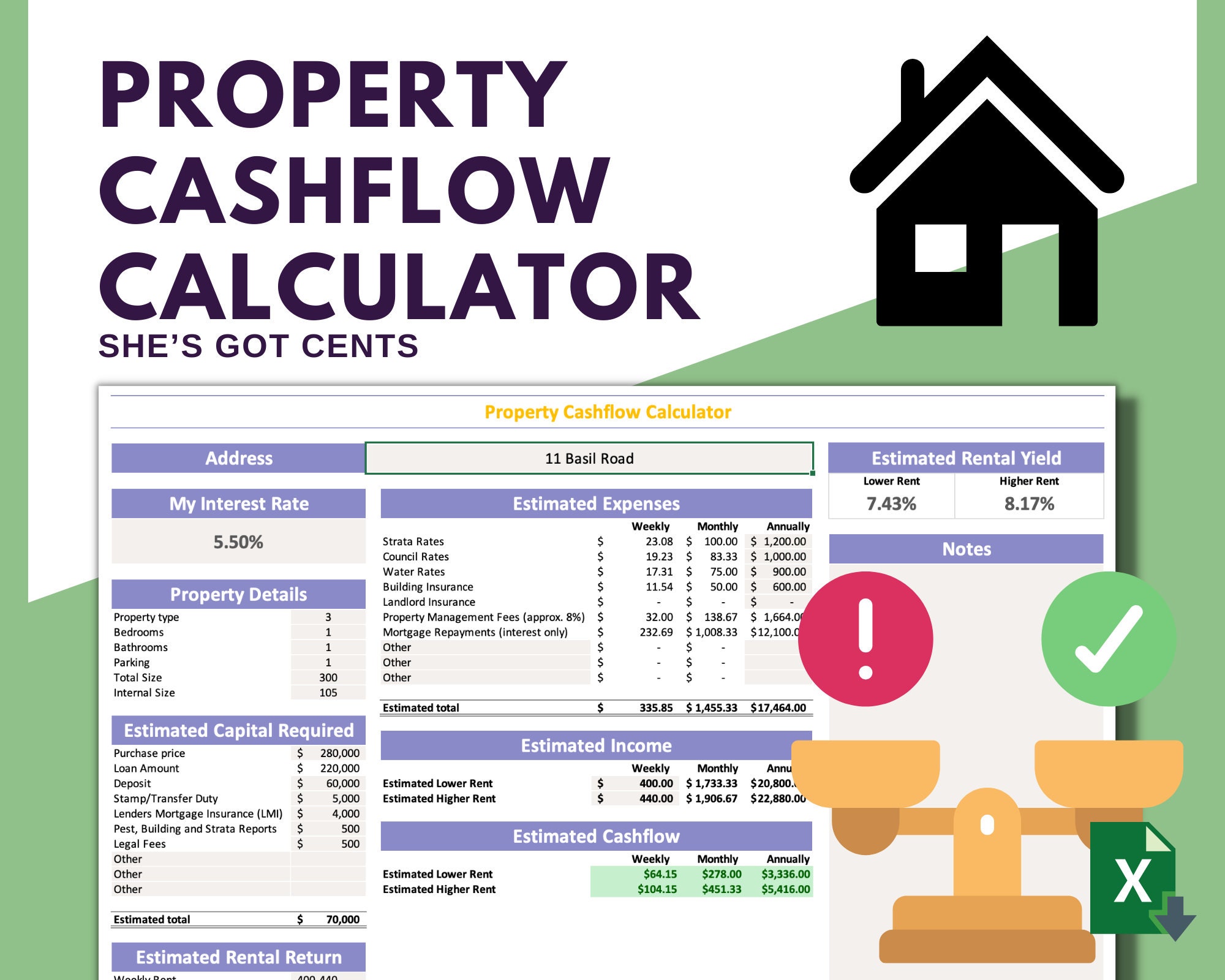

Think of cash flow as the money left over after you've paid all the bills associated with your rental property. It's the sweet, sweet reward for being a landlord – the actual profit you pocket. If this number is positive, you're essentially getting paid to own a property. Pretty neat, right?

The Grand Estimate: A Simple Formula

At its heart, estimating cash flow is like figuring out how much candy is left after you've shared some with your siblings (and maybe snagged a few extra yourself). The super-simplified formula is this: Rental Income - Expenses = Cash Flow. Boom! That's the gist of it. But like a gourmet meal, the details are what make it delicious.

Must Read

Cracking the Code: Income is King!

First things first, let's talk about the money rolling in – your rental income. This is the rent you'll charge your awesome tenants. Do your homework here! What are similar properties in the neighborhood fetching? You don't want to be the person charging what feels like a king's ransom or, conversely, leaving money on the table like a forgotten appetizer.

Check out online listings, chat with local real estate agents who practically live and breathe rental rates, and even drive around to see "For Rent" signs. Aim for a realistic number, one that tenants will happily pay and that reflects the value of your property. Imagine a rent so perfect it makes tenants say, "Sign me up!" before you even finish showing them the place.

The Expense Expedition: Brace Yourselves!

Now, for the part where things can get a little… interesting. Expenses are everything you have to pay out of pocket to keep that rental ship sailing smoothly. And trust me, there are more than just one or two!

The Usual Suspects: The Must-Pay Bills

Every landlord has to deal with these. First up, the big one: mortgage payment. If you've got a loan on the property, this is your monthly debt. Then there's property taxes. These are like the government's way of saying, "Thanks for owning this cool thing!" They can change, so get a good estimate.

Homeowner's insurance is non-negotiable. It's your safety net against, well, everything that could go wrong. Think of it as a magical force field for your property. Don't forget about utilities! Will you cover water, trash, sewer, or electricity? Clarify this upfront and budget accordingly. It's like deciding who gets to control the thermostat in a shared apartment, but with real money.

The Sneaky Stuff: Things That Pop Up

This is where things get a little more… creative. Property management fees are a big one if you're not managing it yourself. Think of them as paying a professional butler to handle all the tenant drama. Even if you're a DIY landlord, it's smart to budget a small amount for your time and effort – your own personal "landlord salary."

Then there's repairs and maintenance. This is the wild card! Leaky faucets, a broken washing machine, a tree branch deciding to make friends with your roof – these things happen. A good rule of thumb is to set aside a percentage of your rental income for this. Some people say 1% to 10% of the property value annually, or a certain amount per month per unit. This is where playful exaggeration comes in: imagine a squirrel chewing through your electrical wires – better be prepared!

Vacancy is another beast. Your property won't be rented 100% of the time. There will be periods between tenants. It's wise to factor in a month or two of lost rent per year. This is like saving up for that epic vacation you know you'll take, even if you don't know when. It’s the calm before the next tenant storm.

And don't forget capital expenditures (CapEx). These are the big-ticket items that will eventually need replacing: the roof, the HVAC system, the water heater. These aren't monthly expenses, but they'll drain your bank account if you're not ready. Imagine your furnace deciding to go on strike in the middle of winter – you’ll need funds for its replacement!

The Calculation Shuffle: Putting It All Together

Okay, deep breaths! We've gathered our income and our expenses. Now, let's do the magic math. Take your estimated monthly rental income and subtract all your estimated monthly expenses. This includes a portion of your annual property taxes, insurance, CapEx, and a monthly allowance for repairs and vacancy.

For example, if you rent your place for $2,000 a month, and your mortgage, taxes, insurance, and estimated monthly reserves for repairs, vacancy, and CapEx add up to $1,500, then your estimated monthly cash flow is $500 ($2,000 - $1,500). That's $500 extra in your pocket!

Making It Shine: Optimizing Your Cash Flow

The goal is to have a positive cash flow – meaning more money is coming in than going out. The higher the number, the happier your bank account will be. It’s like a seesaw; you want the income side to be way heavier!

To boost your cash flow, you can try to increase your rental income (carefully, of course!) or meticulously cut down on expenses. Maybe you can find a cheaper insurance policy, or perhaps you're overestimating your repair budget. Every dollar saved is a dollar earned!

Estimating cash flow might seem like a puzzle, but it’s really just about being realistic and doing your homework. It’s about creating a predictable stream of income that can make your financial dreams a reality. So go forth, estimate with confidence, and may your cash flow be ever positive and plentiful!