How Much You Should Spend On Rent

Alright, gather 'round, you lovely lot, and let's talk about the beast that haunts our bank accounts: rent. It's like that slightly clingy ex you can't quite shake, always demanding attention (and a significant chunk of your hard-earned cash). We’ve all been there, staring at a rent statement with the same bewildered expression a cat has when you show it a cucumber. What is this sorcery?!

So, how much should you be shelling out for your cozy (or let's be honest, sometimes cramped) abode? The internet, bless its digital heart, is practically overflowing with advice. You've got your trusty "30% rule," your more aggressive "20% rule," and then there are those wildlings who suggest you live in a cardboard box and declare your freedom. We're going to navigate this labyrinth together, with more humor than a stand-up comedian on open mic night.

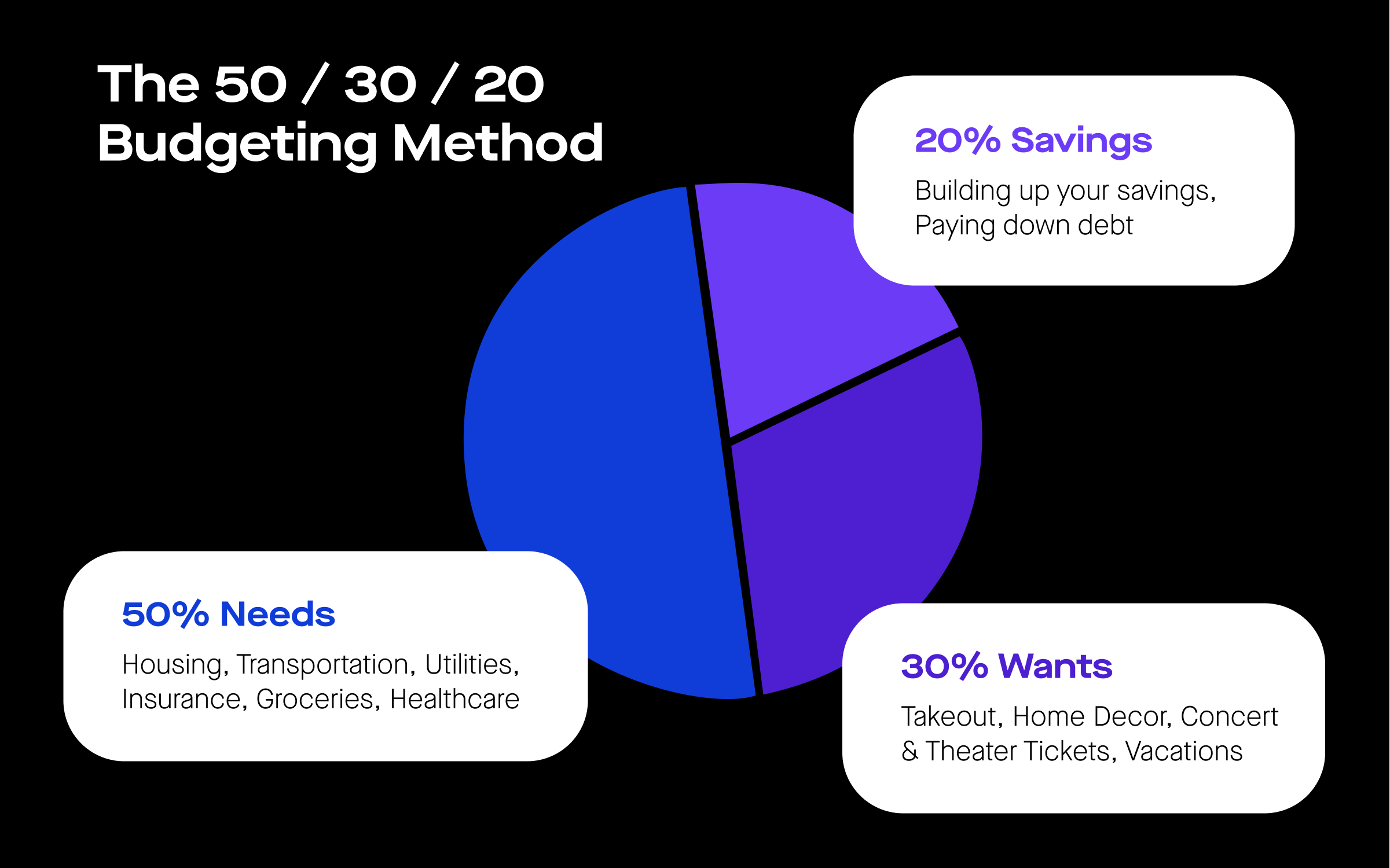

Let's kick things off with the most widely cited rule: the 30% rule. The general idea here is that your rent shouldn't gobble up more than 30% of your gross monthly income (that's the money before taxes and all the other fun deductions). So, if you're pulling in $4,000 a month, aim for rent no higher than $1,200. Sounds sensible, right? Like a perfectly toasted slice of sourdough.

Must Read

But here's the kicker: this rule is as old as dial-up internet and, frankly, sometimes as realistic. In many major cities, especially the ones where avocado toast is a primary food group, finding a shoebox for 30% of your income is about as likely as spotting a unicorn delivering your Amazon package. We're talking about places where even the pigeons probably have stock options. So, while it’s a great starting point, don't feel like a failure if reality slaps you with a higher percentage.

Then there's the stricter 20% rule. This one’s for the financial ninjas, the people who can knit their own sweaters and apparently have a personal chef who doubles as a budget advisor. If you can swing this, congratulations! You're basically living the dream, with enough disposable income to, you know, buy things that aren’t ramen. However, for the vast majority of us, aiming for 20% is like trying to do a triple backflip on your first day of gymnastics. Impressive, but probably not happening.

Now, let's get real. The "best" rent percentage is as unique as your fingerprint, or your questionable taste in music. It's a personal equation. Factors like your debt, your savings goals, your lifestyle, and whether you dream of owning a solid gold toilet all play a role. If you're drowning in student loans that make a small nation's GDP look like pocket change, or you're aggressively saving for a down payment on a house (which, in some cities, might actually be a really nice shed), then a lower rent percentage becomes critically important.

Imagine your income as a pizza. The 30% rule says your rent gets three slices. The 20% rule says it gets two. But what if you've got other hungry mouths to feed? You’ve got your student loan pepperoni, your car payment mushrooms, your grocery pineapple (don't knock it till you try it!). Suddenly, those slices become a lot more precious. You need to decide how many slices each "mouth" gets, and that’s where the art of budgeting comes in.

Let's talk about the grim, yet hilarious, reality for many. We're the "40% to 50% rule" club. Yes, you heard that right. Some of us are practically donating a kidney to our landlords every month. And while this isn't ideal (it leaves about as much room for fun as a sardine can), it's the situation for many. If you're in this boat, it doesn't mean you're a financial pariah. It just means you need to be extra smart about your other expenses. Think of it as extreme couponing, but for your entire life.

What are the signs you're spending too much on rent? Well, for starters, if your diet consists solely of instant noodles and the free condiments you pilfer from fast-food joints. If you haven’t bought new socks in three years because you’re worried about the $8 price tag. If your social life consists of watching Netflix at home because going out requires a second mortgage. These are all red flags, people! It’s not a badge of honor to be perpetually broke because your rent is astronomical. Your landlord, on the other hand, is probably living it up, possibly on a yacht made of pure gold, fueled by your monthly payments.

Consider this surprising fact: according to some studies, the average renter in San Francisco spends over 50% of their income on rent. Fifty percent! That’s like working half the month just to keep a roof over your head, and the other half to, you know, live. It’s enough to make you want to pack up your life and move to a yurt in Montana. And honestly, sometimes the thought is tempting.

So, what's the magic solution? There isn't one, sadly. It’s about honesty with yourself. Sit down with a spreadsheet (or a napkin, if spreadsheets are too intimidating) and map out your actual income and your actual expenses. Be brutally honest. That $5-a-day fancy coffee? That subscription you haven’t used in six months? Those impulse buys that make you feel good for five minutes and guilty for five days? They all add up. Every dollar you spend on non-essentials is a dollar you could be putting towards rent, or saving, or investing in that llama farm you've always dreamed of.

Think about your priorities. Is it crucial for you to live in the trendiest neighborhood, even if it means eating beans for every meal? Or would you rather have a bit more breathing room financially and live slightly further out, perhaps in a place where the pigeons don't judge your life choices?

And here’s a wild idea: negotiate your rent. Yes, you can do it! Landlords aren't always as rigid as a statue. If you’re a good tenant, always pay on time, and have kept the place in pristine condition (meaning no accidental existential graffiti on the walls), you have leverage. A polite conversation can sometimes shave off a surprising amount. Think of yourself as a shrewd negotiator, a wolf of Wall Street, but with less yelling and more polite requests.

Ultimately, the "how much you should spend on rent" question is less about a magic number and more about finding a balance. It’s about ensuring your housing situation doesn’t cripple your ability to live a fulfilling life, save for the future, or occasionally splurge on something that isn’t edible. It’s about making your home a sanctuary, not a source of constant financial dread. So, do your math, be honest about your habits, and may your rent payments be ever so slightly less painful than a root canal. And who knows, maybe one day you'll be the landlord on the gold yacht. A person can dream, right?