How Much Does Insurance Go Up After An Accident

Alright, gather 'round, grab your lukewarm latte, and let's talk about something that makes us all collectively groan louder than a toddler demanding a second cookie: car insurance after an accident. You know, that moment after you've exchanged insurance cards with a stranger who, let's be honest, probably has a secret life as a demolition derby champion, and you start to wonder about the financial fallout. Will your premium suddenly decide to do a bungee jump off a cliff? Will it start demanding caviar and private jets?

The short, slightly terrifying, and entirely true answer is: it depends. Like, a lot. Think of your insurance premium as a shy creature. It’s usually content to just… exist. But then BAM! An accident. And suddenly, it’s not so shy anymore. It’s got a lot to say, and most of it involves your wallet.

Let's break it down, shall we? Because nobody wants to be blindsided by a rate hike that makes their bank account weep. First off, we need to talk about the severity of the accident. Did you tap someone’s bumper gently while trying to parallel park with the grace of a newborn giraffe? Or did you perform an unplanned, high-speed ballet with three other vehicles and a rogue shopping cart? The difference is like comparing a stubbed toe to a full-blown amputation. And your insurance company, bless their data-crunching hearts, notices.

Must Read

A fender bender, especially if it's minor and you're not at fault, might barely register on your premium's radar. It's like a little "oopsie" in their books. They might sniff at it, perhaps issue a stern but polite memo, but your premium probably won't go into cardiac arrest. However, if your accident resembles a scene from a Fast & Furious movie, complete with screeching tires and an unexpected explosion of airbags (hopefully not a real explosion, but you get the picture), then your premium is going to sit up and take notice.

Then there's the golden ticket to a higher premium: fault. Ah, fault. The great divider. If you were the architect of the chaos, the conductor of the symphony of destruction, then yes, your insurance is likely to stage a dramatic increase. We're talking about those moments where you know you were the reason the universe decided to redecorate the asphalt. Your insurance company sees this as a rather expensive hobby you've picked up, and they're going to want to charge you accordingly for the privilege.

Now, if the accident wasn't your fault? Well, that's a different story. In many cases, if you’re deemed 100% not at fault, your premium might not budge an inch. It’s like your insurance company saying, "Okay, you survived. Good job. Don't do it again." But be warned, even if you're mostly innocent, if you had even a tiny contributing factor (like, say, you were momentarily distracted by a particularly dazzling butterfly), your insurer might see that as a microscopic crack in your otherwise pristine driving record, and that could still lead to a subtle eyebrow raise – and a small premium hike.

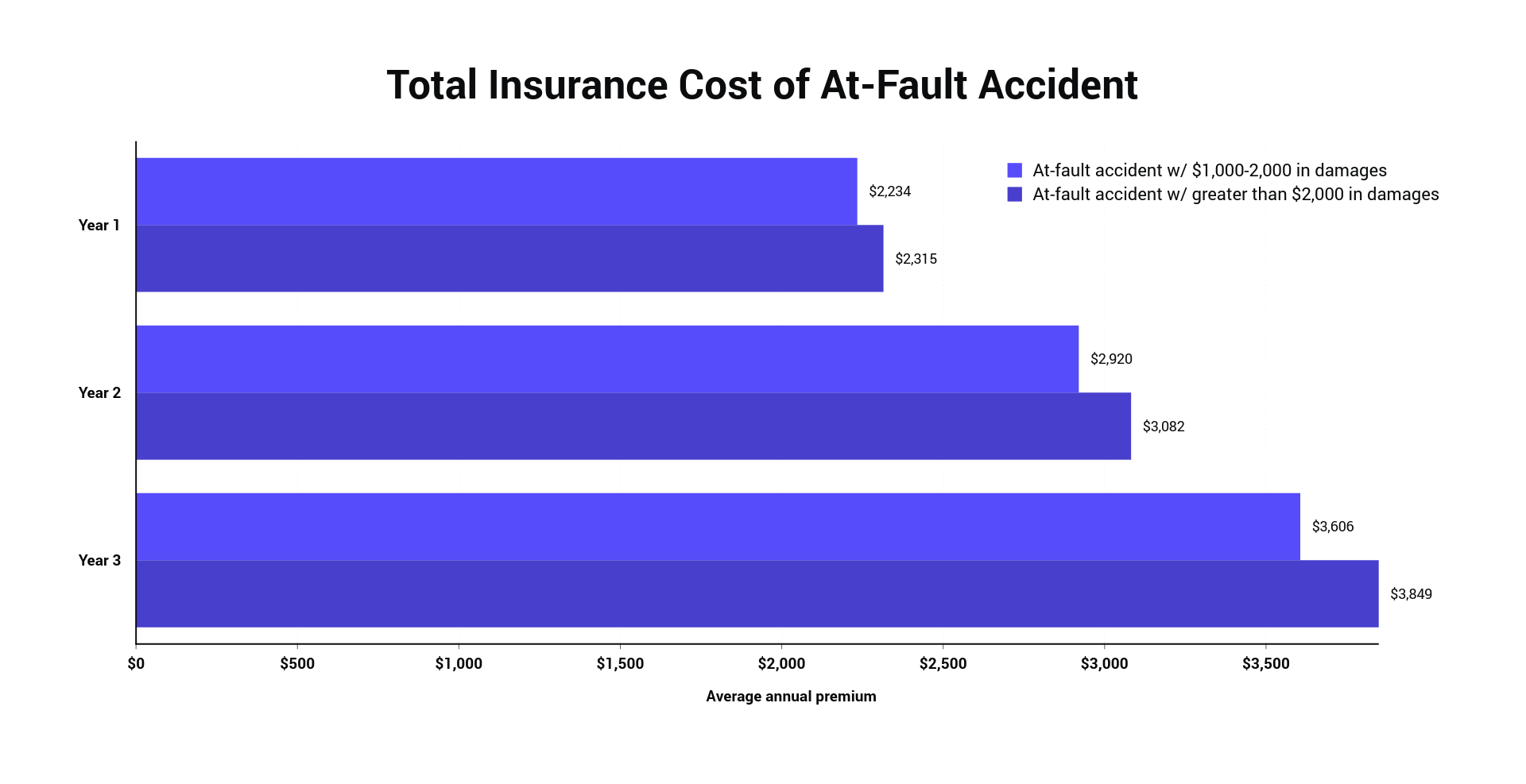

Speaking of hikes, how much are we actually talking? This is where the crystal ball gets a little cloudy, because insurance companies have more variables than a mad scientist's lab. Generally, after an at-fault accident, you could see your premium jump anywhere from 10% to 50% or even more. Imagine that! Your annual premium, which you probably already feel is high enough to fund a small nation, suddenly decides it wants to be an even larger nation. It’s like a surprise tax on your driving skills.

For a minor accident where you're at fault, it might be on the lower end of that scale. Think of it as a gentle nudge from your insurer, saying, "Hey, maybe ease up on the spontaneous U-turns, champ." But for a more significant accident, especially one involving injuries or substantial damage? Buckle up, buttercup, because that premium could go on a rocket ship to the moon. Some sources suggest that a major at-fault accident could even double your premium for a few years!

And let's not forget the magical number that insurance companies love to track: your driving record. If you've been a saint on the road for years, racking up accident-free months like they're Pokémon cards, your insurer might be a little more forgiving. They might even offer you a "claims forgiveness" program (which, by the way, is worth looking into!). But if your record looks more like a Jackson Pollock painting of near-misses and minor infractions, then one accident might just be the straw that breaks the camel's back – or in this case, the premium's budget.

Here's a fun (read: not fun at all) fact: some insurance companies use a "risk score" that goes up after an accident. This score is like your driving report card, and a bad grade means you're now in the "higher risk" category. It’s like being put on a naughty list, but instead of Santa bringing you coal, your insurance company brings you a higher bill.

What about the type of accident? Was it a multi-car pileup that looked like bumper cars gone wild? Or a single-vehicle incident where you decided to have a staring contest with a tree and the tree won? Both will affect your premium, but the former, with its potential for multiple claims, is usually the bigger budget-buster. It's like the domino effect, but with dollar signs.

And then there's the duration. This premium hike isn't usually a one-time thing. It often sticks around for three to five years, sometimes even longer, depending on the severity and your insurer's policies. So, that little accident you had last year might still be making your wallet feel a bit… lighter. It’s like a long-term commitment you never signed up for. A really expensive, unwanted commitment.

So, what's the takeaway from this thrilling adventure into the world of post-accident premiums? Firstly, drive safely. It sounds obvious, but it's the golden rule. Secondly, understand your policy. Know what "at-fault" means and what kind of coverage you have. Thirdly, shop around! After an accident, don't just meekly accept your increased premium. Get quotes from other insurance companies. You might be surprised at how much a little comparison shopping can save you. It’s like finding a hidden stash of money you didn't know you had!

Think of your insurance premium as a fickle friend. Sometimes it's there for you, quietly doing its thing. Other times, after a bit of a kerfuffle, it gets a little… demanding. But by being informed and proactive, you can navigate these choppy waters without your wallet capsizing. Now, who needs another coffee? This has been exhausting!