How Much Does A Short Lease Devalue A Property

Hey, so you're thinking about that short lease thing, huh? We've all been there, staring at the paperwork, wondering if it's a secret real estate superpower or a ticking time bomb. And the big question, the one that keeps you up at night (or at least makes you google at 2 AM), is about devaluing your place. Like, how much does a short lease actually tank your property's worth? Let's dive in, grab a virtual coffee, and spill the tea.

First off, what even is a short lease? It's not like your lease is a teenager, going through a rebellious phase. It’s basically a lease with a significantly shorter remaining term than what’s considered standard or desirable. Think, like, under 70 years left, sometimes even less than 50. It's the kind of thing that makes future buyers go, "Hmm, that's a bit close for comfort."

And why should you care? Because when it comes time to sell, that lease is a huge part of your property's story. It’s not just about the bricks and mortar, darling. It’s about the right to be in those bricks and mortar. And if that right is on a timer, well, that changes the whole narrative, doesn't it?

Must Read

The Big Kahuna: How Much Does It Actually Cost You?

Okay, so the million-dollar question. How much does this whole short lease situation actually devalue your property? The truth is, there's no magic number. It’s not like saying, "Oh, a short lease chops off exactly 15% of the value." If only life were that simple, right? It’s more of a… feeling. A gut feeling. A nervous twitch when you’re trying to sell.

But let’s get real. It definitely has an impact. A significant impact, sometimes. Imagine you're buying a car. You see two identical cars, same mileage, same condition. One has a warranty that runs for another five years, and the other is fresh out of warranty. Which one are you leaning towards? The one with the peace of mind, right? Your property is kind of the same, but with a much bigger price tag and way more emotional investment.

Buyers, especially savvy ones, know that a short lease means they’ll have to deal with extending it sooner rather than later. And trust me, extending a lease isn't always a walk in the park. It can be expensive, time-consuming, and sometimes, downright frustrating. So, they'll factor that hassle, that potential future cost, into their offer now.

The Market Dictates, My Friend

The real answer, honestly, lies with the market. What's happening in your neck of the woods? Are properties with short leases flying off the shelves because there's a shortage of desirable places? Or are they sitting there, gathering dust, while perfectly lease-bound properties are snapped up?

If you're in a super hot market, a short lease might be a speed bump, not a roadblock. People might be willing to overlook it for the right price or the perfect location. But in a cooler market? Oh boy. It can feel like trying to sell ice cream in Antarctica. People have choices, and they'll choose the path of least resistance, the one with the least amount of future lease-related drama.

Think about it from a lender's perspective too. Some mortgage lenders get a little… anxious about properties with very short leases. They're in the business of minimizing risk, and a lease that's ticking down fast can feel like a bit of a gamble. So, if a buyer can’t get a mortgage easily, that’s another door slammed shut, right?

The "What Ifs" That Linger

Let’s talk about the dreaded "what ifs." What if the lease extension costs way more than you expected? What if the landlord is being completely unreasonable? What if the law changes and makes extending even harder? These are the anxieties that whisper in the back of a potential buyer's mind, and they’re usually reflected in a lower offer. It’s like a built-in negotiation tactic for them, whether they admit it or not.

A property with a long, secure lease feels like a solid investment. A property with a short lease feels a bit more… temporary. And people want permanence, especially when they’re sinking a massive amount of cash into something. They want to feel like they're buying a home, not just renting the right to own for a limited time.

So, the devaluation isn't just about the number of years left. It's about the perceived risk. It’s about the unknown future costs and the potential headaches. And those are things that are notoriously hard to put a precise dollar figure on, but they are absolutely real. It’s the invisible tax on a short lease.

So, How Do You Quantify This Beast?

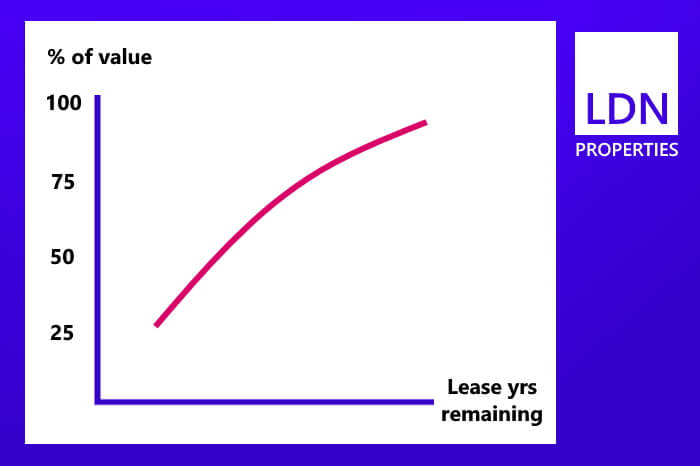

Right, you want numbers. I get it. It’s tempting to want a neat little percentage. But honestly, it's more about percentages of the potential value. If a property with a 100-year lease is worth, say, $500,000, a very similar property with only 50 years left might be worth significantly less. How much less? It could be anywhere from 5% to… well, a lot more. We're talking tens of thousands, potentially hundreds of thousands, depending on the lease length, location, and property type.

Some experts will tell you that for every year under a certain threshold (like 80 or 90 years), you might lose a certain percentage. But again, this is a generalization. It’s like trying to guess the exact amount of sugar in a cookie just by looking at it. You have a general idea, but the precise amount is a mystery until you measure.

The best way to get a feel for it is to look at comparable sales in your area. Are there properties with similar lease lengths that have sold recently? What were their prices like compared to those with longer leases? This is your closest bet to getting a real-world valuation. It's the detective work of real estate!

Beyond the Price Tag: The Intangible Hits

It’s not just about the sticker price, though, is it? A short lease can also affect the ease of selling. Imagine you're a seller. You've got this beautiful home, but the lease is a bit… dainty. You might find that your pool of potential buyers shrinks dramatically. Not everyone is comfortable or knowledgeable enough to deal with short leasehold properties. They might just scroll past, looking for something with a longer, more reassuring lease term.

And even among the buyers who are interested, you might face more tough negotiations. They know you're in a slightly weaker position, and they'll probably try to leverage that. So, while the price might be one thing, the amount of time it takes to sell and the stress involved can also be considered a form of devaluation, right? Your time and sanity have value too!

Think about the emotional attachment a buyer might feel. They’re dreaming of settling down, putting down roots. A short lease can introduce a sense of urgency and uncertainty that clashes with that dream. It’s like planning a long road trip and realizing your car’s gas tank is suspiciously small. You'll get there, but you'll be stopping a lot more often.

The Lease Extension Tango

Now, you might be thinking, "Okay, but I can just extend the lease!" And yes, you can! But as we touched on, it's not always straightforward. The cost of extending a lease can be… significant. It often depends on the ground rent, the current market value of your property, and the length of the extension you're seeking. And let me tell you, the landlord holds a lot of the cards in this particular game.

The longer you leave it, the more expensive it generally gets. It's like that leaky faucet you ignore. It's a small drip now, but if you wait too long, it can turn into a full-blown flood that costs a fortune to fix. So, the devaluation from a short lease can also be amplified by the potential cost of rectifying it.

And the process itself? It can be a bureaucratic maze. You might need solicitors, surveyors, and a whole lot of patience. It's not a quick weekend project. This is another reason why buyers might shy away. They see the lease length, they do a quick mental calculation of extension costs and hassle, and they decide it’s just not worth it compared to a property with a longer lease.

Who is Least Affected?

So, is everyone doomed with a short lease? Not necessarily. There are some situations where the devaluation might be less dramatic. For instance, if you’re in a very niche market where short leases are the norm, or if the lease extension process is exceptionally straightforward and affordable in your specific area. It’s rare, but not entirely impossible.

Also, if you’re selling to someone who is intending to immediately extend the lease, and they’ve factored that cost and process into their offer, the impact might be mitigated. They see it as a project, not a permanent problem. But even then, they’ll want a discount for taking on that project, won’t they? It’s always about compensating for the perceived inconvenience or risk.

Another factor is the type of property. A flat in a block with a shared ground rent might be viewed differently than a standalone house with its own leasehold. The dynamics can change. But generally speaking, the shorter the lease, the bigger the headache, and the bigger the headache, the bigger the potential devaluation.

The "Too Short" Threshold

When does a lease become "too short" to ignore? This is where things get fuzzy again. Generally, leases under 80 years start to raise eyebrows. But anything under 70, and especially under 50, is usually where you see the most significant impact. Some might even say that a lease with less than 30-40 years remaining can make a property very difficult to sell, or at least, very difficult to sell at its full market value.

Think of it like a wedding anniversary. 50 years is golden, right? A big deal. But if your lease is coming up on its 50th birthday, it’s less of a celebration and more of a "what are we doing about this?" situation. It’s reaching a point where the future feels a bit uncertain, and that uncertainty translates to a lower perceived value.

The closer you get to the end, the more urgent the need to address it becomes, and the more leverage the leaseholder has. So, the devaluation isn't linear. It can accelerate as the lease gets shorter. It’s like a snowball rolling downhill, gathering momentum and size.

So, What’s the Takeaway?

Look, the bottom line is this: a short lease is almost certainly going to devalue your property. How much? It’s a bit of a crystal ball situation, heavily influenced by your local market, the specific lease terms, and the general economic climate. But it’s a real devaluation, not just a myth or a buyer’s ploy.

It impacts the price, the ease of sale, and the pool of potential buyers. It introduces risk and uncertainty, which are the enemies of a good property investment. So, if you're thinking of selling a property with a short lease, be prepared for that conversation. Do your homework, get valuations, and understand the potential costs and complexities of extending the lease. It’s better to be informed than surprised, right?

And if you’re buying a property with a short lease? Well, do your due diligence with gusto! Get a surveyor, talk to a solicitor specializing in leasehold, and always factor in the cost and hassle of extension. A seemingly good deal can quickly turn sour if you haven’t fully grasped the leasehold implications. It's a bit like buying a stunning vintage dress – it might be beautiful, but you need to make sure it fits and that you know how to care for it properly. Don't let that lease be a hidden moth hole!

Ultimately, a short lease is a factor that will be considered. It's not the end of the world, but it's definitely something you need to be aware of and plan for. So, keep that coffee warm and that knowledge flowing. Happy property hunting (or selling)!