How Much Do You Take Home On 30000

So, you're eyeing that $30,000 salary, huh? That sounds pretty darn good, right? Like, "hey, I can actually buy avocado toast whenever I want" good. But then, BAM! Reality hits. You start wondering, "Okay, but how much of that actually lands in my bank account? Like, the real money I can spend on, you know, life?" It's like that moment you order a giant, delicious-looking cake, and then the waiter brings out the bill, and you're like, "Wait, where did all the frosting go?"

Seriously though, that's a super common question. Most people, when they see a salary number, they imagine that's what they're getting. A nice, round, easy-to-visualize figure. But oh, honey, it's a bit more complicated than that. Think of it like planning a fabulous vacation. You budget for flights and hotels, but then there are all those little extras, you know? The souvenir magnet, the overpriced-but-worth-it gelato, the "just in case" travel insurance. It all adds up, doesn't it?

So, let's break down this $30,000 magic number. We're talking about your gross income here. That's the big cheese, the total amount before anything gets nicked, uh, I mean, deducted. Think of it as the whole pie. Delicious! But, spoiler alert, you don't get the whole pie. Someone's always got a slice in mind, and in this case, it's the government, and sometimes your employer.

Must Read

First up, the biggie: taxes. Ugh, taxes. The necessary evil, right? We all gotta contribute to the good stuff, like roads (sometimes paved!), schools (hopefully with actual pencils!), and all that jazz. But man, they can take a chunk. Now, the exact amount you pay in taxes depends on a bunch of things. It's not like there's a universal tax stamp that says "$30,000 = X dollars." Nope.

We're talking about things like your filing status. Are you single and ready to mingle (and pay taxes solo)? Or are you married, filing jointly, maybe sharing the tax burden with your boo? This can make a difference, believe it or not. It's like deciding whether to split the bill at dinner or go Dutch. Sometimes one way is just… kinder to your wallet.

Then there are deductions and credits. Ah, the sweet relief! These are the things that can actually lower the amount of income the government taxes. Think of them as coupons for your tax bill. Are you a student? Do you have kids? Do you own a home and pay mortgage interest? Do you make charitable donations? These can all chip away at your taxable income, making that tax bill a little less scary. It’s like finding a forgotten $20 bill in your coat pocket – pure joy!

But for a $30,000 salary, let's be honest, you're probably not hitting those super-fancy deduction categories like owning a mansion and investing in Bitcoin. You'll likely be taking the standard deduction. This is a fixed amount that most people can just claim without having to itemize a million little expenses. It's the easy button for taxes. And that's fine! It simplifies things, right?

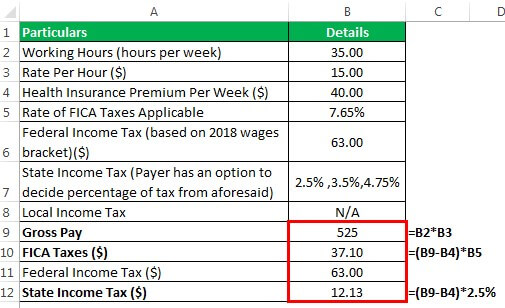

So, let's do some super-duper rough math here. We're not tax lawyers, okay? This is coffee-chat math. For $30,000 a year, if you're single, after the standard deduction and typical federal income tax rates (which, by the way, are progressive, meaning higher earners pay a higher percentage – fair enough, I guess!), you might be looking at somewhere in the ballpark of, say, 10-12% going to federal income tax. So, maybe around $3,000 to $3,600 a year. Crazy, right?

But wait, there's more! We haven't even touched on state income tax. Yup. Depending on where you live, your state might want its own slice of that $30,000 pie. Some states have no income tax at all – lucky ducks! Others can be pretty hefty. This can add another, say, 3-7% (or even more in some places!) to your tax burden. So, another $900 to $2,100 or so could be heading out the door.

And then there's FICA taxes. This is Social Security and Medicare. This one's a flat rate, set by the feds. It's currently 7.65% of your gross pay. This is non-negotiable, folks. This is the money that helps fund our current retirees and our healthcare system. So, for $30,000, that's a cool $2,295 taken out for FICA. Every. Single. Year. It's like a mandatory savings plan for… well, for the future. Hope it's there when we need it, right?

So, let's add it all up, just for a rough estimate. Federal income tax (let's say $3,300), state income tax (let's say $1,500, because who knows where you live!), and FICA ($2,295). That's already around $7,095 in taxes just from these main ones. So, out of your $30,000, you've already seen about $7,095 disappear. Poof! Like a magic trick you didn't ask for.

Now, what's left is your net income, or what we affectionately call your "take-home pay." So, $30,000 - $7,095 = $22,905. Still not bad, right? That's over $22,000 you can actually use. That’s pretty decent for a lot of places. You can definitely live on that, especially if you're smart with your money.

But hold up! We're not done with the deductions yet. What about health insurance? If your employer offers it, and most do, you'll likely have a premium that gets taken out of your paycheck. This can vary wildly. Are you getting a super-basic plan, or a Cadillac plan with all the bells and whistles? Let's say it's, oh, $50 a month for your share. That's $600 a year. Okay, not a huge dent, but it's another chunk.

Then there are things like retirement contributions. Are you putting money into a 401(k) or a similar plan? This is a smart move! Seriously, future you will thank you. Even if it's just a small percentage, like 3% of your salary ($900 a year), that's another amount that won't hit your checking account right away. But hey, it's for your future self, so that's a good kind of "gone." Think of it as a delayed gratification party for retirement.

What about other deductions? Maybe you have to pay for parking at work, or there's a union due, or you're contributing to a flexible spending account (FSA) for medical or dependent care. These all trim down your take-home pay a little more. It’s like the little surprise fees that pop up on an online purchase – annoying, but sometimes unavoidable.

So, let's do a revised calculation. We had $22,905 after taxes. Now, let's subtract our estimated health insurance ($600) and retirement contributions ($900). That brings us down to $21,405. See? It's a moving target, this take-home pay thing.

Now, it's crucial to remember that these are just estimates. Seriously. Your actual take-home pay could be a bit higher or a bit lower. The best way to know for sure? Look at your pay stub! That's where all the magic (and the deductions) is laid out in glorious detail. It's like the report card for your paycheck.

Think about it this way: if you're living in a state with no income tax, and you opt out of employer-sponsored health insurance (which, uh, maybe not the best idea, but people do it!), and you contribute nothing to retirement, your take-home pay would be much closer to that $22,905 mark. But if you're in a high-tax state, paying for premium health insurance, and maxing out your 401(k) contribution, your take-home could be significantly less.

So, what's the bottom line? On a $30,000 gross salary, you're probably looking at a net income somewhere between, say, $18,000 and $24,000 per year. That's a pretty wide range, I know! But it's the reality of how taxes and deductions work. It's not a straight-up division of $30,000 by 12 months. It's more like a carefully curated budget that gets whittled down before it even reaches you.

And that's okay! Knowing this is actually a superpower. When you understand how much you actually have to spend, you can budget better, save more effectively, and avoid those "where did all my money go?" moments. It's like knowing the ingredients of your favorite recipe – you can make it yourself, and maybe even make it better!

So, next time you see a salary advertised, don't just focus on the big, shiny number. Remember all the bits and bobs that come out before it gets to you. It’s a bit like buying a house – you don’t just look at the sticker price; you factor in the mortgage, the taxes, the insurance, the repairs… you know the drill. It's all part of the financial adventure!

Ultimately, $30,000 is a solid starting point for many. It's enough to live comfortably in many parts of the country, especially if you're mindful of your spending. But it’s definitely not "set for life" money. It's more like "build a good foundation and plan for the future" money. And that's a really important stage to be in!

So, cheers to understanding your paystub and to making smart financial decisions! Now, who wants another coffee?