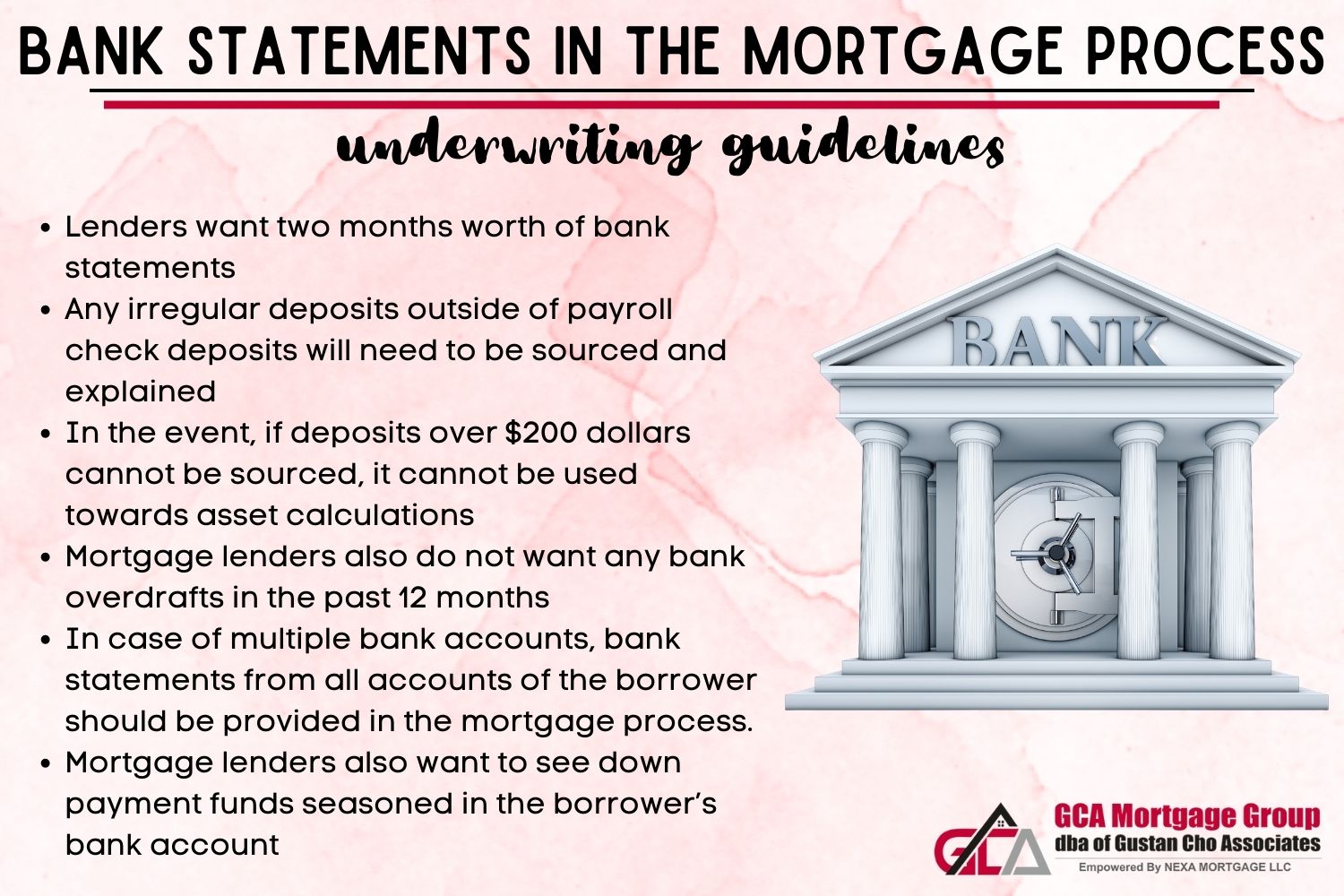

How Many Months Bank Statements For Mortgage

So, you're dreaming of that perfect pad, the one with the picket fence, the fancy kitchen, or maybe just a slightly bigger closet. Awesome! Getting a mortgage can feel like unlocking a secret level in a video game, and one of the keys you'll need involves your bank statements. Think of them as your financial report card, showing lenders how well you've been managing your hard-earned cash.

Now, a question that pops up more often than a rogue popcorn kernel is: "How many months of bank statements do I actually need to gather?" It's a fair question, and the answer isn't as complicated as deciphering ancient hieroglyphs. In fact, it's pretty straightforward!

The Magical Number: It's Usually Two!

Drumroll, please! For most mortgage applications, the magic number of bank statements you'll need is two months. Yep, just two! It’s like needing to show you’ve practiced your scales twice before you can get to the grand finale.

Must Read

This is generally for your checking accounts and your savings accounts. Lenders want to see a consistent pattern of how you handle your money on a regular basis. It’s not about showing them your entire financial history since the dawn of time, but rather a recent snapshot.

Think of it this way: if you were showing someone your favorite dessert recipe, you wouldn't pull out the ancient, stained cookbook from your grandma's attic, right? You'd show them the version you use now, the one that consistently delivers deliciousness. Your bank statements are kind of the same idea!

Why Two Months? A Little Lender Logic

So, what's the rhyme or reason behind this two-month rule? Lenders are basically playing detective. They want to make sure you're not suddenly transferring a massive sum of money from a secret offshore account (don't worry, most of us don't have those!) or receiving a bunch of "gifts" that aren't really gifts.

They're looking for stability and transparency. Two months gives them enough information to see your typical income deposits, your regular bill payments, and how you manage your day-to-day finances without being overwhelming.

It’s about building trust. If your statements show a steady flow of money and responsible spending habits, lenders feel more confident that you can handle the responsibility of a mortgage. It’s like seeing a student consistently do their homework – the teacher knows they’re prepared for the test!

What If I Have More Than One Account?

Now, what if you’re a financial maestro with a symphony of accounts? Maybe you have a checking account, a primary savings account, and a separate "future down payment" savings account that’s practically overflowing with dreams. That's fantastic!

For each of these accounts that you're using to show your financial health, you'll generally need to provide two months of statements. So, if you have three primary accounts you want to highlight, you’ll be gathering six statements in total.

It’s like packing for a trip. You might have a carry-on for essentials, a checked bag for clothes, and a little backpack for snacks. Each serves a purpose, and you need to show what's in each relevant bag!

Don't Forget the "Gifted Funds" Scenario!

Ah, the generous relatives! If a significant portion of your down payment comes from a loving gift from family, lenders will want to see extra documentation. This is where things can get a little more detailed, but don't sweat it!

Along with your regular two months of statements, you'll typically need a gift letter from the donor. This letter states that the money is a genuine gift and does not need to be repaid. It's like a formal thank-you note for the lender!

And, just like with your own accounts, they’ll want to see two months of statements from the account where the gifted funds were deposited. This shows the money arrived and settled into your account, proving it's truly yours to use for the down payment. No funny business allowed, just good old-fashioned generosity!

The "Other" Accounts to Consider

Sometimes, lenders might peek at other types of accounts. If you have investment accounts or retirement funds that you're using as a secondary source of funds or to show overall financial strength, they might ask for statements from those too.

The timeframe for these can sometimes stretch a bit longer, perhaps three to six months. This is because the value of investments can fluctuate more than a simple savings account. They want to see the recent trend, not just a one-day snapshot.

It’s like checking the weather report for a longer forecast. They want to see if it’s been consistently sunny (or consistently stable!), not just if it’s raining right now. So, keep those investment statements handy, just in case!

What NOT to Do with Your Bank Statements

Here’s where we get a little playful. Imagine your bank statements are like precious jewels. You wouldn’t want to smudge them with jam, would you? Or worse, try to hide a suspiciously large withdrawal for a solid gold trampoline!

Do NOT make any massive, unusual withdrawals or deposits right before applying for a mortgage. This is a big no-no! It can raise red flags faster than a matador spots a bull.

And please, for the love of all things financially sound, do NOT alter your bank statements. Lenders have sophisticated ways of detecting even the tiniest of "enhancements." It’s like trying to paint over a crack in the wall; it’s only a matter of time before it shows.

The Power of a Clean Financial Record

The goal is to present a clear, consistent, and honest picture of your finances. Two months of statements for your main accounts are the standard because they usually show this effectively. It’s the financial equivalent of a good, solid handshake – trustworthy and to the point.

So, when you’re gathering your documents, aim for those two months of recent statements for your primary checking and savings accounts. It’s the most common requirement and the simplest way to get started on your mortgage journey.

Think of yourself as a financial rockstar, ready to present your hit album of statements. Two months is your lead single, and it's a chart-topper!

A Quick Checklist for Your Statement Quest

Here’s a super-duper easy rundown:

- Checking Accounts: 2 months of statements.

- Savings Accounts: 2 months of statements.

- Gifted Funds: 2 months of statements for the account receiving the gift, plus a gift letter.

- Other Accounts (Investments, etc.): Potentially 3-6 months, depending on lender.

Remember, these are general guidelines. Your specific lender might have slightly different requirements. It’s always a brilliant idea to ask your loan officer directly about their exact needs. They are your friendly guides on this mortgage adventure!

Armed with this knowledge, you can tackle your bank statement gathering with confidence and maybe even a little bit of pizzazz! Go forth and conquer your mortgage dreams, one statement at a time!