How Long Do Late Payments Stay On Your Credit Report

Okay, so picture this: I was a young’un, just starting out in the glorious world of adulting. And, you know, that first credit card? It felt like a golden ticket to… well, to buying slightly nicer ramen and maybe a few more impulse buys than I should have. Life was good. Until, BAM! A bill arrived that I completely, utterly, and embarrassingly forgot about. Just… vanished from my brain like a sock in the dryer.

It wasn't a huge amount, nothing catastrophic. But that little red “Late Payment” notification on my statement? It felt like a scarlet letter. I remember stressing about it for weeks. Would this one little slip-up ruin my entire financial future? Was I doomed to a life of rejected loan applications and judging stares from potential landlords?

That little scare got me thinking, and honestly, it’s something a lot of us wonder about when that dreaded notification pops up or we realize we've missed a payment. So, let's dive into it, shall we? We're talking about the nitty-gritty of how long those late payments, those little financial oopsies, actually stick around on your credit report. Because knowledge, my friends, is power. And in this case, it’s the power to stop a tiny mistake from becoming a massive, looming anxiety.

Must Read

The Not-So-Secret Life of Late Payments

Alright, let's get straight to the point. The magic number you're probably looking for is seven years. For most types of negative information, including late payments, that's how long they typically stay on your credit report. Yep, a whole seven years. It sounds like a long time, right? Especially when you’re the one who made the late payment. It feels like it’s going to be there forever, judging you every time you try to get a new phone contract.

But here's the kicker: while it's on your report for seven years, its impact starts to fade much, much sooner. Think of it like a bad haircut. In the first few weeks, it’s all anyone can see. You feel self-conscious. But after a few months, it grows out, and people barely notice. Your credit report is kind of like that, but with a much longer growth cycle.

What Exactly Counts as a "Late Payment"?

Before we get too deep, let's define what we're talking about. A late payment usually means you've missed the due date by 30 days or more. Most lenders are pretty forgiving for a day or two. You know, life happens. But once you hit that 30-day mark, that's when they typically report it to the credit bureaus (Equifax, Experian, and TransUnion).

So, if you pay your bill on the 15th and the due date was the 10th, you might get a late fee, but it likely won't hit your credit report immediately. However, if you don't pay it by, say, the 10th of the next month, you're definitely in late payment territory. And that's when the clock on those seven years starts ticking.

The Seven-Year Itch (for Your Credit Report)

So, that seven-year rule applies to most negative marks. This includes:

- 30-day late payments

- 60-day late payments

- 90-day late payments

- And even more severe delinquencies like 120+ days late

It also applies to things like collections, charge-offs, bankruptcies (though bankruptcies can sometimes stay longer, like 10 years, depending on the type), and foreclosures. It's like a general statute of limitations for bad credit behavior, at least as far as what the credit bureaus are allowed to keep on your file.

Now, this isn't some arbitrary number pulled out of thin air. It's actually governed by the Fair Credit Reporting Act (FCRA). This law is designed to protect consumers by preventing old, irrelevant negative information from haunting you forever. It ensures that your credit report reflects your current financial standing, not ancient history.

The Nuances: When the Seven-Year Clock Might Start

Here's where it gets a little… fuzzy. For a missed payment, the seven-year clock usually starts from the date of the delinquency. That means the date you first became 30 days late. So, if you're late on January 10th and pay it off on February 5th, the seven years technically starts ticking from January 10th.

But what about collection accounts? If a debt goes to collections, the FCRA allows creditors to report the collection account for seven years from the date of the last activity on the original account. This can sometimes be a bit confusing because "last activity" can be interpreted in different ways. Usually, it's from the date the account became delinquent with the original creditor.

And then there are judgments. Civil judgments related to debt can stay on your report for seven years from the date the judgment was entered, or until the legal statute of limitations for enforcing the judgment expires, whichever is longer. This is why those court-related issues can sometimes stick around for a bit.

The Fading Power of a Late Payment

Okay, so seven years is the lifespan, but that doesn't mean the impact is consistent throughout. The truth is, the closer a late payment is to the present, the more it will hurt your credit score. As time goes by, its influence diminishes.

Think of it like this: a 30-day late payment from last month is going to have a significantly bigger negative effect on your score than a 30-day late payment from six years ago. Lenders are primarily interested in your recent behavior. They want to know if you're a reliable borrower now.

The Severity Scale: 30 vs. 60 vs. 90+

It's also important to remember that not all late payments are created equal in the eyes of your credit score. A single 30-day late payment, especially if it's an isolated incident and you have a generally good credit history, will have a less severe impact than multiple 60-day or 90-day late payments, or a pattern of consistent late payments.

A 60-day late payment tells lenders you struggled for longer. A 90-day late payment (or more) is a serious red flag. It signals a significant inability to manage your finances. These more severe delinquencies will drag your score down more dramatically and will continue to have a stronger negative influence for longer, even as they age.

What Happens When the Seven Years Are Up?

This is the part you’ve been waiting for! Once that seven-year mark hits, the negative information, like that pesky late payment, is supposed to be removed from your credit report. Poof! Gone.

This removal is mandated by the FCRA. It’s not a courtesy; it’s a legal requirement. So, in theory, after seven years, that old late payment should no longer be visible to lenders when they pull your credit report.

The Catch: "Last Activity" Shenanigans

Now, while we’re talking about seven years, there’s a common pitfall, especially with collection accounts. As I mentioned, for collections, the seven years can sometimes be measured from the "date of last activity." If a creditor or collector makes a payment on a collection account, or even sends you a letter about it, this can sometimes reset the clock, or at least extend the reporting period based on when that activity occurred.

This is a really important distinction. For a simple late payment on your credit card that you eventually caught up on, the seven years usually starts from the first missed payment date. But for a debt that's gone to collections, you need to be extra careful about what constitutes "activity" and when that seven-year period is truly over. Sometimes, collectors will try to use this to keep reporting old debts for longer than they should.

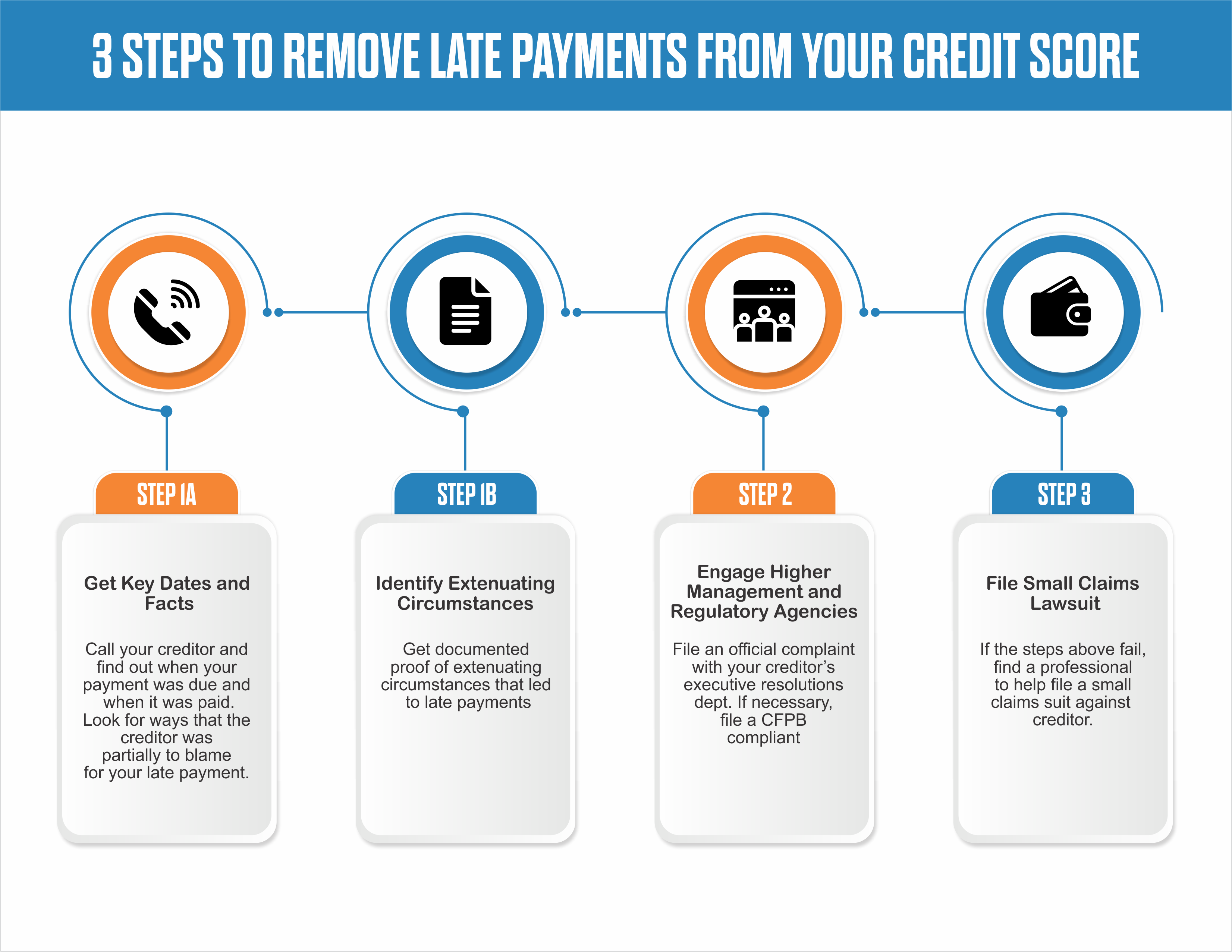

Can You Get a Late Payment Removed Sooner?

Ah, the million-dollar question! While the general rule is seven years, are there ways to expedite the process? Sometimes, yes! Here are a few scenarios:

- Errors: The most common way to get something removed sooner is if it's an error. If a late payment was reported incorrectly by the lender or the credit bureau, you have the right to dispute it. If your dispute is successful, they'll remove it. So, always check your credit reports regularly!

- Goodwill Letters: This is a long shot, but it's worth a try, especially for a single, isolated late payment. You can write a "goodwill letter" to the creditor explaining the situation (briefly and without making excuses!) and asking them to remove the late payment from your credit report as a gesture of goodwill. Some lenders might do it, especially if you're a long-time customer with a good payment history otherwise. Don't expect miracles, but it's a polite plea.

- Negotiation with Collection Agencies: If the late payment has resulted in a debt going to collections, and you negotiate a settlement, sometimes you can negotiate for the collection agency to agree to remove the negative mark from your report. This is rare, and they usually prefer to report it as "paid collection" (which is still negative but better than an unpaid one), but it's not impossible.

The Takeaway: Be Proactive and Patient

So, what’s the ultimate lesson here? First, try your absolute best not to be late on your payments. Set up autopay, set reminders, do whatever it takes. Those late fees are annoying enough, and the credit score ding is even worse.

Second, if you do have a late payment, understand that it’s not the end of the world. It will hurt your credit score, but its impact fades over time. The key is to demonstrate consistent, on-time payments moving forward. That's the best way to counteract the negative effects of past mistakes.

And finally, keep an eye on your credit reports. Check them at least once a year from AnnualCreditReport.com. If you see a late payment that shouldn't be there, or if you think it’s been on your report longer than the seven years allowed, dispute it. You have rights!

That forgotten credit card bill from my early days? Eventually, it just aged off my report. And in the meantime, I learned a very valuable lesson about responsibility, reminders, and not letting things slip through the cracks. It was a tough teacher, but the lesson stuck. And now, hopefully, you're armed with the knowledge to navigate your own credit report, no matter what little bumps you might encounter along the way.