How Do You Set Up A Trust Fund

So, you're thinking about trust funds, huh? That's pretty awesome! It sounds super fancy and complicated, like something only rich people in movies worry about. But guess what? Setting up a trust fund is actually a lot more accessible than you might think. Think of it as a way to be a super-organized, benevolent superhero for your loved ones, even when you're off… doing whatever awesome stuff you'll be doing! Let's break it down, no stuffy legal jargon allowed, promise!

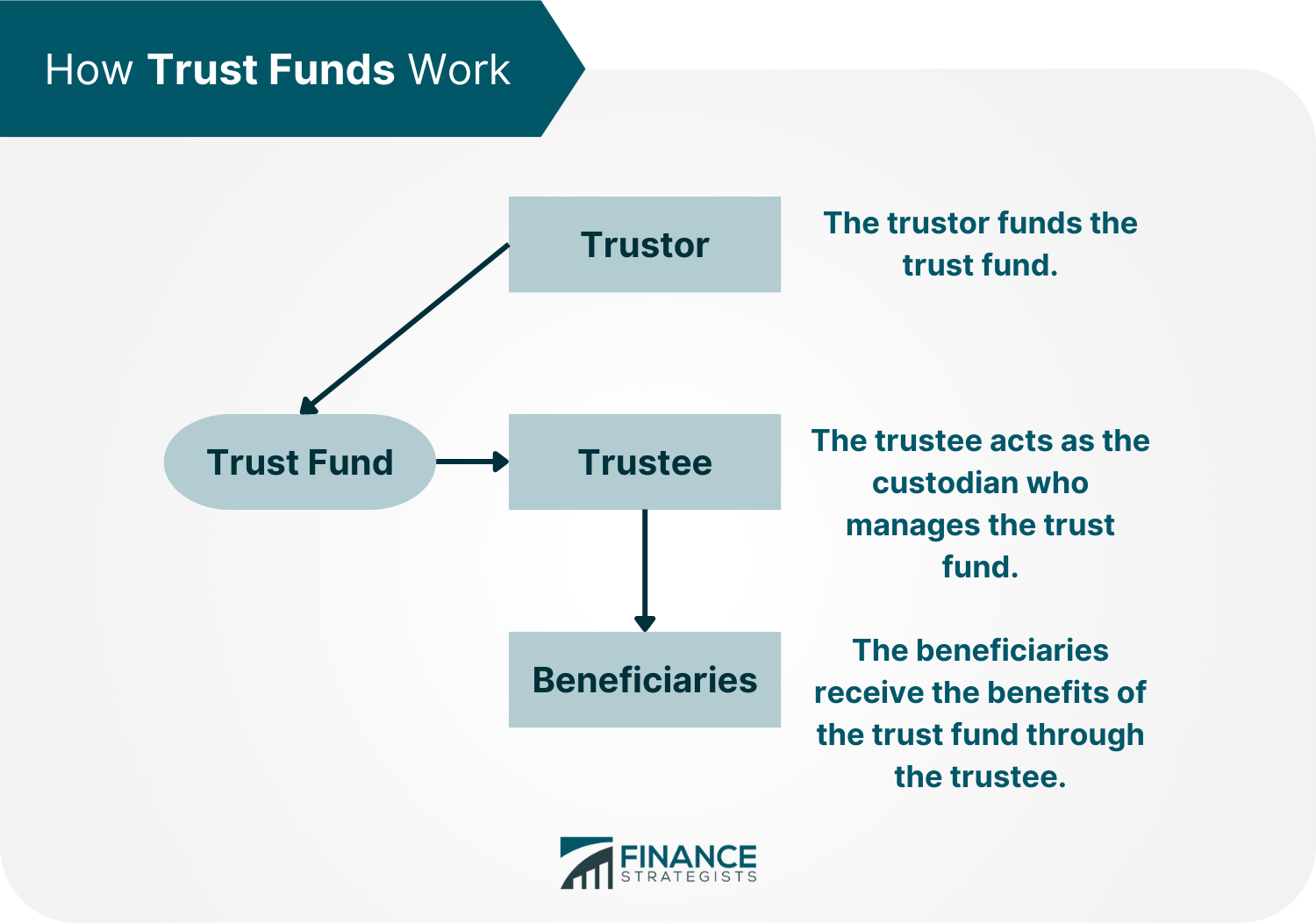

First things first, what is a trust fund, anyway? Imagine you have a special box. You put your treasures (money, property, that collection of vintage comic books you’re secretly hoarding) into this box. Then, you tell a trusted friend (we'll call them the "trustee" – sounds important, right?) who gets what from the box, and when. They're basically the cool guardian of your goodies, making sure everything goes to the right people according to your wishes. Easy peasy!

Why Bother With a Trust Fund? Aren't Wills Enough?

Great question! Wills are super important, no doubt. They're like the general instructions for your estate. But trusts have some extra superpowers. For starters, they can help you avoid probate. Probate is that official court process where your will gets scrutinized. It can be lengthy, public (so everyone knows your Aunt Mildred’s secret cookie recipe is going to you!), and sometimes a real drag. A trust, on the other hand, can often skip that whole song and dance. Your assets can be distributed much more quickly and privately. Think of it as a VIP express lane for your legacy.

Must Read

Another biggie is control. With a will, once it’s done, it’s pretty much set. With a trust, you can put in specific conditions. For example, you can say your kid can’t get their inheritance until they graduate college, or maybe they need to prove they’ve learned to, I don’t know, fold their laundry properly. (A noble goal, indeed!). You can also set it up to benefit beneficiaries over a long period, providing ongoing support instead of a lump sum that might disappear faster than free donuts in the breakroom.

Plus, if you’re thinking about estate taxes, a trust can be a super handy tool to potentially minimize those. It’s like getting a discount on your final farewell gift to your loved ones. (Disclaimer: I'm not a tax advisor, so definitely chat with one of those wizards for the nitty-gritty on this!).

Types of Trusts: Not All Trust Funds Are Created Equal!

Okay, so not all trusts are the same. It’s not a one-size-fits-all situation. The most common ones you’ll hear about are:

Revocable Living Trusts (The Flexible Friends)

These are the workhorses for many people. "Revocable" means you can change or cancel it while you're alive and well. "Living" means you set it up during your lifetime. This is your chance to get your affairs in order while you’re still here to, you know, enjoy life. You can tweak beneficiaries, change assets, or even dissolve the whole thing if you change your mind. It’s like having a draft document that you can continuously edit.

Think of it as your personal safety net. You're the boss, you can make changes, and it’s generally a pretty straightforward way to manage your assets and ensure they go where you want them to. You are the initial trustee, so you still have full control.

Irrevocable Trusts (The Stick-To-It-iveness Champs)

Now, these are a bit more permanent. Once you set up an irrevocable trust, it's very difficult, if not impossible, to change or revoke. This might sound scary, but it's often done for specific reasons, like significant tax advantages or asset protection. Because you're giving up a certain level of control, the IRS and creditors might see your assets as no longer belonging to you, which can be a good thing in certain situations.

These are the ones where you really need to know what you’re doing and have a solid plan. It's like committing to a really great tattoo – you want to be sure you love it forever!

Setting Up Your Trust: The Nitty-Gritty (But Still Fun!)

Alright, ready to roll up your sleeves? Here’s the general roadmap:

1. Figure Out Your "Why" and "What"

Before you even think about talking to a lawyer (though you totally will!), take some time for some serious reflection. What are your goals? Who do you want to benefit? What assets do you want to include? Be specific! Do you want your grandkids to have money for college? Or perhaps you want to set aside funds for a pet’s lifetime care? (Seriously, best gift ever to a furry friend!).

Jot down your thoughts. This clarity will make the whole process so much smoother. It’s like planning a road trip: you need to know your destination before you start packing.

2. Choose Your Trustee Wisely

This is a big one. Your trustee is the person (or institution) who will manage the trust and distribute your assets according to your instructions. They need to be:

- Trustworthy: Obvious, right? But seriously, this person will hold a lot of responsibility.

- Organized: They'll be dealing with paperwork, investments, and beneficiaries.

- Responsible: They need to make sound decisions and follow your wishes to the letter.

- Good with numbers (or willing to hire someone who is): Especially if you have investments.

This could be a family member, a close friend, or even a professional trustee from a bank or trust company. Consider the pros and cons. A family member might be more emotionally invested, but a professional might have more experience and objectivity. You can also name a successor trustee in case your first choice becomes unable or unwilling to serve. It's like having a backup quarterback!

3. Draft the Trust Document (This is Where the Lawyer Comes In!)

Okay, this is where you really need professional help. Trying to draft a trust document yourself is like trying to perform your own appendectomy. Don’t do it! You need an experienced estate planning attorney. They are the architects of your financial legacy.

Your attorney will guide you through the legalities, ensuring your trust document is legally sound and reflects your wishes precisely. They'll help you decide on the best type of trust for your situation, outline your beneficiaries, specify distribution rules, and handle all the legal jargon. Think of them as your trusty co-pilot for this journey.

They’ll ask you a ton of questions, probably more than you’ve been asked in years. Be patient and honest. This is the time to spill the beans about your financial empire (or humble kingdom!).

4. Fund Your Trust (The Magic Happens Here!)

This is the crucial step that many people overlook. A trust document is just a piece of paper if it doesn't contain anything! You need to transfer ownership of your assets into the trust. This is called "funding" the trust.

For example, if you want your house to be in the trust, you’ll need to re-title the deed to the trust’s name. If it’s money in a bank account, you’ll need to change the account to be held by the trust. For investments, you’ll work with your brokerage firm. This can involve a bit of paperwork, but it’s absolutely essential. It’s like buying a beautiful gift box, but then forgetting to put any presents inside!

Your attorney or their paralegal can help guide you through this process. Don't be afraid to ask them to explain each step. It's your money, your legacy – you have every right to understand it!

5. Maintain and Review

A trust isn't a "set it and forget it" kind of deal. Life happens! Your circumstances change, your beneficiaries' circumstances change, and laws can change. It's a really good idea to review your trust periodically, especially after major life events like a marriage, divorce, birth of a child, or death of a beneficiary.

Think of it as giving your trust a health check-up every few years. Does it still align with your goals? Are the beneficiaries still the right people? Is the trustee still the best fit? This proactive approach ensures your trust remains a powerful and effective tool for years to come.

:max_bytes(150000):strip_icc()/what-is-a-trust-fund-357254_final1-5b3e687ac9e77c00370bae43-72eaa014efbf46a9a42fd1b90a5251b9.jpg)

A Little More Trusty Advice

Don't let the word "trust" intimidate you. It’s a powerful tool that can bring peace of mind and ensure your wishes are honored. It’s about being thoughtful and proactive in how you care for your loved ones.

If you have minor children, a trust can be a lifesaver, ensuring they are provided for financially in a structured way, even if something were to happen to you. It’s like leaving them a roadmap and a toolkit, not just a pile of cash they might not know what to do with.

And hey, even if you don't have millions in the bank, a trust can still be incredibly valuable. It's about thoughtful planning for any amount of assets that matter to you and your family.

The Uplifting Finale!

So there you have it! Setting up a trust fund might sound like a monumental task, but when you break it down, it’s really about caring for your future and the future of those you love. It’s an act of love, really. It’s about saying, "I’ve thought about this, and I want to make sure things are handled smoothly and with care, even when I can’t be there myself."

Imagine the peace of mind that comes with knowing your loved ones will be taken care of, that your legacy will be managed according to your vision. It's like planting a beautiful tree that will provide shade and sustenance for generations to come. So go forth, my friend! Explore your options, chat with an attorney, and take that step towards securing your legacy. You’re not just setting up a trust; you’re crafting a beautiful chapter in your family’s story, a story that will continue to unfold long after you’ve moved on to your next grand adventure. And that, my friend, is a truly wonderful thing to smile about!