How Can I Do Payroll On My Own

Hey there, fellow hustlers and dream-chasers! Ever find yourself staring at that stack of invoices and a calendar that’s starting to look like a Tetris game gone wrong? Yeah, we get it. Running your own gig, whether it’s a cozy little bakery or a cutting-edge design studio, is all about passion and proving your vision. But then there’s the other stuff. The stuff that’s essential, the stuff that keeps the engine running, but can sometimes feel as exciting as watching paint dry. We’re talking about payroll.

Now, before you click away thinking, "Uh, payroll? Isn't that for suits and skyscrapers?" – hold up! Doing your own payroll, especially when you're just starting out or have a small team, isn't some insurmountable mountain. It's actually more like a scenic hike you can totally conquer with the right boots and a good playlist. Think of it as an act of self-care for your business. When you understand where every dollar is going, you’re in the driver's seat, not just a passenger. So, let’s ditch the dread and dive into how you can own this payroll thing, with a smile (mostly!).

The "Why" Behind the DIY Payroll Vibe

Okay, so why would anyone choose to do their own payroll when there are services for it? Great question! For starters, cost-effectiveness is a biggie. Outsourcing payroll can add up, especially when you're bootstrapping. Doing it yourself can save you a chunk of change that can be reinvested into, say, that artisanal coffee machine you've been eyeing for the breakroom (we see you!).

Must Read

Beyond the budget, there's a certain empowerment that comes with it. You’re not just handing over a task; you're actively managing a critical part of your business. It’s like learning to cook your favorite meal from scratch instead of always ordering takeout. You gain a deeper appreciation for the ingredients and the process. Plus, let's be honest, when it comes to your team, those people who are the backbone of your dreams, you want to be the one ensuring their hard-earned cash lands in their accounts accurately and on time. It’s about building trust and showing you’re invested.

Think of it this way: remember when you first learned to drive? A bit daunting, right? But now, you probably don't even think about it. You just hop in and go. Payroll can be like that. Once you get the hang of it, it becomes a smooth, routine part of your business operations. It’s a skill, and like any good skill, it’s learnable and manageable.

The Building Blocks: What You Actually Need

So, what’s in your payroll toolkit? Don't worry, it's not a toolbox full of intimidating spreadsheets and arcane tax forms. We're talking a few key things:

1. Know Your People: Employee Information is King

This is your foundation. You need to have accurate and up-to-date information for each employee. This includes:

- Full Name and Address

- Social Security Number (SSN): Essential for tax reporting.

- Pay Rate: Hourly wage, annual salary, or commission structure.

- Pay Frequency: Weekly, bi-weekly, semi-monthly, monthly?

- Tax Withholding Information: This comes from their W-4 form (or equivalent for non-US entities).

- Any Deductions: Health insurance premiums, retirement contributions, garnishments, etc.

It might sound like a lot, but think of it like collecting ingredients before you bake. You wouldn't start mixing without the flour, sugar, and eggs, would you? This information is your core recipe.

2. The Crown Jewels: Understanding Gross vs. Net Pay

This is where the magic (and the math) happens. Your gross pay is the total amount of money an employee earns before any deductions are taken out. It's their actual earnings based on their hours worked or salary.

Your net pay, on the other hand, is the amount that actually hits their bank account. This is after all the taxes, deductions, and other withholdings have been subtracted from the gross pay. It's the “take-home pay.” So, if your friend is making you a killer smoothie, gross pay is all the fruit, yogurt, and protein powder; net pay is the delicious, ready-to-drink beverage you actually sip.

3. The Tax Man Cometh: Federal, State, and Local Taxes

Ah, taxes. The one constant in life, right? This is probably the most complex part of DIY payroll, but it's totally navigable. You'll need to understand:

- Federal Income Tax: This is based on the employee's W-4 and the IRS tax brackets.

- Social Security and Medicare Taxes (FICA): These are fixed percentages of an employee's gross pay (up to certain limits for Social Security). You, as the employer, also have to match these contributions.

- Federal Unemployment Tax (FUTA): This is paid by employers to fund unemployment benefits.

- State Income Tax: If your state has an income tax, you'll need to withhold and remit it. Rules vary by state.

- State Unemployment Tax (SUTA): Similar to FUTA, but at the state level.

- Local Taxes: Some cities or localities also have their own income or wage taxes.

Fun Fact: Did you know that Social Security taxes in the US have a wage base limit? For 2024, it’s $168,600. Once an employee earns more than that in a year, you stop withholding Social Security taxes on their earnings above that amount. Medicare taxes, however, have no wage base limit!

The key here is to research your specific tax obligations. The IRS website is your best friend (yes, really!), and your state's department of revenue will have all the local details.

4. The Deductions Department: More Than Just Taxes

Beyond taxes, you might have other deductions to consider:

- Health Insurance Premiums: Employee contributions are usually pre-tax, meaning they reduce taxable income.

- Retirement Plan Contributions: Like 401(k)s or IRAs. These are often pre-tax too.

- Garnishments: These are court-ordered deductions for things like child support or debts.

- Other Benefits: Paid time off, disability insurance, etc., might factor in.

Keeping track of these requires clear communication with your employees and understanding the rules around pre-tax vs. post-tax deductions. It’s like managing a complex recipe with several optional ingredients – you need to know which ones affect the final flavor (and tax bill!).

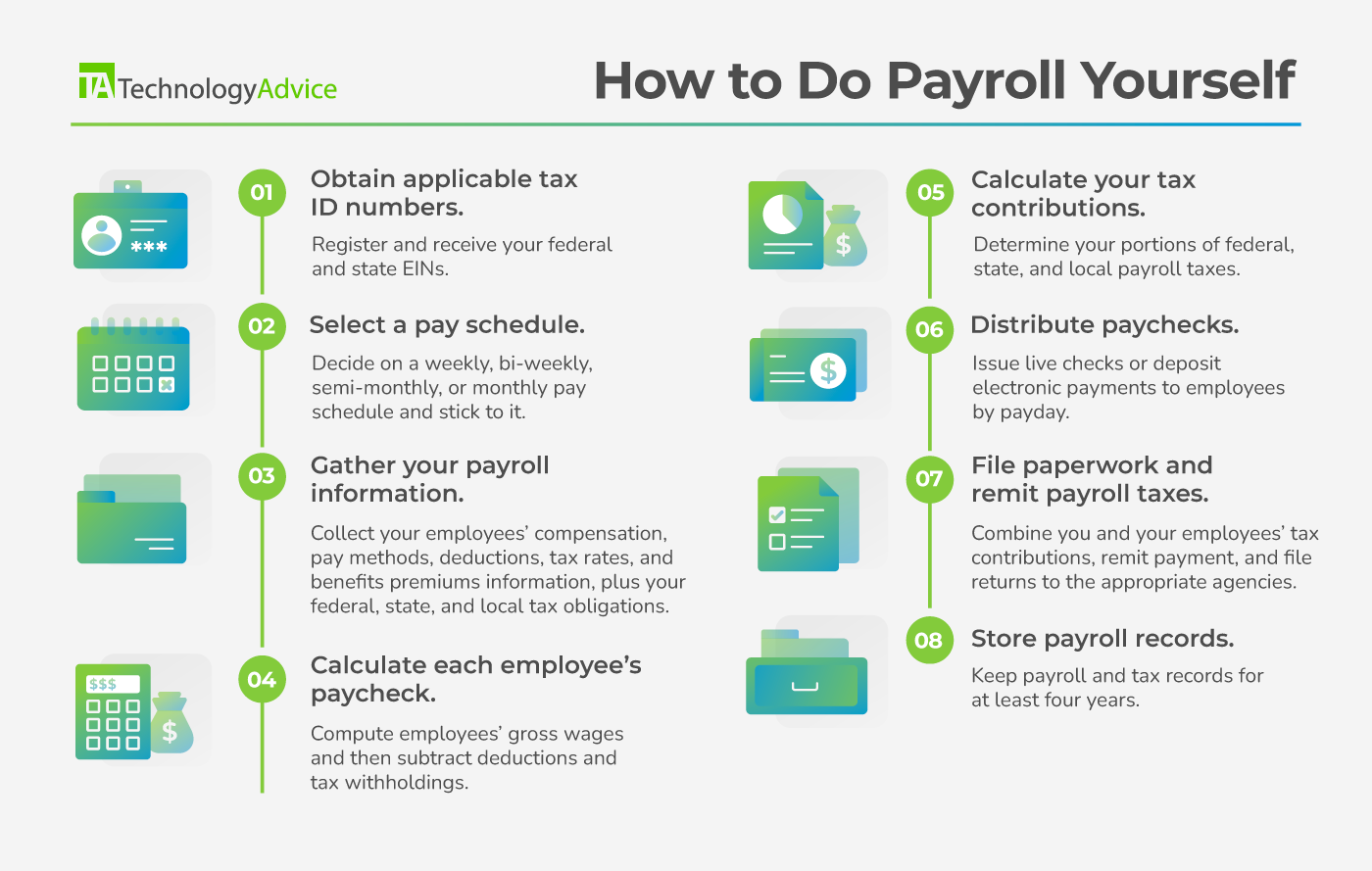

The Practicalities: How to Actually DO It

Okay, you’ve got the knowledge. Now, how do you execute? You’ve got a few paths:

1. The Spreadsheet Samurai Method

For the truly brave and numerically inclined, a well-structured spreadsheet can work. Think Microsoft Excel or Google Sheets.

- Set up your columns: Employee Name, Hours Worked, Rate, Gross Pay, Federal Tax, State Tax, FICA (Social Security & Medicare), FUTA, SUTA, Deductions, Net Pay.

- Use formulas: This is where the magic happens. Link cells so calculations are automatic. For example, Gross Pay = Hours Worked * Rate.

- Keep it updated: This is crucial. Any change in hours, rates, or deductions means updating the sheet.

- Separate tabs: You might have a tab for employee data, a tab for weekly payroll calculation, and a tab for tax summaries.

Pro Tip: There are tons of free payroll spreadsheet templates online. Start there and adapt it to your needs. It's like finding a great recipe online and tweaking it to your taste!

Cultural Nugget: Spreadsheets have been around since the late 1970s (VisiCalc was a pioneer!). They’ve evolved, but the core concept of organizing data visually and performing calculations remains, a testament to their enduring utility. They're the unsung heroes of so many businesses.

2. Payroll Software: Your Digital Sidekick

If spreadsheets make you break out in a sweat, or if you have more than a handful of employees, payroll software is your best friend. Many affordable options are designed for small businesses.

- Features to Look For: Automatic tax calculations, direct deposit capabilities, employee self-service portals, and reporting tools.

- Ease of Use: Choose software with a user-friendly interface. You don’t want to spend hours figuring it out.

- Customer Support: A good support team can be a lifesaver when you hit a snag.

Popular Options (do your own research!): QuickBooks Payroll, Gusto, Xero Payroll, Patriot Payroll. Each has its own strengths and pricing models.

Think of payroll software as hiring a super-organized, always-available assistant who’s a whiz with numbers. They handle the heavy lifting of calculations and compliance, freeing you up for more strategic thinking.

The Cadence: When and How to Pay

Consistency is key! Your chosen pay frequency dictates when you run payroll:

- Weekly: You’ll run payroll 52 times a year. Often for hourly workers.

- Bi-weekly: You’ll run payroll 26 times a year. Most common for hourly and salaried.

- Semi-monthly: You’ll run payroll 24 times a year, usually on specific dates (e.g., the 15th and 30th). Often for salaried employees.

- Monthly: You’ll run payroll 12 times a year. Less common for general employees, more for specific contracts or executive pay.

The Process:

- Gather Hours/Data: Collect timesheets or confirm salary and deduction changes.

- Enter Data into Software/Spreadsheet: Input all the necessary information.

- Review Carefully: Double-check everything! A small typo can lead to big headaches.

- Run Payroll: Generate pay stubs and the payroll register.

- Process Payments: Initiate direct deposits or prepare checks.

- Remit Taxes: Make sure your tax payments are made on time to the correct authorities.

Pro Tip: Schedule your payroll runs in your calendar! Treat it like an important meeting you can’t miss.

Reporting and Remitting: The Paper Trail

This is where you show the government (and yourself) that you've got it all under control. You'll be dealing with forms like:

- Form 941 (Employer's Quarterly Federal Tax Return): Reports your federal income tax, Social Security tax, and Medicare tax withholdings.

- Form 940 (Employer's Annual Federal Unemployment Tax Act Return): Reports FUTA taxes.

- Form W-2 (Wage and Tax Statement): Given to employees and filed with the Social Security Administration, reporting their annual wages and taxes withheld.

- Form W-3 (Transmittal of Wage and Tax Statements): A summary of all W-2s.

- State and Local Tax Forms: These vary significantly by location.

When to File?

- Quarterly for Form 941.

- Annually for Form 940, W-2s, and W-3.

- State and local requirements will have their own schedules.

Crucial Point: Timely tax remittance is non-negotiable. Penalties for late payments can be hefty and quickly erode any savings from doing payroll yourself. Make sure you know the deadlines and set reminders.

Troubleshooting Your Payroll Prowess

Even with the best intentions, you might encounter bumps in the road. Here are some common issues and how to handle them:

- Incorrect Tax Calculations: Double-check your tax tables and formulas. Ensure you’re using the correct tax year’s rates.

- Over/Underpayments: Mistakes happen. If you overpay, you'll need to recover the funds from the employee (with their agreement and adherence to labor laws). If you underpay, you'll need to issue an additional payment promptly.

- Missed Deadlines: If you miss a tax deadline, contact the relevant tax agency immediately. They can often work with you to set up a payment plan and may waive penalties if you can show it was an honest mistake and you’re rectifying it.

- Employee Changes: A change in an employee's pay rate, marital status (affecting W-4), or deductions requires immediate adjustment in your payroll system.

The Golden Rule: When in doubt, consult a professional. It might cost a little, but a tax advisor or payroll specialist can save you a lot of pain and potential fines. Think of it as an insurance policy for your payroll operations.

The Joy of the Direct Deposit

If you’re using payroll software or a bank that offers it, direct deposit is a game-changer. It’s efficient, secure, and a definite perk for your employees.

Benefits for Employees:

- Convenience: No more rushing to the bank.

- Security: Reduces the risk of lost or stolen checks.

- Faster Access to Funds: Money is available on payday.

Benefits for You:

- Efficiency: Streamlines the payment process.

- Reduced Paperwork: No physical checks to print or manage.

- Traceability: Clear record of payments.

Setting up direct deposit usually involves getting employees to fill out a form with their bank account and routing numbers. Easy peasy!

A Little Reflection: Payroll as Part of Your Journey

Doing your own payroll can feel like one of those adulting responsibilities that’s a little less glamorous than designing a killer logo or landing a big client. But here’s the thing: it’s also incredibly empowering. It’s about taking ownership of every aspect of your business, from the big creative leaps to the quiet, essential mechanics.

Think about it: when you make your morning coffee, you’re not just brewing a drink; you’re setting the tone for your day. You’re in control of that simple ritual. Doing your payroll yourself is similar. It's a deliberate act of managing your business’s well-being, ensuring that the people who help you build your dreams are compensated fairly and accurately. It’s a way of saying, "I see you, I value you, and I’m meticulously handling the details that matter."

So, the next time you approach payroll, don't groan. Take a deep breath. You’ve got this. You’re not just processing numbers; you’re fueling your business and nurturing your team. And that, my friends, is a pretty awesome feeling. Keep building, keep dreaming, and keep your payroll in order – the journey is yours to command!