Do You Pay Tax On Personal Pension

Hey there, future retiree! Ever find yourself staring at your payslip, or maybe just daydreaming about a comfy future filled with… well, whatever makes you happy? You've probably heard the whispers, the gentle nudges, about pensions. And then the inevitable question pops into your head: "Do I actually have to pay tax on my personal pension?" It's a super valid question, and honestly, it's not as scary as it might sound. Let's dive in, shall we? Think of this as a friendly chat, not a lecture from your tax inspector!

So, what's the deal with pension tax? The short answer is: it's a bit of a mixed bag, but mostly in a good way! We're talking about how the money you put into your pension and the money you take out are treated by HMRC (that's Her Majesty's Revenue and Customs, for the uninitiated). It's all designed to encourage you to save for your golden years. And who doesn't want to be a golden-ager, right?

The Magic of Tax Relief: Getting Money Back!

Let's start with the really good stuff: the money going in. This is where things get pretty sweet. When you contribute to a personal pension, you usually get something called tax relief. What does that even mean? Well, imagine you earn £100, and a chunk of that is taxed. But if you pop that money into your pension, it's like the tax man says, "Okay, you're saving for later, good on you! Let's knock some tax off that."

Must Read

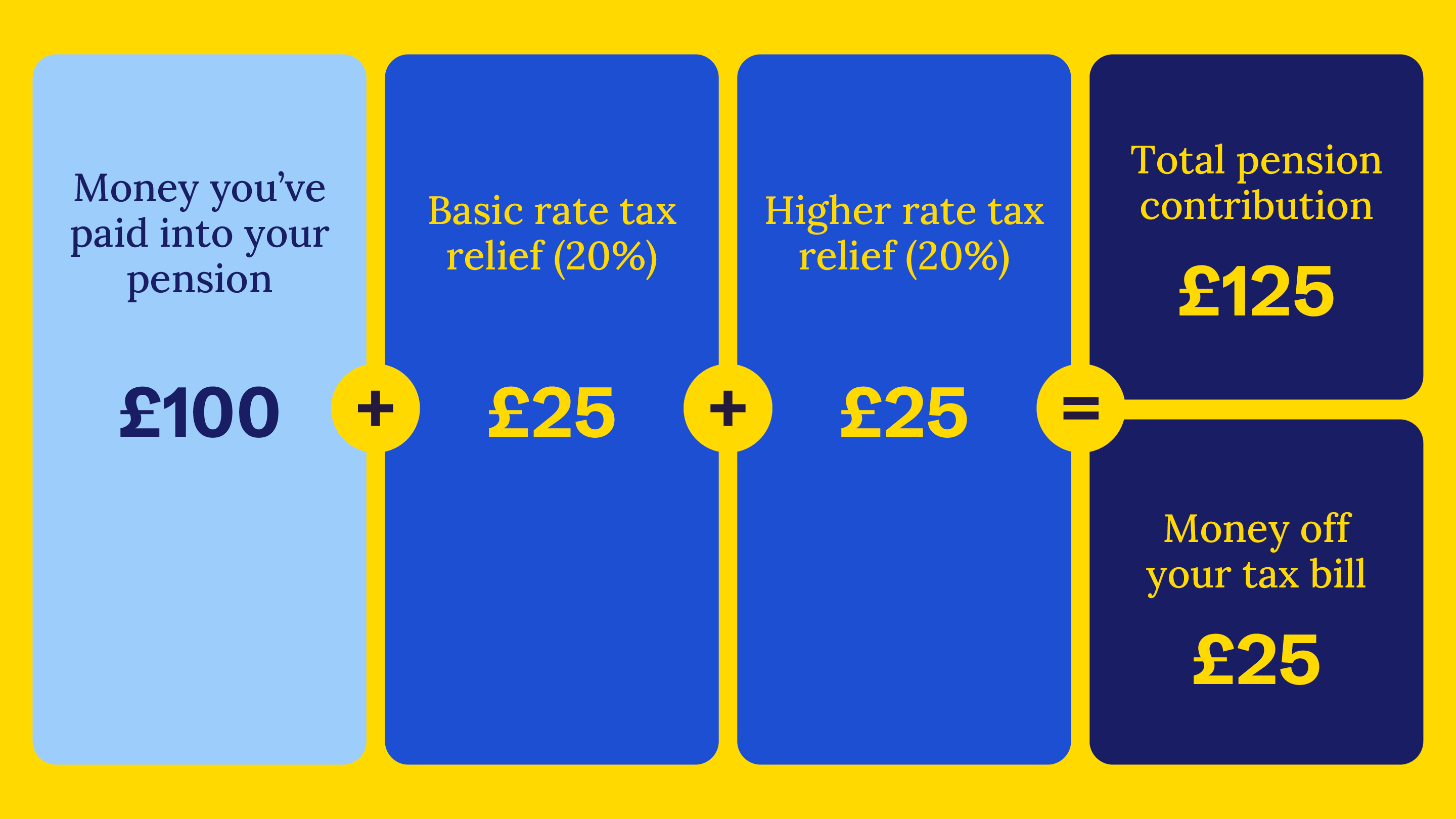

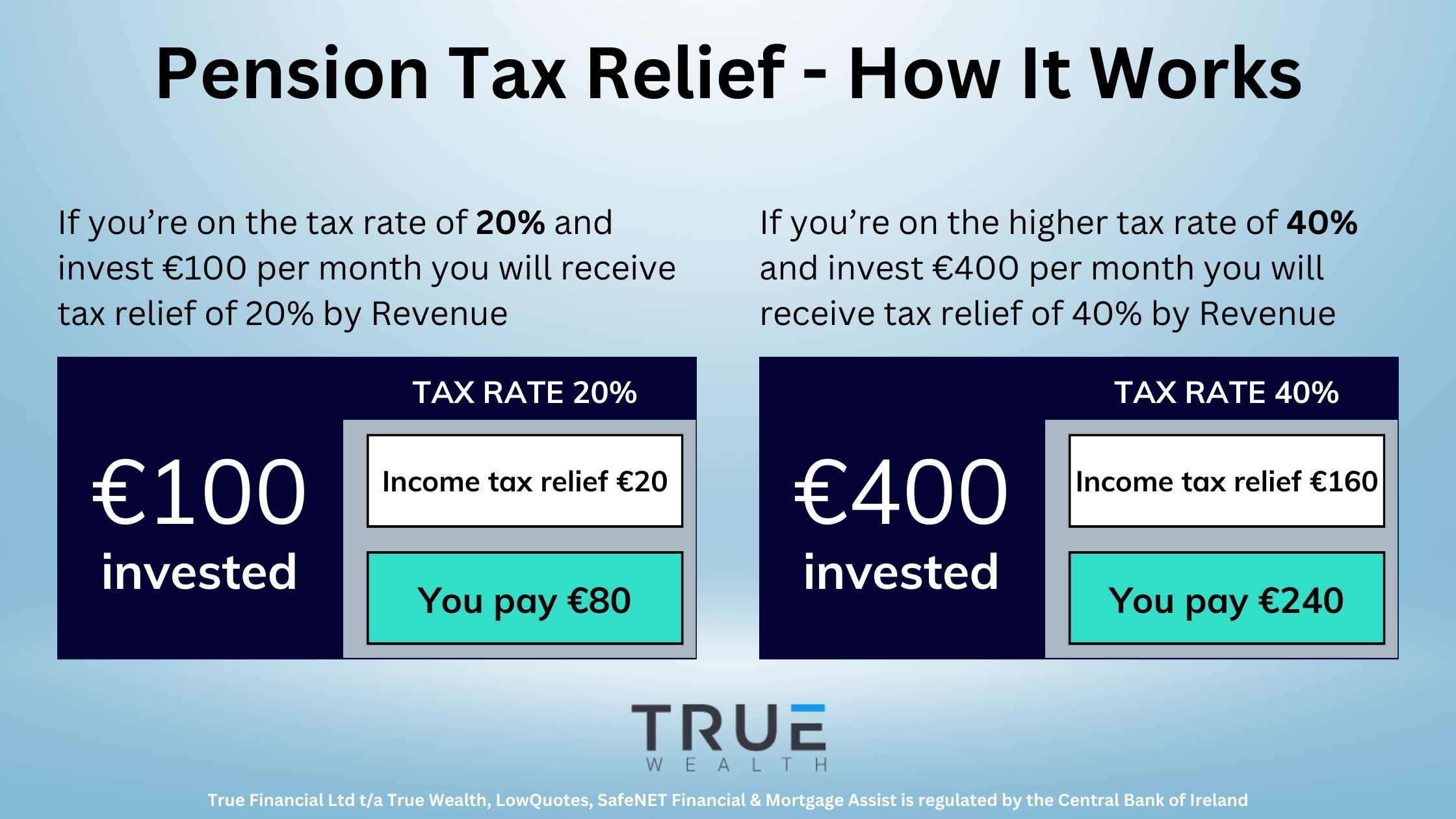

So, if you're a basic rate taxpayer (that's the 20% bracket), for every £80 you put into your pension, the government chucks in an extra £20. Poof! £100 in your pension pot, and you only paid £80. It's like getting a 25% discount on your future self’s happiness. Pretty neat, huh?

If you're a higher rate taxpayer (40%), it's even better! For every £60 you contribute, the government adds £40. That's a 66.7% boost! It’s like a super-sale for your retirement savings. And if you're an additional rate taxpayer (45%), well, you get the most bang for your buck. It’s a powerful incentive, really. The government is basically saying, "Save for your future, and we'll help you do it faster."

How Does This Magic Happen?

There are two main ways this tax relief usually works:

The 'Net Pay' Method (Super Easy!)

For many people, especially those with workplace pensions, this is how it happens automatically. Your employer deducts your pension contribution before calculating your income tax. So, the money you see in your bank account has already had the tax relief applied. You don't have to do a thing! It's like ordering a coffee and the barista already knows you want that extra shot of flavour before they even charge you.

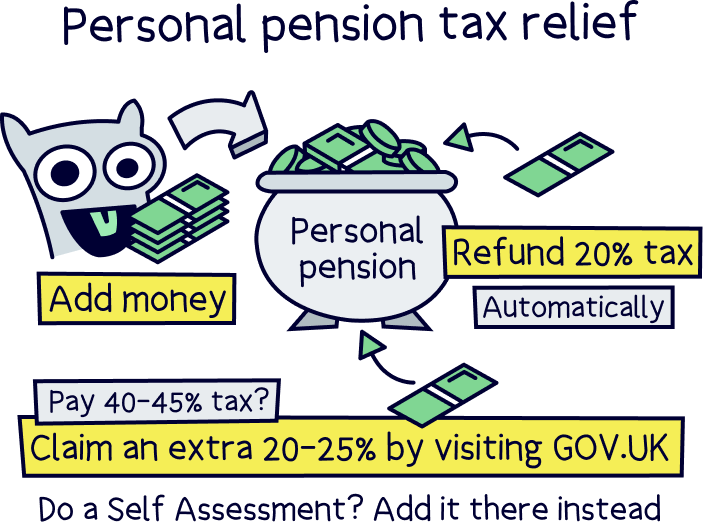

The 'Relief at Source' Method (Still Easy!)

For most personal pensions (like SIPPs - Self-Invested Personal Pensions), your pension provider will claim basic rate tax relief from HMRC on your behalf. So, if you pay £80 into your pension, they'll add the £20. Then, if you're a higher or additional rate taxpayer, you claim the extra relief back through your annual self-assessment tax return. It’s a bit like having a secret agent working for your pension, ensuring it gets all the tax goodies it deserves.

So, when the money's going in, it's definitely tax-advantageous. You're essentially getting a discount on your future wealth. That’s the first big win!

What About When You Start Taking Money Out? That's When the Tax Man Knocks, Right?

Okay, now for the part where you actually start dipping into your pension pot. This is often where people get a bit anxious. "Will I have to pay a fortune in tax then?" you might wonder. Again, it’s not a simple yes or no, but there are some really generous allowances that make a big difference.

The most common way to access your pension is through something called pension drawdown or by buying an annuity. Let's focus on the most common and often more flexible option, which is taking lump sums or regular income directly from your pension.

The 25% Rule: Your Tax-Free Treasure Chest!

This is the golden ticket for most people. When you reach retirement age (which is currently 55, but is rising), you can usually take up to 25% of your pension pot as a tax-free lump sum. Yes, you read that right – completely tax-free. Think of it as a bonus payment from your past self to your present retired self. You could use it for a holiday, a new car, or just to finally buy that fancy coffee machine you've been eyeing!

This 25% is calculated on the total value of your pension at that point, or on a portion of it if you're taking it out gradually. It's a fantastic benefit designed to give you a nice financial cushion as you start retirement.

What About the Rest? The Taxable Bit.

So, if you take 25% tax-free, what happens to the remaining 75%? Well, that's where income tax comes into play. The money you withdraw from your pension pot after the initial 25% lump sum is treated as taxable income. However, and this is a crucial point, you only pay tax on it as and when you take it out.

This means you can manage your income in retirement. If you have other sources of income (like state pension, rental income, or savings interest), you can plan your pension withdrawals to fall within your personal tax allowance for that year. For most people, this means they might not pay any tax at all, or they'll pay a lower rate of tax.

Let's break it down with a super simple example:

- Imagine you have a pension pot worth £100,000.

- You can take 25% of that, which is £25,000, completely tax-free.

- The remaining £75,000 is what you can draw an income from.

- If you take £10,000 from the £75,000 in a tax year, and your personal tax allowance that year is £12,570 (this figure can change), you won't pay any income tax on that £10,000!

See? It’s about being smart with your withdrawals. It's not a massive, immediate tax bill. It's more like a gradual trickle of income that you can often manage to keep within your tax-free allowances.

The Lifetime Allowance: A Little Caveat

Now, there's one thing you might hear about called the Lifetime Allowance (LTA). This used to be a limit on the total amount of pension savings you could have across all your pensions without incurring an extra tax charge. However, as of April 2024, the Lifetime Allowance charge has been abolished. This means you can now accumulate more pension savings without facing additional tax charges on exceeding a specific limit. It's definitely good news for those who have saved diligently over many years!

While the charge is gone, there are still provisions for Benefit Crystallisation Events (BCEs) which are points where your pension rights are tested against previous LTA limits. However, for most people, the removal of the charge means they are far less likely to be affected by it. It's definitely a positive change that simplifies things!

So, To Sum It Up...

Do you pay tax on your personal pension? Yes, but it's highly tax-efficient. You get significant tax relief on the way in, which means your pension grows faster. And when you take money out, you can take a chunk of it completely tax-free. The rest is taxed as income, but you have a lot of control over when and how much you withdraw, allowing you to potentially minimise your tax bill.

It's like planting a seed. You get a little help with the initial planting (tax relief), the plant grows strong and healthy (tax-efficient growth), and when it's time for the harvest, you get a good portion of it for free, and the rest is taxed fairly as you enjoy it. Pretty cool, right?

The key takeaway is that personal pensions are designed to be a rewarding way to save for your future. They offer significant tax advantages that can make a real difference to your retirement nest egg. So, don't be shy about looking into them. Your future self will thank you!

:max_bytes(150000):strip_icc()/taxes-in-retirement-how-much-will-you-pay-2388083v-6-5b4cba9fc9e77c0037315bd8-8ed4f6b983744e1ba2e910636aa65873.png)