Do You Need A Deposit To Remortgage

Hey there, you! So, you're thinking about remortgaging, huh? Smart move, really. It's like giving your mortgage a little glow-up. But then, the nagging question pops into your head, right? Like a little pop-up ad you can't close: "Do I need a deposit to remortgage?" It’s a classic. Makes you pause, doesn't it? Like you're about to embark on some grand financial adventure, and there might be a secret entrance fee. Let's spill the beans, shall we?

Grab your coffee (or tea, no judgment here!), and let's chat about this. Because, honestly, who has time for complicated jargon when we're just trying to figure out if we need to dig into our savings again? It’s not like you’re buying a whole new house, so why would you need a deposit, right? It seems a bit… counterintuitive. Like asking a chef to bring a salad to a steak dinner. Just doesn’t quite fit.

So, the short, sweet, and hopefully not-too-disappointing answer is: usually, no, you don't need a deposit to remortgage. Hooray! See? Not so scary after all. Think of it this way: when you remortgage, you're essentially swapping your old mortgage for a new one. You're not buying a new property, so the lender isn't taking a risk on a brand new asset. They're looking at the equity you've already built up in your current home. It’s like a friendly handshake with a new bank, not a full-blown house hunt.

Must Read

But, of course, life isn't always a simple yes or no, is it? There are always those little ifs and buts that like to sneak in. So, let's unpack this a bit more. What's actually going on behind the scenes when you remortgage?

What is Remortgaging, Anyway? (A Quick Recap)

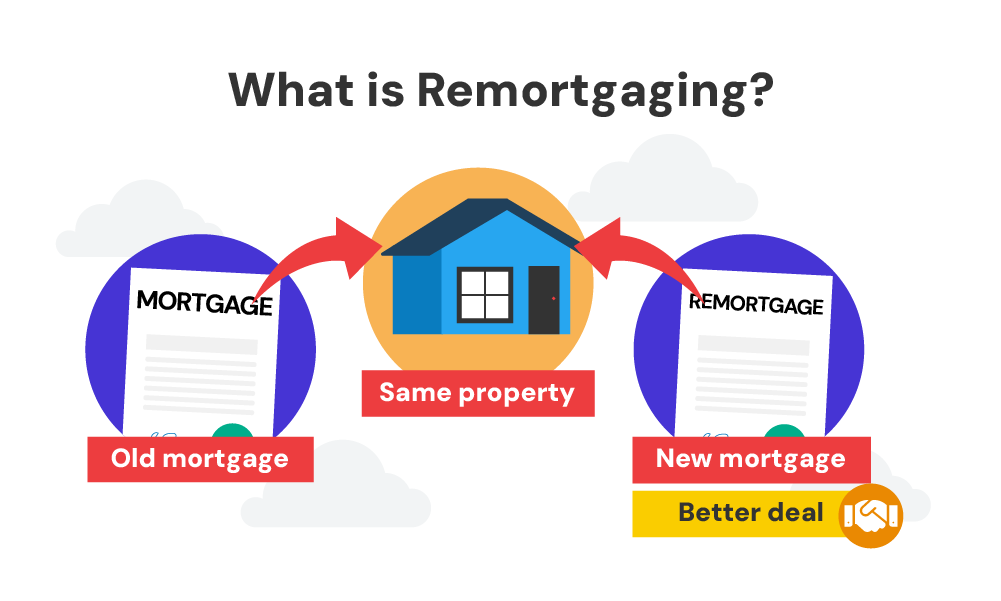

Okay, imagine your current mortgage. It's been with you for a while. Maybe the interest rate is creeping up like a vine, or perhaps you've heard whispers of much better deals out there. Remortgaging is basically taking out a new loan to pay off your old one. You're not moving house, but you are moving lenders, or sometimes, even staying with your current lender but getting a new product. It's all about getting a better deal, freeing up cash, or maybe even shortening your loan term. Like giving your financial life a little… refresh. Or a complete overhaul, if you're feeling brave!

The key here is that you already own your home. You've been paying it off, little by little. That means you've built up some equity. Fancy word, I know. But it just means the difference between what your house is worth and what you still owe on your mortgage. So, if your house is worth £200,000 and you owe £150,000, you've got £50,000 in equity. That's your stake in the game. It's your own money, essentially, sitting there. Lenders love to see that. It shows you're a good bet. Like a well-behaved student who always hands in their homework on time.

So, Why the Deposit Question?

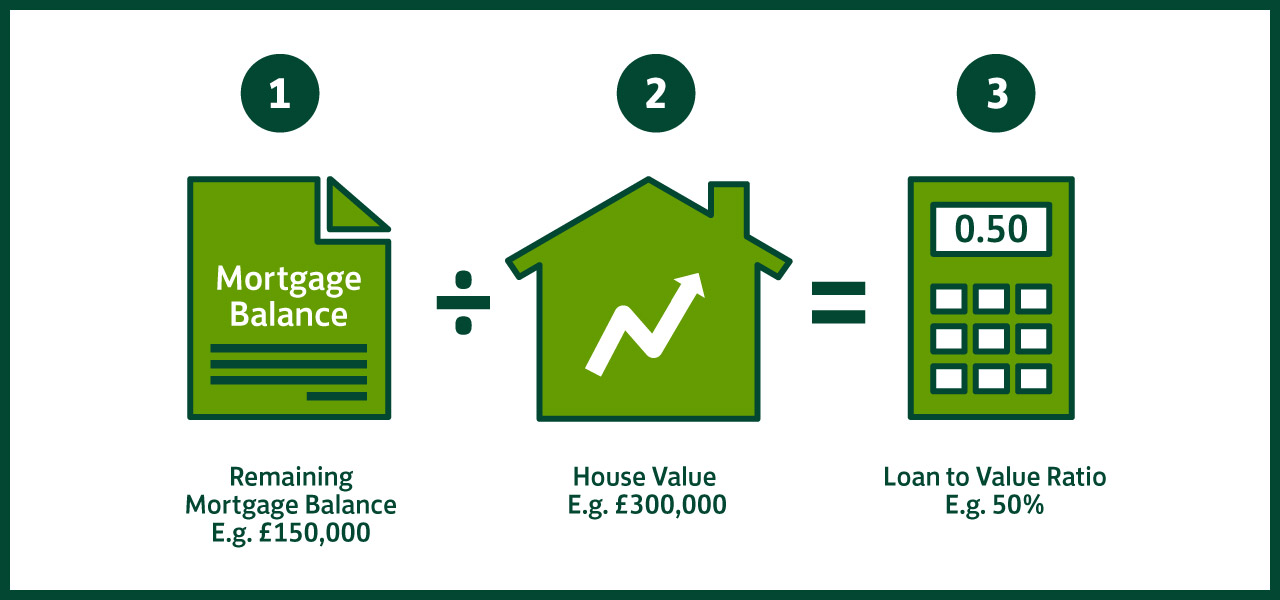

Now, you might be thinking, "But my mate Dave, he had to put down a deposit when he remortgaged!" And that, my friend, is where things get a tiny bit more nuanced. It all comes down to your Loan-to-Value (LTV) ratio. Another one of those financial phrases that sounds like it belongs in a sci-fi movie, right? But it's actually quite simple.

LTV is just a percentage. It's the amount you want to borrow compared to the value of your home. So, if your home is worth £200,000 and you want to borrow £160,000, your LTV is 80% (£160,000 / £200,000 = 0.80). Simple math, really. You probably did this when you first bought the place, too. Except then, you definitely needed a deposit because you were buying a whole new thing!

Lenders use LTV to assess risk. The lower your LTV, the less risk for the lender. They're basically saying, "Hey, if this person suddenly decides to stop paying, we're not going to lose our shirts because they've got a good chunk of their own money tied up in this." Makes sense, doesn't it?

Most lenders offer their best rates to people with lower LTVs. Think of it as a reward for being financially responsible. Like getting a gold star on your report card. Generally, if your LTV is 80% or lower, you won't need to provide an additional deposit. You've already got enough skin in the game. You're golden!

When Might You Need to Chip In?

Ah, here comes the plot twist! What if your LTV is a bit higher? Say, you've had a bit of a rough patch, or maybe property prices in your area have taken a bit of a nosedive (ouch!). Or perhaps you want to borrow more money than you currently owe, maybe to do some renovations? That's when things can get interesting. You might find yourself needing to put down a deposit. It’s not ideal, I know. It feels like you’re going backwards, doesn't it?

For example, if you want to remortgage and your LTV would be above 80%, say 85% or 90%, some lenders might ask for you to contribute. They’ll want you to bring that LTV down to a level they're comfortable with. So, if your house is worth £200,000 and you want to borrow £180,000 (a 90% LTV), and the lender only offers their best deals up to 80%, you might need to find that extra 10% (£20,000) as a deposit. Ouch. Suddenly, that deposit question feels a lot more real, doesn't it? It’s like finding out your favourite dessert has an extra, unexpected ingredient you didn't ask for.

This often happens when you're looking to borrow a higher percentage of your home's value. It's their way of saying, "We're happy to lend, but we want you to share a bit more of the financial burden." It’s all about risk management for them. Think of it as them wanting to see you’re really committed to this house. You've got to show them you've got a serious crush on your property, financially speaking!

What About Borrowing Extra Cash?

This is a big one. Many people remortgage not just for a better rate, but to release some of the equity they've built up. Want to do that dream kitchen renovation? Or maybe you're thinking about consolidating some debts? Remortgaging can be a great way to do it. But here’s the kicker: when you borrow more money, your LTV goes up. And a higher LTV often means you might need to contribute a deposit.

Let's say you owe £150,000 on your £200,000 house, and you want to borrow an extra £50,000 for an extension. That’s £200,000 you want to borrow in total. Your LTV is now 100% (£200,000 / £200,000). Woah! Most lenders aren’t keen on that. They want to see that you've got some buffer. So, if the lender will only lend up to 85% LTV, and you want to borrow £200,000 on a £200,000 house, you'd need to find that extra 15% (£30,000) yourself. It’s like trying to get a VIP pass, but they only let so many people in, and you’ve got to pay a bit extra for the exclusive experience.

It really depends on the lender's policies and how much of your home's value they're willing to lend against. Some are more flexible than others. It's a bit like dating – some people are pickier than others! Always shop around and see who offers what.

What if Your Property Value Has Dropped?

This is a tough one, and unfortunately, it happens. Property markets aren't always on an upward trajectory. If the value of your home has decreased since you took out your current mortgage, your LTV might have increased even if your outstanding balance hasn't. So, you might find yourself in a situation where you're effectively borrowing a higher percentage of its current worth. And guess what? That can trigger the need for a deposit.

Imagine you bought your house for £250,000 with a £200,000 mortgage (80% LTV). Five years later, your house is now only worth £220,000, and you still owe £180,000. Your new LTV is a whopping 81.8% (£180,000 / £220,000). Even though you've paid off some of the mortgage, your percentage borrowing has gone up because the house value has dropped. So, if the lender you're looking at only goes up to 80% LTV, you might be asked for a deposit to bring it down. It's like trying to fit into a pair of jeans that have shrunk in the wash – you might need to do some... financial dieting.

Don't Panic! There are Always Options.

Okay, so if you do find yourself in a situation where a deposit seems to be on the cards, don't throw your hands up in despair! There are usually other avenues to explore.

First up: shop around like it's Black Friday. Seriously. Different lenders have different LTV criteria. Some might be happy to lend at a higher LTV than others. You might find a lender who will accept your LTV without asking for a deposit, even if it's slightly higher than another's preferred rate. It’s all about finding the right match. Like a dating app for mortgages!

Second: consider a guarantor. This is a bit more niche, and usually for more complex situations, but sometimes a family member with good credit and assets might be able to act as a guarantor. This essentially means they’re promising to cover your mortgage payments if you can’t. It’s a big ask, of course, but it's an option for some.

Third: wait it out. If your LTV is only slightly over the preferred threshold, and you're not in a desperate rush, you could focus on paying down more of your mortgage over the next year or so. Every little bit you pay off reduces your LTV. It might just be enough to put you in a better position for your next remortgage attempt.

Fourth: consider a mortgage broker. These guys are the wizards of the mortgage world. They know the market inside out, and they can find deals that you might not find on your own. They can also be brilliant at navigating those tricky LTV situations. They speak fluent "lender-ese." Think of them as your financial secret weapon.

The Bottom Line

So, to circle back to our original question: do you need a deposit to remortgage? Most of the time, and if you're in a good equity position (meaning your LTV is reasonably low), then absolutely not! It's one of the perks of already owning your home. You're not starting from scratch. You've got that sweet, sweet equity.

However, if your LTV is high, if you're looking to borrow a significant amount more than you currently owe, or if your property's value has dipped, then yes, you might be asked to chip in. It's all about risk. But even then, don't despair! There are always ways to explore. So, chin up, do your research, and happy remortgaging!

Now, go on, pour yourself another cuppa and enjoy the peace of mind that you've got this. It’s not as complicated as it sounds, right? Just a few numbers, a bit of understanding, and you’re good to go. You've got this!