Can You Have Two Mortgages At Once

So, you've got that cozy house. It's your castle, your happy place. But lately, you've been eyeing another little slice of heaven. Maybe a weekend getaway cabin? Or a rental property to make some extra cash?

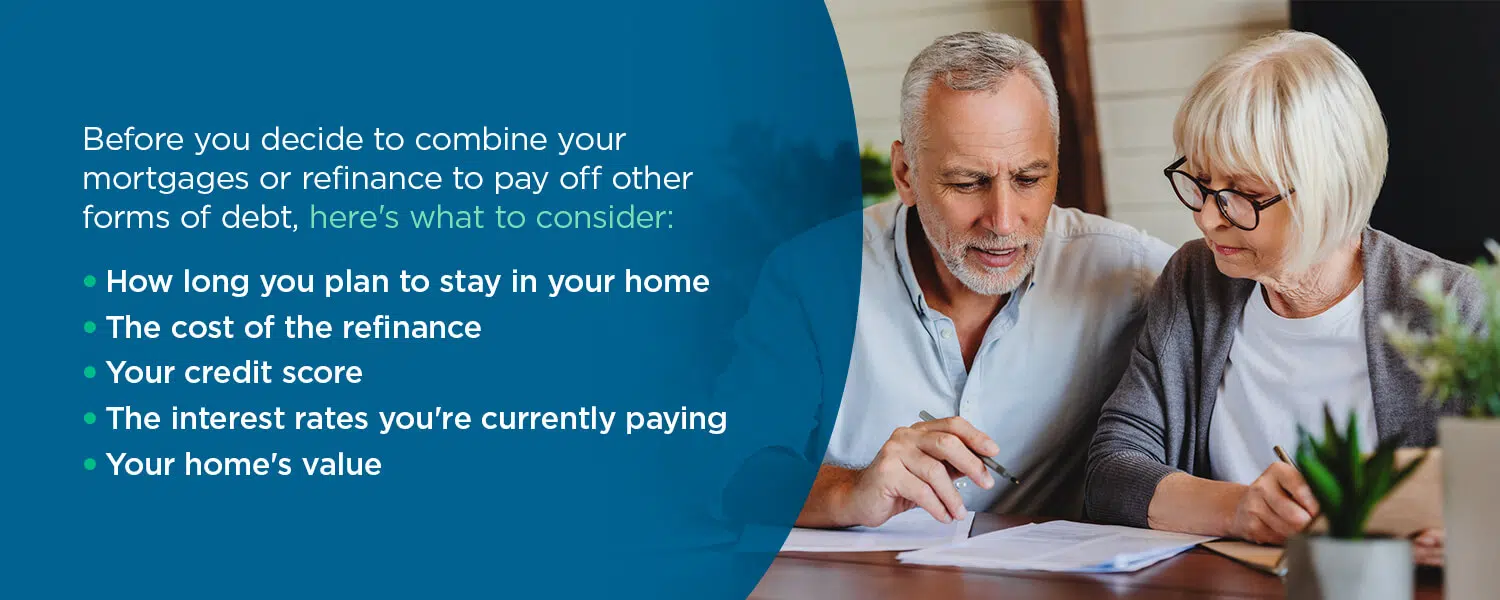

The question pops into your head, a little whisper, a mischievous thought: Can you have two mortgages at once? It sounds a bit like juggling flaming torches while riding a unicycle. Intensely exciting, but also a tad terrifying.

Let's be real, most of us think one mortgage is a pretty big commitment. It's like signing your life away for a few decades, right? It feels like a lifelong dance with Bank of America or Wells Fargo.

Must Read

But what if your bank account is doing a little happy jig? What if you've got a stable job and a decent savings cushion? Suddenly, that second mortgage doesn't sound so outlandish.

The short answer, my friends, is a resounding yes! You absolutely can have two mortgages. Shocking, I know. It’s not some mythical creature whispered about in hushed tones by financial wizards.

Think of it this way: your first mortgage is your primary residence. That's your main squeeze, your ride-or-die. Your second mortgage? Well, that's like a delightful fling, a secondary adventure.

Now, before you start browsing Zillow for that beachfront condo, there are a few tiny, minuscule, almost insignificant details to consider. Just a few little speed bumps on your mortgage superhighway.

First off, lenders are going to look at your debt-to-income ratio. This is their fancy way of saying, "How much money are you bringing in versus how much are you already promising to pay out?" They like to see that you're not already drowning in payments.

Having a second mortgage means a bigger monthly payment. That's just math, people. So, your income needs to be robust enough to handle both. No one wants a lender to send you a sad, glitter-covered "We're breaking up" letter.

Your credit score is also going to be your BFF in this scenario. A stellar credit score is like a golden ticket. It tells lenders, "This person is responsible! They pay their bills on time! They probably even fold their socks!"

A higher credit score means you're less of a risk. And less risk for the lender means better interest rates for you. Everyone wins! Except maybe your sock drawer, which might be a bit less organized.

The type of property you're buying matters too. A vacation home might be viewed differently than a primary residence. Lenders might have different rules for investment properties.

So, if you're dreaming of that mountain lodge, you might need to do a bit more homework. It’s not just about the view; it’s about the mortgage terms.

The loan process for a second mortgage can be a bit more involved. Lenders want to be extra sure you can handle the financial juggling act. They’ll probably ask for more documentation than they did the first time.

Get ready for paperwork. So much paperwork. You might start seeing mortgage forms in your sleep. It’s like a financial obstacle course designed by a particularly organized squirrel.

You'll likely need a decent down payment for your second property. Lenders want to see that you've got some skin in the game. They don't want to feel like they're the only ones taking a gamble.

Think of it as a test of your financial fortitude. Can you build two homes (or one home and one rental empire) without collapsing into a puddle of spreadsheets?

Some people use a Home Equity Line of Credit (HELOC) on their first home to help with the down payment on a second. That's like borrowing from your castle to build a new turret. It's a clever move, but also requires careful consideration.

A HELOC allows you to borrow against the equity you've built in your current home. It can be a flexible option, but remember, it's still a loan with interest. Don't get too carried away with HELOC champagne.

Then there's the whole "what if life throws a curveball?" scenario. Job loss, unexpected medical bills, a sudden urge to buy a llama farm. These things happen.

Having two mortgages means you have two significant financial obligations. If one income stream dries up, it can become a real pickle. A very expensive pickle.

It's important to have an emergency fund that's substantial enough to cover multiple mortgage payments. Think of it as your financial superhero cape, ready to swoop in when things get dicey.

Some people see two mortgages as a way to build wealth. Owning multiple properties can lead to appreciation and rental income. It's a long-term investment strategy.

It's like planting two financial trees and hoping they grow into money-making forests. Just make sure you've got good soil and plenty of sunshine (or, you know, a stable economy).

Others might take on a second mortgage for a different reason entirely. Perhaps a co-signer on a family member's home. Or helping a child buy their first place.

This is where the emotional side of mortgages comes into play. It's not always just about spreadsheets and interest rates. Sometimes, it's about family and shared dreams.

The important thing is to be honest with yourself and with your lenders. Don't try to hide your financial situation. They have ways of finding out, and it's rarely a pleasant discovery.

It’s like trying to hide a giant, sparkly unicorn in your backyard. Eventually, someone's going to notice.

So, can you have two mortgages at once? Yes. Is it for everyone? Probably not. It requires careful planning, a strong financial foundation, and perhaps a slightly adventurous spirit.

If you’ve got the income, the credit, and the desire, then go forth and explore the possibilities. Just remember to breathe and maybe have a good financial advisor on speed dial. They're like your mortgage sherpas, guiding you through the treacherous peaks.

And hey, if it all works out, you could end up with two amazing places to call your own. One for quiet evenings, and one for, well, even more quiet evenings. Or maybe one for Netflix binges and the other for hosting epic board game nights.

The possibilities are as vast as your mortgage potential. Just remember, with great financial power comes great responsibility. And maybe a little bit of extra paperwork.