Can You Add Negative Equity To A New Car Loan

Imagine this: you're practically skipping into the dealership, ready to snag that shiny new car you've been dreaming about. The scent of fresh upholstery, the gleam of the paint... it's all so exciting! But then, your friendly salesperson, let's call them "Mr./Ms. Dealmaker", drops a little bombshell. They mention something about "rolling over" your old car loan. And suddenly, that dream car starts to feel a tiny bit like a financial juggling act. The question that might pop into your head is, "Can you actually add negative equity to a new car loan?" It sounds a bit like a magic trick, doesn't it?

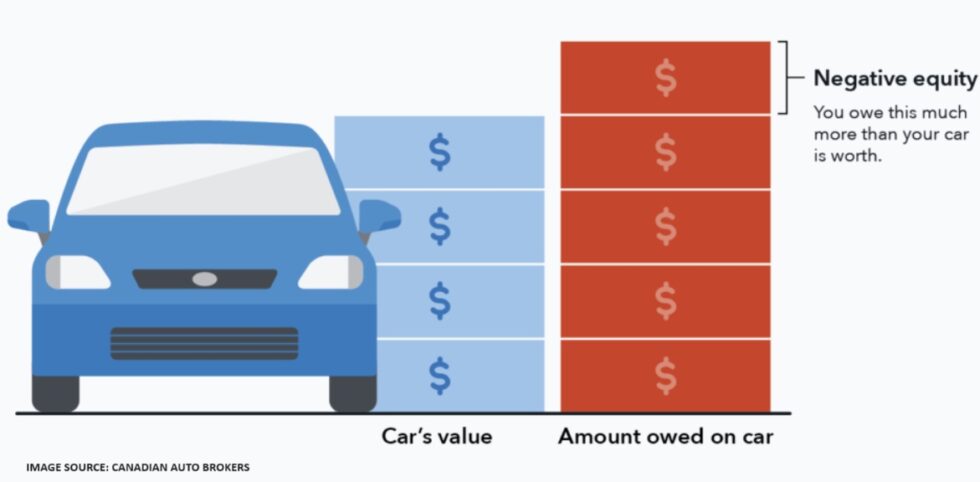

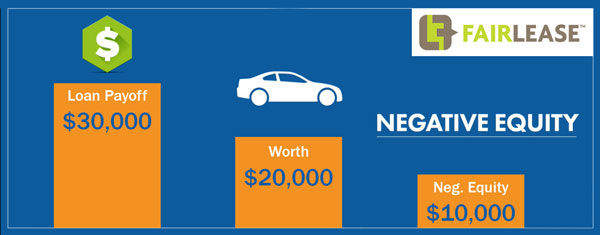

Think of negative equity like this: your old car is worth less than what you still owe on it. So, if your car is worth $5,000 but you owe $7,000, you have a whopping $2,000 in negative equity. It's like owing more on a pizza than the pizza is actually worth. A bit of a head-scratcher, right? And when you're eyeing that fabulous new set of wheels, the thought of tacking that debt onto your new purchase might seem a little... wild. But it's a real thing, and it happens more often than you might think. It's one of those quirky financial twists that makes the car-buying journey so unexpectedly thrilling!

So, can you do it? The short answer is, yes, you can. It's a bit like adding an extra topping to your already decadent ice cream sundae, but with your car loan. Dealerships and lenders often have programs that allow them to finance that negative equity right into your new car loan. This means that instead of paying off that $2,000 shortfall from your old car separately, they'll just add it to the price of your new one. Pretty neat, huh? It’s a way for them to help you drive away in that new car without having to come up with that extra cash on the spot. It’s a clever financial maneuver, and honestly, a little bit of a spectacle to witness firsthand. It’s like watching a magician pull a rabbit out of a hat, but the rabbit is your old car debt, and the hat is your new car loan.

Must Read

Now, why would anyone do this? Well, life happens! Maybe your old car took a nosedive in value faster than you expected. Perhaps unexpected bills popped up, and you couldn't afford to pay off the difference. Whatever the reason, negative equity can be a sticky situation. When the opportunity arises to simply roll it into a new loan, it can feel like a lifesaver. It means you don't have to drain your savings or take out a separate, high-interest personal loan to clear the slate. It’s a way to smooth out the financial bumps and keep your car-buying dreams alive. This whole process can feel like a grand financial play, with lots of moving parts and surprising outcomes. It's the kind of thing that makes you lean in and pay attention!

But here's where things get really interesting, and a little bit like a financial tightrope walk. When you add negative equity to your new car loan, you're essentially borrowing more money than the new car is actually worth. This means your new car starts its life with you already "upside down" on the loan. It's like buying a brand new, top-of-the-line smartphone and immediately discovering it's worth less than you paid for it. It’s a curious financial paradox that makes you wonder about the inner workings of the car market and loan structures.

Think of it as a financial gamble, a daring move in the world of car financing!

This also means your monthly payments will be higher than they would be if you weren't carrying that extra debt. You'll be paying interest on the negative equity, meaning you'll end up paying more over the life of the loan. It’s like buying a large pizza and then having to pay extra for the crust, even though you didn't really want it. This can make it harder to build equity in your new car, which is the part of the car's value that you actually own. Building equity is like planting seeds for future financial growth; when you start with negative equity, it’s like planting those seeds in rocky soil.

So, is it a good idea? Well, that's the million-dollar question, isn't it? It can be a practical solution if you're in a pinch and need a new car. It can help you avoid the immediate financial burden of paying off the old loan. However, it's crucial to understand the long-term implications. You'll be in debt for longer, and you'll pay more in interest. It’s a trade-off, like choosing a shortcut that might be a bit more scenic but also takes a little longer. The whole concept is fascinating because it highlights the flexibility and sometimes surprising strategies employed in automotive finance. It’s a testament to how lenders try to facilitate sales and how consumers navigate their financial realities.

What makes this whole scenario so special is the sheer ingenuity of it. Lenders are essentially finding ways to keep people driving new cars, even when they're carrying past financial baggage. It's a testament to the power of creative financing and the desire for that new-car smell. It’s a bit of a financial dance, a tango between desire and debt. And for many people, it's a dance they have to perform to upgrade their ride. The fact that this option even exists is a conversation starter in itself. It’s like discovering a secret menu at your favorite restaurant; it’s there, it’s an option, and it changes the entire dining experience.

So, the next time you’re at a dealership, and you hear that phrase about "rolling over" your old loan, you'll know exactly what's happening. It’s not just a sales pitch; it’s a financial strategy that allows you to blend your past debt with your future automotive dreams. It's a bit of a gamble, a bit of a solution, and a whole lot of financial intrigue. It’s the kind of thing that makes you realize the world of car loans is far more exciting and complex than you might have initially thought. It’s an adventure, really, in your financial journey towards that shiny new vehicle. You might even feel a little thrill just knowing this option is out there, waiting to be explored. It’s like having a special key to unlock a new chapter in your car ownership story!