At What Age Can You Retire With 500k

Hey there! So, you're wondering about that magic number, right? That sweet spot where you can finally ditch the alarm clock and maybe even swap the spreadsheets for… well, whatever floats your boat. We're talking about retiring with 500k. Sounds like a lot, but can it actually buy you freedom? Let's spill the beans.

Picture this: you’re sipping your first cup of coffee, no rush, no deadlines. Just pure, unadulterated chill. That’s the dream, right? And $500,000 is often tossed around as this big, shiny goal. But is it a real goal, or just another one of those "get rich quick" schemes that’s actually a "get rich verrrryyy slowly" scheme? 😉

So, Can $500k Make You a Retiree?

The short answer? Maybe. Yeah, I know, not exactly the fireworks you were hoping for. But honestly, retirement is a super personal thing. It’s like asking, "What’s the perfect pizza topping?" Everyone’s got a different answer, and it depends on a whole bunch of factors. Your lifestyle, where you live, how much you like to spend money (guilty as charged sometimes!), all that jazz.

Must Read

Think about it. If you’re picturing yourself living in a tiny hut in the woods, eating berries and whittling for fun, then $500k might actually be a king’s ransom. You could probably live like royalty! But if your dream retirement involves daily fine dining, private jets, and a butler named Jeeves (because, why not?), then yeah, $500k might feel a bit… tight. Like trying to fit a whale into a sardine can.

The "4% Rule" – Our New Best Friend (Sort Of)

Okay, so there’s this thing the super-smart financial gurus talk about. It’s called the 4% rule. Basically, the idea is you can withdraw 4% of your retirement savings each year, and it should last you a really long time. Like, forever long. It’s based on historical market returns, which, let’s be honest, can be a bit of a rollercoaster.

So, for our $500k hypothetical situation, 4% of that is… drumroll please… $20,000. Per year. Sounds like pocket money, doesn’t it? But wait, it’s not just $20,000. That’s $20,000 you can take out every single year without touching the principal. Pretty neat, huh?

Now, let’s do some quick math. $20,000 a year. Can you live on that? For some people, absolutely. Especially if they have other income sources. Social Security, maybe a small pension from a former life, or even a side hustle that’s more fun than work. But for many, $20,000 a year isn't going to cut it. Not by a long shot. It’s like trying to fuel a Bentley with a teacup of gas.

![Can I Retire at 60 with $500K? [YES! See Examples of How]](https://youngandtheinvested.com/wp-content/uploads/retire-at-60-with-500k-retirement-analysis.webp)

So, What Age Are We Talking About?

This is the million-dollar question, right? (Or, in our case, the $500k question!) If you can live on $20,000 a year, and you manage to squirrel away $500k by, say, age 50… then boom! You could theoretically retire. That’s a pretty early retirement, my friends. Imagine telling your boss, "See ya!" at 50. Pure bliss.

But let's get real. For most of us, $20,000 a year isn't exactly living the high life. We’re talking about covering the absolute bare essentials. Rent or mortgage, food, utilities, a little bit of fun money for… well, a little fun. Forget fancy vacations or that brand-new Tesla you’ve been eyeing. So, if you want a more comfortable retirement, you're probably looking at needing more than $500k, or you’re going to need to work a bit longer.

The Age Factor: It's a Biggie!

The older you are when you retire, the less time your money has to last. That’s just basic math, but it’s a crucial point. If you retire at 60 with $500k, that $20k withdrawal is expected to cover about 25 years of living. If you retire at 70, it’s only about 15 years. See the difference? It’s like the difference between a marathon and a sprint. And retirement is definitely a marathon, people!

And let’s not forget about inflation. That $20,000 today won’t buy you the same amount of stuff in 10 or 20 years. Prices go up, my friends. Everything gets more expensive. So, while the 4% rule is a good starting point, it's not a crystal ball. We have to factor in that the cost of living will likely increase over time. Your $20k might become $25k, then $30k, and so on. Suddenly, that $500k starts to shrink a little faster, doesn't it?

What Else Needs to Be on Your Radar?

So, we’ve established that $500k can work, but it’s a bit of a tightrope walk for many. What else should you be thinking about? Let’s dive a little deeper.

Healthcare Costs: The Boogeyman of Retirement

This is a huge one. Seriously. Health insurance in retirement can be ridiculously expensive. Unless you’re lucky enough to have a super-generous employer who provides retiree health benefits (and let’s be honest, those are rarer than a unicorn these days), you’re going to be on the hook for those premiums. And as you get older, your healthcare needs tend to… increase. Who knew? 😅

Think about deductibles, co-pays, prescriptions. These costs can add up faster than you can say "ouch!" So, when you're planning your $500k retirement, you absolutely need to factor in a solid chunk for healthcare. It’s not a suggestion; it’s a necessity. It's like planning a road trip and forgetting to budget for gas. Not going to get very far!

Lifestyle Creep: The Silent Killer of Savings

This is where “lifestyle creep” comes in. It’s a fancy term for how our spending habits tend to increase as our income increases. You get a raise, you buy a nicer car. You save more, you start thinking about that bigger house. It’s insidious! And in retirement, it can be your savings’ worst enemy.

If you’re used to a certain level of spending, and you don’t consciously adjust it for retirement, that $500k can disappear quicker than free donuts in the breakroom. You have to be honest with yourself about your spending. Can you downsize your life a bit? Can you find cheaper hobbies? Can you learn to love generic brands? (Okay, maybe not that extreme, but you get the picture.)

So, Can You Retire with $500k and Live Comfortably?

Let’s revisit this. If you’re talking about a comfortable retirement, one where you’re not constantly counting pennies and can enjoy some of life’s little luxuries, then $500k might not be enough for everyone, especially if you're looking to retire early.

Most financial planners will tell you that aiming for 10-15 times your annual income is a safer bet for retirement. So, if your desired annual retirement income is, say, $50,000, then you’d ideally want $500,000 to $750,000 saved. See how $500k starts to look a little less like a golden ticket and more like a good start?

What About Social Security?

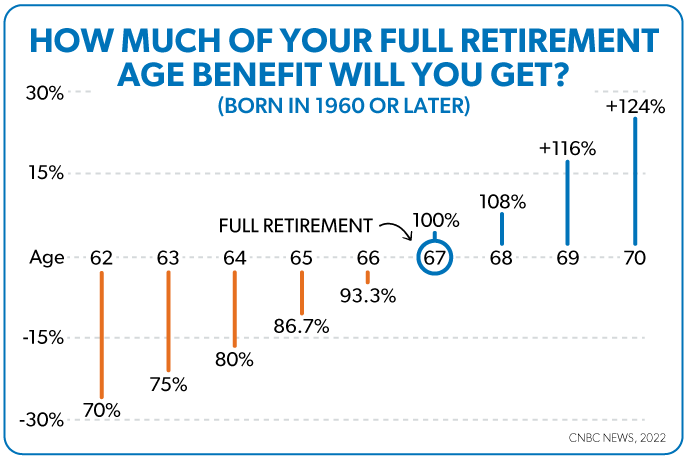

Ah, Social Security. Our collective safety net. For many, it’s going to be a significant part of their retirement income. The amount you receive depends on your earnings history, and when you choose to claim it. Claiming it early means smaller payments, while waiting longer means bigger payments. It's a trade-off, a bit like choosing between a quick but small scoop of ice cream or a longer wait for a bigger scoop. And let's be honest, the older you are when you claim, the more you’ll be covered by that $500k as well, making it stretch further.

So, if you have $500k saved and you're expecting a decent Social Security check, your retirement picture changes dramatically. That $20,000 withdrawal from your savings becomes supplemental income, not your sole means of survival. Suddenly, retirement at 60 with $500k seems much more feasible, even with a comfy lifestyle in mind.

The Age Sweet Spot: A Range, Not a Number

Instead of a specific age, think of it as a range. If you have $500k, and you’re okay with a more modest lifestyle, or you have other income streams like Social Security, you might be able to retire in your late 50s. If you want a truly luxurious retirement, or you don’t have other income, you’re probably looking at closer to your late 60s or even early 70s, and you might want to aim for more than $500k.

It’s all about the balance. Your savings, your desired spending, your expected lifespan, and any other income sources. It's a puzzle, and each piece is crucial. Don't forget to factor in taxes too! Those withdrawals from your retirement accounts aren't always tax-free, and taxes can eat into your nest egg faster than a hungry teenager at a buffet.

Don't Forget the Fun Stuff!

Retirement isn’t just about surviving; it’s about thriving! What do you want to do with all that newfound free time? Travel? Learn a new skill? Volunteer? Spend quality time with grandkids (or pets!)? Make sure your budget accounts for the things that truly bring you joy. If your retirement dreams involve expensive hobbies, you’ll definitely need a bigger nest egg or a longer working career.

The most important thing is to plan. Don't just wing it. Talk to a financial advisor (if you can afford one!), crunch the numbers, be realistic about your expenses, and have a clear vision of what you want your retirement to look like. $500k is a fantastic start, a really impressive milestone, but it’s just one piece of a much bigger, more exciting picture.

So, can you retire with $500k? Yes, it’s possible. But the age at which you can do it comfortably, and without living like a pauper, is a very individual journey. It’s about smart planning, realistic expectations, and a healthy dose of optimism. Now, who’s ready for another coffee and some more dreaming?